MNI US MARKETS ANALYSIS - Equities Yet to Erase Tariff Drop

Highlights:

- Treasuries pressured, yields supported as tariff letter deluge underpins uncertainty

- GBP underperforms as steel, aluminium deal may miss deadline

- Light schedule keeps focus on the White House

US TSYS: Carry-Over Selling, Tariff by Tweet Watch

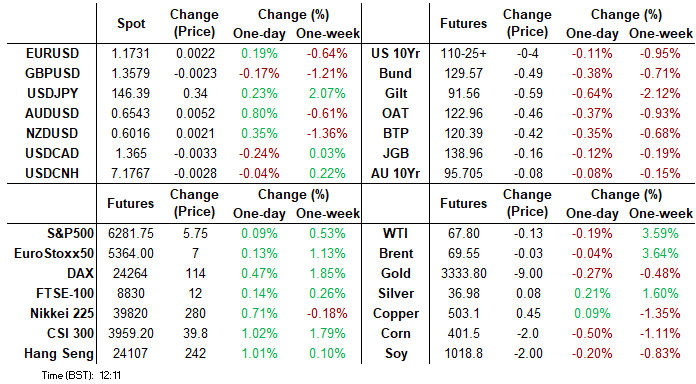

- Treasuries remained under pressure overnight, currently extending lows with the Sep'25 10Y contract back at June 20 levels despite delaying the July 9 tariff deadline to August 1 yesterday.

- Selling continues after after Pres Trump announced 25% tariffs on Japan and South Korea Goods. Additional announcements included: 25% tariffs on Malaysia and Kazakhstan, 30% on South Africa and 40% on Laos and Myanmar. Tsys largely ignored the EUs 10% tariff deal "with caveats", negotiations ongoing.

- Currently, the Sep'25 10Y contract trades -3.5 at 110-26 (110-25 low / 111-01.5 high). After trading through support at the 50-day EMA (110-31), sights are on 110-17 next, a Fibonacci retracement point. A break would strengthen a bearish threat. Resistance to watch is at 111-28, the Jul 3 high.

- Curves bear steepen: 2s10s +2.333 at 50.608 (48.455 low), 5s30s +1.801 at 97.362 (95.370 low); 10Y yield +.0318 at 4.4112% (4.4191% high).

- The USD back near steady (Bbg US$ index -.35 at 1196.16) after scaling back Monday's bounce on the initial Japan/S.Korea tariff headlines.

- Looking ahead - economic data limited to NY Fed 1-Yr Inflation Expectations at 1100ET, Consumer Credit at 1500ET. US Tsy auctions $50B 6W & $50B 52W bills at 1130ET, $58B 3Y Note auction (91282CNM9) at 1300ET. No scheduled Fed speakers today, main focus on the release of FOMC minutes for the June meeting tomorrow at 1400ET.

SOFR: Mix Of Net Short Setting & Long Cover Around Independence Day Weekend

OI data points to net short setting dominating through the SOFR greens between Thursday and Monday settlements (no settlement Friday, owing to the observance of the Independence Day holiday), before net long cover came to the fore in the blues.

| 07-Jul-25 | 03-Jul-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,318,372 | 1,315,935 | +2,437 | Whites | +51,835 |

SFRU5 | 1,190,957 | 1,173,169 | +17,788 | Reds | +19,392 |

SFRZ5 | 1,282,265 | 1,267,246 | +15,019 | Greens | +9,042 |

SFRH6 | 983,694 | 967,103 | +16,591 | Blues | -5,011 |

SFRM6 | 852,563 | 855,055 | -2,492 |

|

|

SFRU6 | 837,275 | 829,721 | +7,554 |

|

|

SFRZ6 | 912,525 | 913,547 | -1,022 |

|

|

SFRH7 | 725,545 | 710,193 | +15,352 |

|

|

SFRM7 | 664,430 | 655,264 | +9,166 |

|

|

SFRU7 | 466,864 | 468,671 | -1,807 |

|

|

SFRZ7 | 412,814 | 415,045 | -2,231 |

|

|

SFRH8 | 319,101 | 315,187 | +3,914 |

|

|

SFRM8 | 228,191 | 229,327 | -1,136 |

|

|

SFRU8 | 204,307 | 206,589 | -2,282 |

|

|

SFRZ8 | 187,460 | 188,076 | -616 |

|

|

SFRH9 | 141,841 | 142,818 | -977 |

|

|

US TSY FUTURES: Mix Of Net Short Setting & Long Cover Either Side Of Weekend

OI data points to net short setting in the wings (TU, US & WN) between Thursday and Monday settlements (no settlement Friday, owing to the observance of the Independence Day holiday), while net long cover was seen in the intermediates (FV, TY & UXY).

