MNI Eurozone Apr HICP Preview: Unwinding of Easter Effect Key

May-29 11:30By: Emil Lundh and 2 more...

Inflation

DOWNLOAD FULL PDF HERE: May2025EZCPIPreview.pdf

EXECUTIVE SUMMARY

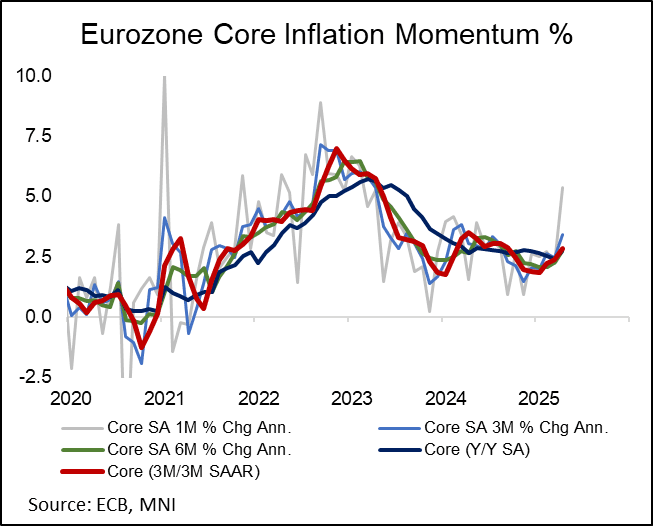

- Tariff developments remain the centre of market attention, but the Eurozone May flash inflation round will still be in focus to determine to what extent the April acceleration in services inflation was temporary.

- The details of the April reading pointed to a substantial “Easter effect” for travel-sensitive services such as airfares, and already released French and Belgian data point to an unwind of these dynamics.

- The French data was notably soft, printing at 0.6% Y/Y (vs 0.9% cons and prior), and added downside risks to MNI’s current consensus for the Eurozone, which stands at 2.0% for headline (vs 2.2% prior) and 2.5% for core (vs 2.7% prior).

- In the near-term, the combination of tariff-related downside growth risks and easing wage pressures are expected to weigh on core inflation, but there remains some uncertainty around the medium-term impacts, particularly amongst Governing Council hawks.

Trending Top

Mar-27 20:13