US: MNI POLITICAL RISK - Democrats Launch New Offensive On Border

May-24 12:21

- Senate Majority Leader Chuck Schumer's (D-NY) failed effort to advance a bipartisan border security bill provides cover for vulnerable Democrats and a platform for President Biden to argue he has engaged credibly in efforts to secure the border.

- US Treasury Secretary Janet Yellen noted that “substantial increases” in living costs are a “problem to a lot of people,” as voters hammer Biden on the assumption he has tools avaiable to control inflation.

- Crypo's big week in Congress continued with House of Representatives approval of legislation barring the Federal Reserve from issuing a central bank digital currency without explicit authorization from Congress.

- President Biden and Kenyan President William Ruto announced an upgrade to bilateral relations during Ruto’s White House State Visit.

- The US is expected to unveil a new USD$275 million package of military aid for Ukraine today as Kyiv struggles to contain a Russian offensive and pressure mounts for the White House to approve Ukrinaian strikes within Russian terrority.

- House Speaker Mike Johnson (R-LA) will "soon" invite Israeli Prime Minister Benajamin Netanyahu to address a joint meeting of Congress.

- Secretary of State Antony Blinken is preparing actions against Georgian lawmakers for passing a ‘foreign influence’ law which would, “stifle” freedom and “impede independent media organizations.”

- Poll of the Day: The presidential race is a deadheat when undecided voters are pressed to decided between Biden and Trump.

Full Article: US Daily Brief

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

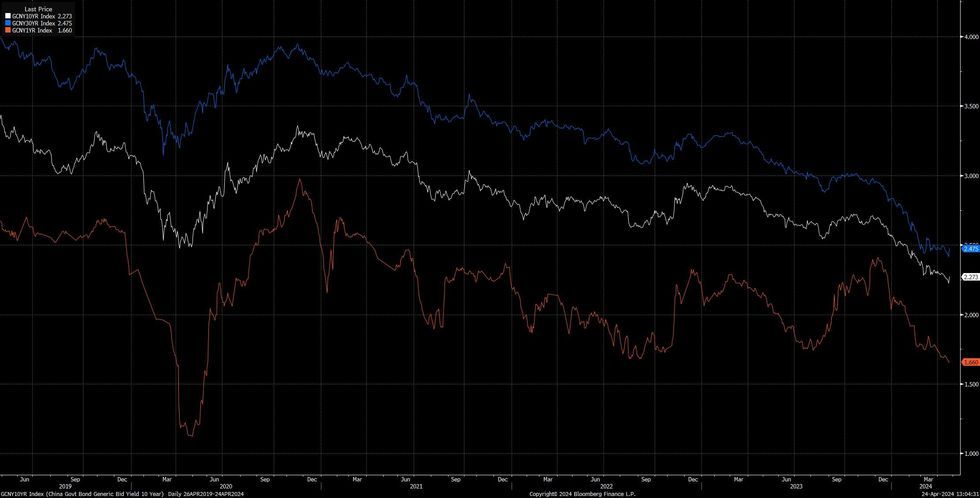

CHINA RATES: Goldman Take Profit On Long CGB Trade Following Policymaker Comms Matching MNI Reports

Apr-24 12:19

Goldman Sachs view “active CGB trading as part of the PBOC's regular open market operation toolbox, rather than QE.”

- They suggest that active CGB trading may mean that “policymakers gain better control of market interest rates, and thus reduce the risk of unintended over-tightening/loosening of financial conditions.”

- They also believe “the upcoming acceleration of government bond issuance implies limited room for further decline in market rates in the near term.”

- The recent policymaker communique on this front shouldn't be a surprise to MNI subscribers. A recent exclusive from our Beijing team (published on April 11) noted that the PBoC will “continue to monitor the longer-dated Chinese government bond market, adding supply and control over leverage to help guide 10-Year CGB yields closer to the present 2.50% one-year MLF rate.”

- Goldman go on to flag that “paying front-end IRS would provide some protection against tighter front-end liquidity conditions due to the likely large volume of government bond supply in the coming months.”

- Finally, they take profit on their long 1-Year CGB trade recommendation for a potential gain of 60bps (entered on 10 November ‘23).

- This comes after CGB yields moved off cycle lows following Tuesday's comments from policymakers.

Fig. 1: China 1-, 10- & 30-Year Yields (%)

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

JPY: USDJPY breaks above 155.00

Apr-24 12:18

- USDJPY is now testing that 155.00 handle.

- Starting to see further upside momentum and eyeing next immediate resistance at 155.29 1.764 proj of the Feb 1 - 13 - Mar 8 price swing, so far printed a 155.17 high.

US: MNI POLITICAL RISK - Blinken To Strike Delicate Balance In China

Apr-24 12:10

- The Senate yesterday overwhelmingly passed a USD$95 billion aid package for Ukraine, Israel, and the Indo-Pacific. The package also includes language requiring Chinese company ByteDance to divest from TikTok, authorises the seizure of Russian sovereign assets, and a calls for range of new sanctions on Iran’s oil sector - including the expansion of secondary sanctions to cover Chinese transactions in Iranian crude oil.

- The Pentagon is preparing a roughly USD$1 billion package of military aid to be dispatched to Ukraine after President Biden signs the bill into law today.

- Secretary of State Antony Blinken arrived in China today for a challenging trip designed to dial-down tensions and convey a raft of concerns including Chinese support for Russia, Chinese industrial overcapacity, and confrontational Chinese naval actions in the South China Sea.

- The Federal Trade Commission yesterday finalised broad regulations banning most non-compete clauses in employment contracts. The rule is expected to come into effect in August.

- Former GOP presidential candidate Nikki Haley received 17% of the vote share in the Pennsylvania presidential primary yesterday - a warning sign for former President Donald Trump.

- A new survey of swing states has found that Biden’s recent polling bump in key battleground states, “has mostly evaporated as a deep current of pessimism about the trajectory of the US economy hurts his standing with voters.”

- Poll of the Day: Americans say, “limiting the power and influence of Russia and China,” are the US’ top long-term foreign policy priorities.

Full article: US Daily Brief