| 07-Jul-25 | 03-Jul-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,284,274 | 4,277,341 | +6,933 | +264,155 |

FV | 7,036,363 | 7,048,798 | -12,435 | -535,942 |

TY | 4,933,016 | 4,946,323 | -13,307 | -876,149 |

UXY | 2,420,723 | 2,421,521 | -798 | -69,289 |

US | 1,834,778 | 1,819,854 | +14,924 | +2,039,424 |

WN | 1,957,701 | 1,954,856 | +2,845 | +512,560 |

|

| Total | -1,838 | +1,334,760 |

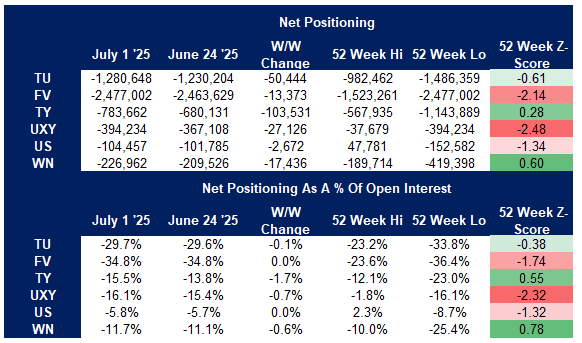

US TSY FUTURES: CFTC Shows A Managers Extend Net Long, Funds Add To Net Short

The latest CFTC CoT report showed asset manager net longs in FV, TY & UXY futures hit record levels in the week of July 1, with net longs also added in TU futures. Meanwhile, the cohort marginally trimmed net longs in both US & WN futures. Over $40mln of DV01 exposure was added to the cohort’s curve-wide net long.

- Leveraged funds added to net shorts in all contracts outside of US futures. The cohort added ~$10mln DV01 to its curve-wide net short, with net shorts in UXY futures hitting a record level.

- Broader non-commercial accounts extended net shorts across the curve (further details in the table below).

Source: MNI - Market News/CFTC/Bloomberg Finance L.P.

EUROPE ISSUANCE UPDATE:

EU dual-tranche syndication: Final terms

- E5bln (bottom of the E5-7bln range we expected) of the new 7-year Dec-32 EU-bond. Books in excess of E62bln, Spread set: MS + 35bps (guidance was MS + 37bps area).

- E4bln up from original E3bln guidance (MNI expected E3-5bln) 3.75% Oct-45 EU-bond tap. Books in excess of E72bln, Spread set: MS + 95bps (guidance was MS + 97bps area).

Netherlands auction results

- E2.055bln of the 3.25% Jan-44 Green DSL. Avg yield 3.176%.

UK auction results

- GBP0.9bln of the 1.875% Sep-49 Linker. Avg yield 2.360% (bid-to-cover 3.39x).

Austria auction results

- E978mln (E850mln allotted) of the 2.95% Feb-35 RAGB. Avg yield 3.008% (bid-to-cover 2.57x; bid-to-issue 2.24x).

- E748mln (E650mln allotted) of the 0% Oct-40 RAGB. Avg yield 3.426% (bid-to-cover 2.61x; bid-to-issue 2.27x).

Germany auction results

- Fairly subdued cover ratio at today's launch (similar to last week's 10-year Bund launch).

- E5bln (E3.754bln allotted) of the new 2.20% Oct-30 Bobl. Avg yield 2.26% (bid-to-offer 1.12x; bid-to-cover 1.49x).

UKRAINE: Kremlin Comments On Renewed US Arms Deliveries As Drones Hit 3 Cities

Speaking ahead of a dinner with Israeli PM Benjamin Netanyahu on 7 July, US President Donald Trump said that his administration would send more weapons to Ukraine, a 180-degree turn from the stance of Secretary of Defence Pete Hegseth who only days ago was reported to be the architect of a halt to the provision of military supplies to Kyiv.

- Trump said, “We’re going to send some more weapons. We have to – they have to be able to defend themselves. They’re getting hit very hard. We’re going to have to send more weapons. Defensive weapons, primarily...” Trump restates “I’m not happy with President Putin at all,” after a call between the two last week. This contrasts with his later call with Ukrainian President Volodymyr Zelenskyy, which Trump described as "very good".

- Reuters reports comments from Kremlin spox Dmitry Peskov. He says that "there are many contradictory statements" in Trump's comments and that "It will take time to clarify what weapons and in what quantity Ukraine is receiving from the US".

