MNI Fed Preview-July 2025: Dividing Lines (Re-Send)

Jul-25 20:53By: Tim Cooper

US

(Re-sending with correct title)

Download Full Report Here

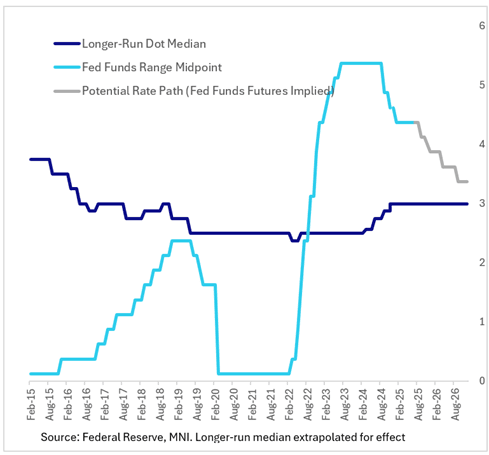

- With the Fed almost certain to hold the funds rate at 4.25-4.50% again at the July 29-30 meeting, focus will be on the degree to which the Committee signals openness to rate cuts resuming in the fall.

- The policy statement is unlikely to see meaningful changes, though Governor Waller and Vice Chair Bowman are widely expected to dissent in favor of a rate cut.

- The message from July is likely to look similar to that of June: a fairly divided Committee retains its overall easing bias but individual participants need varying degrees of certainty before supporting a resumption of the easing cycle.

- Chair Powell is likely to repeat many of his messages from the prior meeting, noting that the Committee's median expectation is for two cuts by year-end albeit dependent on the data in the interim.

- He is likely to point out that the Committee will see two inflation and employment reports by the next meeting in September, with more clarity on the impact of tariffs on consumer prices and activity, and potentially less uncertainty over the policy outlook.

- In other words, the patient approach remains, but the September meeting will the most “live” so far this year.

- Apart from the current thinking on a September cut, areas of interest for the press conference include whether the Committee’s view on neutral rates has shifted, and whether Fed balance sheet management was discussed.

MNI’s separate preview of sell-side analyst summaries to follow on Monday Jul 28