MNI US Inflation Insight: Soft Services Offset Tariff Hints

Jun-12 19:22By: Tim Cooper and 1 more...

Inflation+ 1

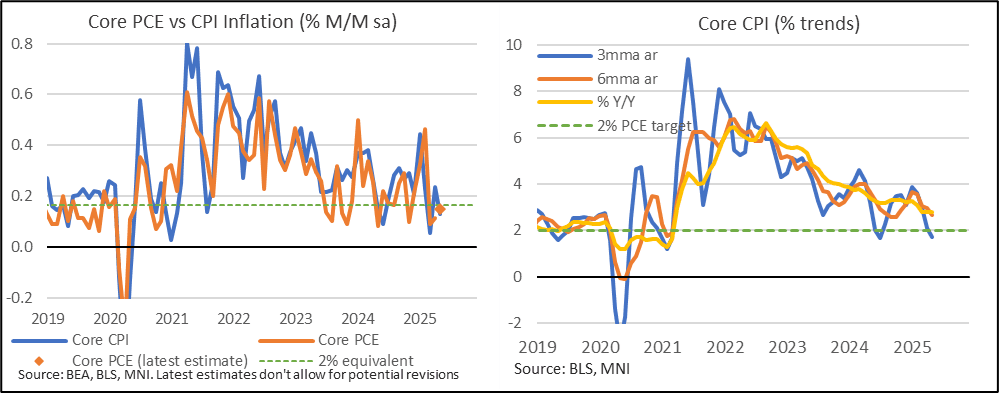

Surprising Weakness Sees Core PCE On Track For Another Soft Print

- Core CPI inflation was notably softer than expected in May at a seasonally adjusted 0.13% M/M.

- There were downside surprises across the major categories, with core goods and both housing and non-housing services.

- Core goods details did show some increased signs of tariff increases but they were clouded by declines for both new & used vehicles and, more surprisingly, apparel.

- Accordingly, the Y/Y surprised lower at an unchanged 2.8% Y/Y whilst the six-month trend rate eased from 3.0% to 2.65% annualized. That’s the first time the six-month rate has been softer than the Y/Y since December, having been as much as 0.4pp higher in Jan and Feb.

- PPI inflation on Thursday then saw largely benign trends even if trade margins bounced back.

- The PCE-relevant components of PPI were largely neutral on the month after a heavy drag in April.

- Core PCE is currently expected to come in at 0.14-0.15% M/M for May.

- It is however, too soon to determine tariff inflation implications, with larger increases expected to filter through in June and July.

- Overall versus pre-CPI, 2025 cumulative Fed cut pricing has deepened 11bp to 53bp –briefly hitting 56bp post-PPI. The next cut is just about priced by September (23+bp, over 90% probability), vs October prior.