- In a potential effort to flatter Trump into changing his stance, Peskov says, "We believe there is wide potential for restarting trade and economic relations between Russia and the US," adding, "US sanctions on Russia are illegal, and they harm both our businesses and those of the US."

- This comes as the cities of Kharkiv, Zaporizhzhia and Odesa were hit overnight by waves of drone strikes, killing one and injuring 71 in Kharkiv, killing one in Odesa, and injuring 20 in Zaporizhzhia.

GBP/USD Trades Poorly, Tariff Headlines May be Weighing

GBP slippage in recent trade helps put GBP/USD and EUR/GBP at new daily lows/highs, with GBP now next to JPY as the poorest performer intraday. GBP/USD is within range of layered support between 1.3563-76 - the latest headlines filtering through the morning that the UK are to miss the deadline to agree to steel and aluminium tariff levels may be weighing on sentiment. But, while futures volumes are picking up as the morning progresses, cumulative activity is below average for this time of day.

- Next week's June CPI & May wages prints should prove illustrative in resolving the pricing for an August rate cut (currently just shy of 90% priced), but it's the year-end pricing that should prove more convictive for the GBP/USD trend near-term and prospects for corrective weakness toward the 1.3481 50-dma and the late June lows of 1.3371.

- Beyond these releases, the trade narrative should play an increasingly larger role - particularly as markets may be beginning to see a growing link between trade dysfunction and economic weakness in the UK - a link that proved much weaker through the first phase of USD weakness in the Trump administration.

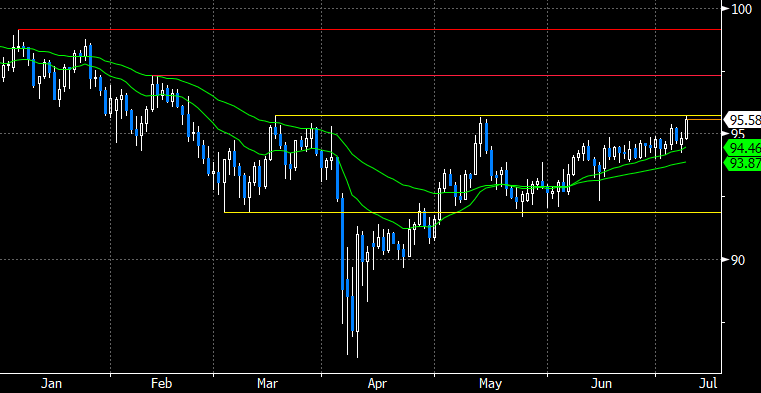

AUDJPY Approaching March Highs Following RBA Surprise

- Despite Monday’s steady move lower for AUDUSD as renewed tariff concerns filtered through to higher beta FX, today’s RBA surprise and subsequent spike higher to 0.6558 fully reversed the week’s decline. The pair has since settled around the 0.6540 mark amid a more stable equity backdrop, and it is worth noting we have ~400mln of 0.6545 expiries rolling off at today’s NY cut.

- This AUDUSD bullish trend set-up is maintained, with the latest pullback considered technically corrective. Moving average studies remain in a bull-mode position, highlighting a dominant uptrend, and scope is still seen for a climb towards 0.6603 next, the Nov 11 high. Initial firm support to watch is 0.6472, the 50-day EMA.

- Standing out on the chart is AUDJPY, which returns to an important area of resistance around 95.75 which aligns with the March and May highs from earlier in the year. Should major equity indices positively navigate the first major tariff deadline this week, the cross could see further upside targeting a move towards the February highs at 97.33. Uncertainty regarding a US/Japan trade deal and a market that remains long JPY could strengthen a short-term extension of the rally.

- Concerns over stubborn domestic inflation led the RBA board to keep the cash rate at 3.85%, in a 6-3 split decision that defied market pricing. Governor Bullock was unapologetic following the call, noting the Reserve had limited ability to influence market pricing ahead of the decision, largely due to the new board voting structure.

Source: Bloomberg Finance L.P. / MNI

FOREX: Tariff Letter Frenzy Caps USD/JPY Rally

- Trump's tariff letter-writing caught markets yesterday, prompting losses for equities and a negative close on Wall Street. Equity futures are yet to reverse, but are off the worst levels of the week headed into the crossover. The tariff headlines yesterday put paid to the USD/JPY rally that seems to have run out of steam into NY hours. That said, price remains in close proximity to 146.45, the weekly high and level above which the corrective move higher could resume. Through here, markets eye 148.03 for direction ahead of the Y149.73 200-dma.

