MNI US Macro Weekly: Staying Calm, Carrying On

Jul-11 21:00By: Tim Cooper

Federal Reserve+ 1

Download Full Report Here

Executive Summary

- The limited set of data releases in the return from the July 4 long weekend didn’t greatly change the outlook for the US economy, reflected by almost-unchanged Fed cut pricing (still 50bp through year-end).

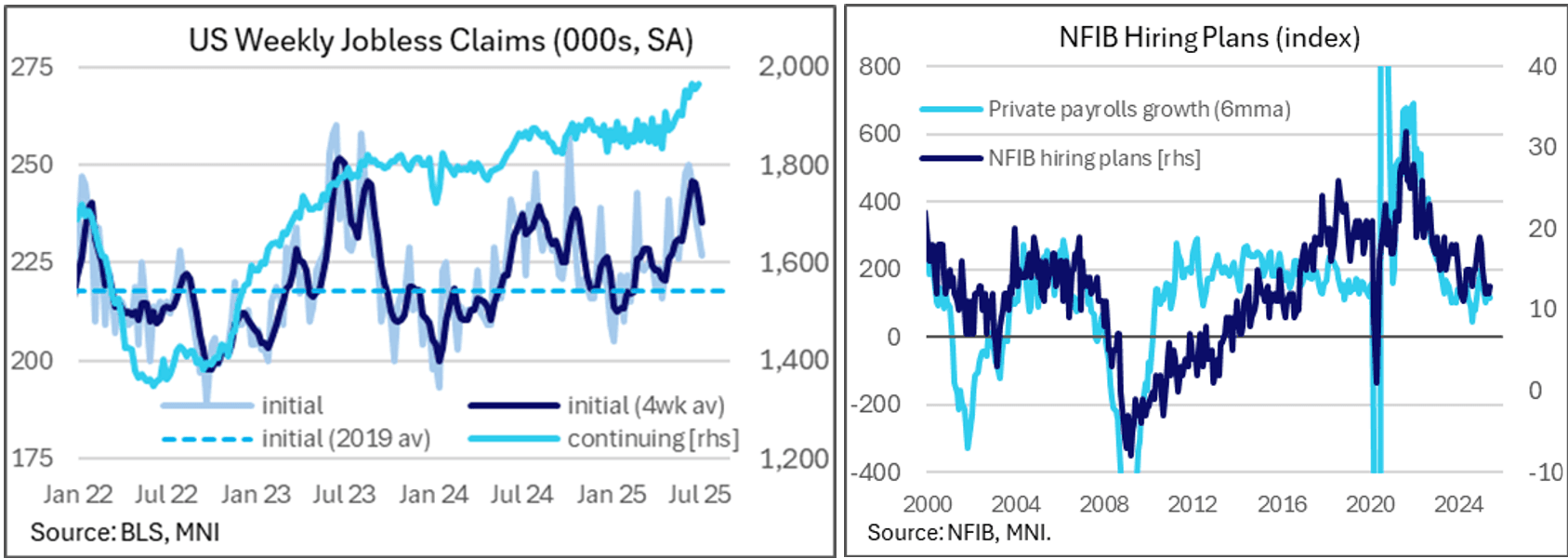

- Employment data appeared to confirm a “low firing, low hiring” labor market, and GDP growth tracking has settled in the 2-3% Q/Q SAAR area for Q2 with signs of gradual but not dramatic slowing in Q3.

- Inflation looks set to pick up in Q3 though perhaps not to as dramatic an extent as previously feared, and in the meantime, inflation expectations are not showing signs of de-anchoring.

- On the latter front, there was perhaps surprisingly little market reaction to the White House’s series of announced tariff rates including on Brazil, Canada, Japan and South Korea, some of which appeared to be higher than had been expected, not to mention a hefty 50% levy on copper imports.

- Fed speakers were limited in number but impactful. Gov Waller reiterated his call to consider a July rate cut, but also gave an extensive (and hawkish-leaning) speech on how he envisaged the future size and composition of the Fed's balance sheet – a subject that will be of growing importance in the coming months as reserves shrink amid the Treasury’s post-debt limit cash rebuild.

- St Louis Fed Pres Musalem warned of tariff inflation impacts potentially extending well into 2026, while Chicago’s Goolsbee said that the latest round of tariff announcements could push back further the Fed’s resumption of easing.

- Conversely, San Francisco's Daly confirmed at an MNI event that she sees two cuts by year-end, sounding increasingly unconcerned about the tariff impact on inflation and saying that she doesn't want to get "behind" in adjusting the policy rate.

- The main headline from the June FOMC meeting minutes was on the Committee's split on the rate outlook, which had already been encapsulated in the Dot Plot mostly split between two and zero cuts for the year. One hawkish note was that "several participants commented that the current target range for the federal funds rate may not be far above its neutral level".

- June CPI is the highlight of next week's US data slate, with MNI's early roundup of analyst expectations showing an anticipated acceleration in the main measures of inflation.

- But even a downside surprise would be unlikely to persuade the Federal Reserve to seriously consider cutting rates in July, given the expected pickup in tariff-related prices in coming months. That said, further evidence of soft price pressures would certainly help lay the groundwork for a resumption of easing in September, particularly if PCE is confirmed to be tame.

- Wednesday’s PPI will refine the post-CPI estimate of PCE. We also have a busy Thursday for data with June Retail Sales alongside the customary weekly jobless claims report.