FED: MNI Fed Preview-June 2025: Dividing Lines

Our July Fed preview has just been published - Download Full Report Here

- With the Fed almost certain to hold the funds rate at 4.25-4.50% again at the July 29-30 meeting, focus will be on the degree to which the Committee signals openness to rate cuts resuming in the fall.

- The policy statement is unlikely to see meaningful changes, though Governor Waller and Vice Chair Bowman are widely expected to dissent in favor of a rate cut.

- The message from July is likely to look similar to that of June: a fairly divided Committee retains its overall easing bias but individual participants need varying degrees of certainty before supporting a resumption of the easing cycle.

- Chair Powell is likely to repeat many of his messages from the prior meeting, noting that the Committee's median expectation is for two cuts by year-end albeit dependent on the data in the interim.

- He is likely to point out that the Committee will see two inflation and employment reports by the next meeting in September, with more clarity on the impact of tariffs on consumer prices and activity, and potentially less uncertainty over the policy outlook.

- In other words, the patient approach remains, but the September meeting will the most “live” so far this year.

- Apart from the current thinking on a September cut, areas of interest for the press conference include whether the Committee’s view on neutral rates has shifted, and whether Fed balance sheet management was discussed.

- MNI’s separate preview of sell-side analyst summaries to follow on Monday Jul 28