- Triggers for a return higher in USD/JPY would be a re-widening of front-end US-Japan yield spreads or a corrective rally for the USD Index - which appears to be building a base at the recent pullback low of 96.377. While tariff uncertainties remain present, another likely delay to the installation of reciprocal tariffs to early August is keeping the USD downside argument intact, despite further warning signs over the pace of USD weakness this year - most recently via a PBOC survey issued to domestic banks earlier in the week.

- JPY is the poorest performer on the day, while AUD is the strongest. The RBA rate decision pushed back against building consensus for another rate cut by holding policy. AUD/USD trades back above 0.6500 as a result, and keeps the 50-dma support intact on any further downside.

- Following the data rush last week, there are no tier 1 releases due from the US Tuesday, although the NY Fed's latest survey on one-year inflation expectations could see some attention, expected to slow to 3.13% from 3.20%. The speaker schedule is similarly light, with just ECB's Nagel at 1500BST/1000ET.

OPTIONS: Expiries for Jul08 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600(E1.1bln), $1.1700(E1.3bln), $1.1770-80(E623mln), $1.1810(E710mln)

- USD/JPY: Y142.60-75($1.1bln), Y146.60($551mln)

- AUD/USD: $0.6435(A$646mln), $0.6545-50(A$563mln)

EQUITIES: Eurostoxx 50 Futures Remain Close to Cycle Highs

- Recent gains in Eurostoxx 50 futures from the Jun 23 low, still appears to be a potential reversal and the contract is holding on to its most recent gains. Price has pierced both the 20- and 50-day EMAs. A clear break of both averages would strengthen a reversal theme. This would open 5486.00, May 20 high and bull trigger. On the downside, a break of 5194.00, Jun 23 low, reinstates a bearish theme.

- The trend condition in S&P E-Minis is unchanged, the outlook remains bullish. Resistance at 6128.75, the Jun 11 high, has recently been breached. The break confirmed a resumption of the uptrend that started Apr 7. This has been followed by a breach of key resistance and a bull trigger at 6277.50, the Feb 21 high. Sights are on 6356.12, a Fibonacci projection. Key support is at the 50-day EMA, at 6011.49.

COMMODITIES: WTI Futures Maintain Softer Tone, But Above 50-Day EMA Support

- WTI futures maintain a softer tone following the reversal from the Jun 23 high, and recent gains appear corrective. Support to watch is the 50-day EMA, at $64.96. It has been pierced, a clear break of it would signal scope for a deeper retracement. This would expose $58.87, the May 30 low. Initial resistance to watch is $71.20, the 50.0% retracement of the Jun 23 - 24 high-low range. Key resistance is at $78.40, the Jun 23 high.

- A recent move lower in Gold resulted in a breach of the 50-day EMA, and a trendline drawn from the Dec 30 ‘24 low and connected to the Feb 28 low. A clear break of both trend tools would signal scope for a deeper correction, and open $3245.5, May 29 low. Note that the latest recovery highlights a possible false trendline break. A resumption of gains would refocus attention on $3451.3, the Jun 16 high. The bear trigger lies at $3248.7, the Jun 30 low.

| Date | GMT/Local | Impact | Country | Event |

| 08/07/2025 | - | ECB de Guindos At ECOFIN Meeting | ||

| 08/07/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 08/07/2025 | 1400/1000 | * | Ivey PMI | |

| 08/07/2025 | 1500/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 08/07/2025 | 1530/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 08/07/2025 | 1700/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 08/07/2025 | 1900/1500 | * | Consumer Credit | |

| 09/07/2025 | - | Reserve Bank of New Zealand Meeting | ||

| 09/07/2025 | 0130/0930 | *** | CPI | |

| 09/07/2025 | 0130/0930 | *** | Producer Price Index | |

| 09/07/2025 | 0200/1400 | *** | RBNZ official cash rate decision | |

| 09/07/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 09/07/2025 | 0930/1030 | BOE Financial Stability Report | ||

| 09/07/2025 | 1000/1100 | BOE FSR Press Conference | ||

| 09/07/2025 | 1045/1245 | ECB Lane At House of the Euro | ||

| 09/07/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 09/07/2025 | 1100/1300 | EC De Guindos Closing Remarks At Conference | ||

| 09/07/2025 | 1400/1000 | ** | Wholesale Trade | |

| 09/07/2025 | 1400/1000 | ** | Wholesale Trade | |

| 09/07/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 09/07/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 09/07/2025 | 1800/1400 | *** | FOMC Minutes |