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

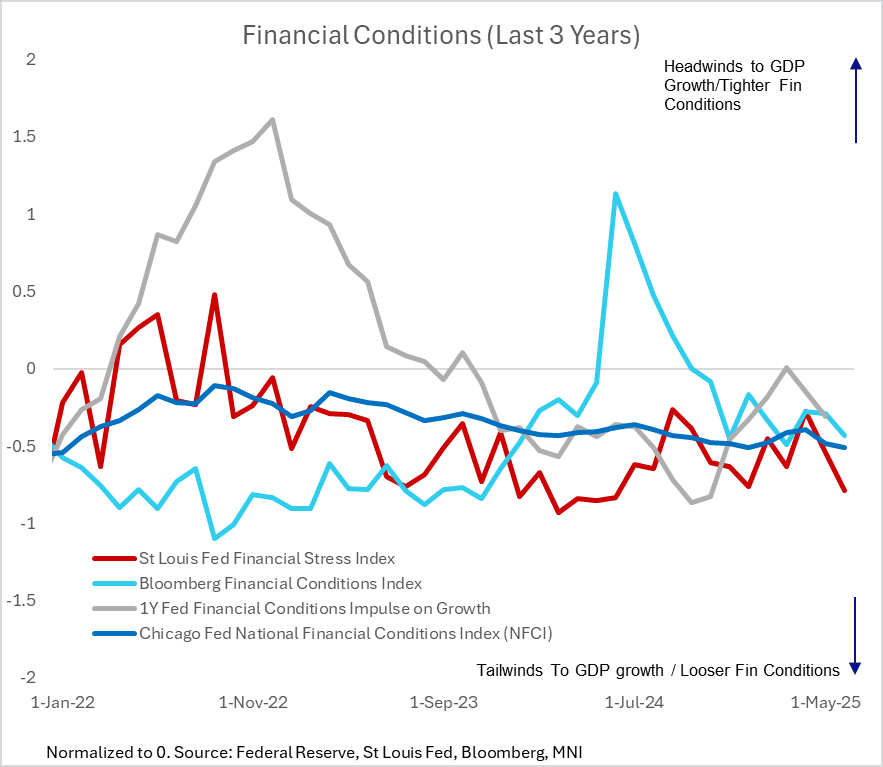

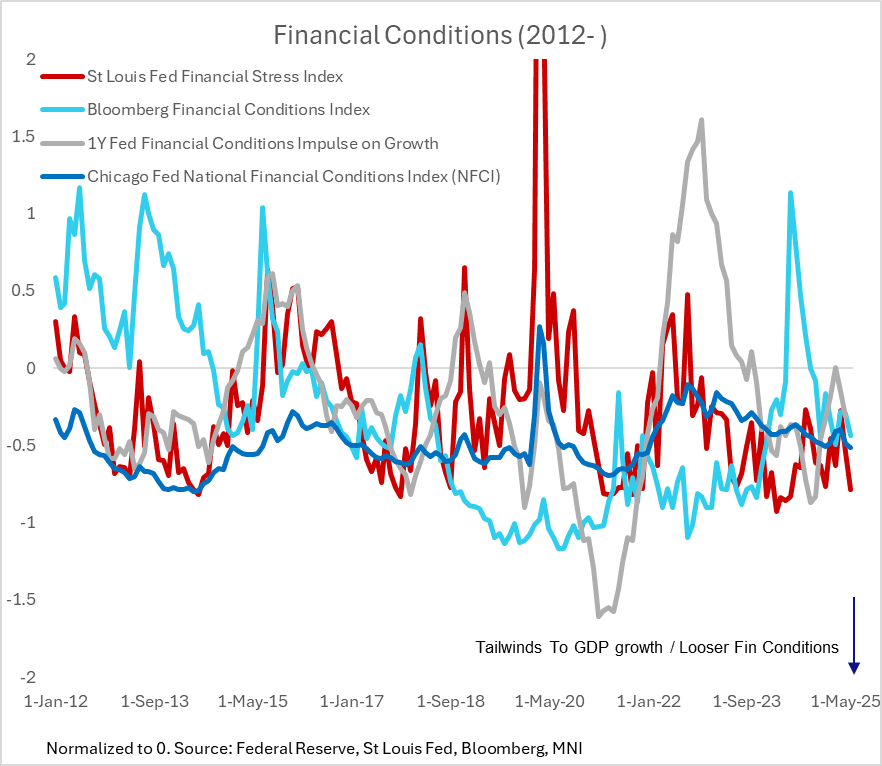

US: Financial Conditions Ease Since April

The Chicago Fed's National Financial Conditions Index (NFCI) was unchanged at –0.51 in the week ending June 20 in the latest update out today. This marks the "easiest" financial conditions since early 2022 by this measure ("negative values have been historically associated with looser-than-average financial conditions").

- The NFCI didn't really show that much tightness through the April equity / bond sell-off, merely returning to August 2024 levels. That's similar to other metrics such as Bloomberg's FCI, and echoes the St Louis Fed's Financial Stress index which has similarly retraced in an easing direction since April.

- The Fed's own financial conditions estimates - also updated today - barely got back to the "zero" level in March indicating financial conditions becoming a headwind to growth - the 1-year lookback impulse on growth was as "loose" in May as it's been in 4 months.

- Most FOMC participants describe current policy as "moderately/modestly/slightly" restrictive, with some eyeing policy as being increasingly close to neutral already. While restrictiveness does appear in some segments of the economy (most prominently housing), the broader scope of financial conditions certainly don't suggest any undue tightness.

USDCAD TECHS: Gains Considered Corrective

- RES 4: 1.4111 High Apr 4

- RES 3: 1.4016 High May 12 and 13 and a key resistance

- RES 2: 1.3920 High May 21

- RES 1: 1.3821 50-day EMA

- PRICE: 1.3748 @ 16:49 BST Jun 25

- SUP 1: 1.3635 Low Jun 18

- SUP 2: 1.3540/3534 Low Jun 16 / 1.0% 10-dma envelope

- SUP 3: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

- SUP 4: 1.3473 Low Oct 2 2024

A primary downtrend in USDCAD remains intact and short-term gains are considered corrective. Resistance at the 20-day EMA, at 1.3713, has been breached. A continuation higher would signal scope for a stronger retracement. Pivot resistance to monitor is at the 50-day EMA, at 1.3821. Key support and the bear trigger has been defined at 1.3540, the Jun 16 low. Clearance of this price point would resume the downtrend.

US TSYS: Treasury Curves Twist Steeper, Fed SLR Proposal Eases Bank Rules

- Treasury futures gradually climbed off midmorning lows after the bell, curves twisting steeper (2s10s +4.186 at 50.911) after the Fed SLR proposal to ease rules for large banks.

- Projected rate cut pricing gains slightly vs. early morning levels (*): Jul'25 at -6.2bp (-5.2bp), Sep'25 at -27.1bp (-25.8bp), Oct'25 at -42.7bp (-41.2bp), Dec'25 at -60.9bp (-59.7bp).

- Near the top end of a narrow session range, the Tsy Sep'25 10Y contract trades +2 at 111-23 (111-11.5L / 111-24H), volume just over 1.1M, 10Y yield -.0078 at 4.2867%. Key resistance remains above the intraday high of 111-24 at 111-30/31.5 (76.4% of May 1-22 downleg / 1.0% 10-dma envelope.)

- New home sales fell to an 18-month low in May, with the 13.7% M/M drop to 623k (seasonally-adjusted, annual rate) adding to evidence that overall US housing market activity is deteriorating.

- Cross asset: stocks flat to mixed (SPX eminis +1.75 at 6148.0; DJIA -101.5 at 42987.5, Nasdaq +48.77 at 19961.30), crude firmer after two day rout (WTI +.75 at 65.12), Gold firmer (+10.34 at 3334.01). After clinging to near steady at midday, the dollar index withdrew in the second half, nearing the prior session's 1W low (BBDXY -2.29 at 1199.24). Despite yesterday’s pullback, EURJPY has recovered strongly on Wednesday, rising 0.55% and back above 169.25.

- Heavy data tomorrow: weekly claims, GDP, Personal Consumption, Pending Home Sales, followed by several scheduled Fed speakers.