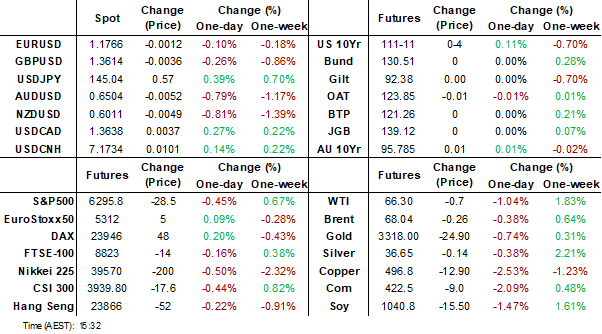

MNI EUROPEAN MARKETS ANALYSIS: USD Up Ahead Of Tariff Deadline

- The USD is firmer as the tariff deadline approaches. AUD and NZD are the weakest performers in the G10 space, while EM FX has been weighed by a fresh Trump tariff threat for BRICs aligned countries.

- US Tsy yields have returned and moved lower after the long weekend. RBA-dated OIS pricing is slightly softer across meetings. A 25bp rate cut this week is given a 94% probability, with a cumulative 79bps of easing priced by year-end.

- Japan wages data was well below expectations, with slumping bonus payments a headwind.

- It's a fairly quiet start to the week data wise, with a few EU related releases on tap. Most focus is likely to rest on trade/tariff related headlines.

MARKETS

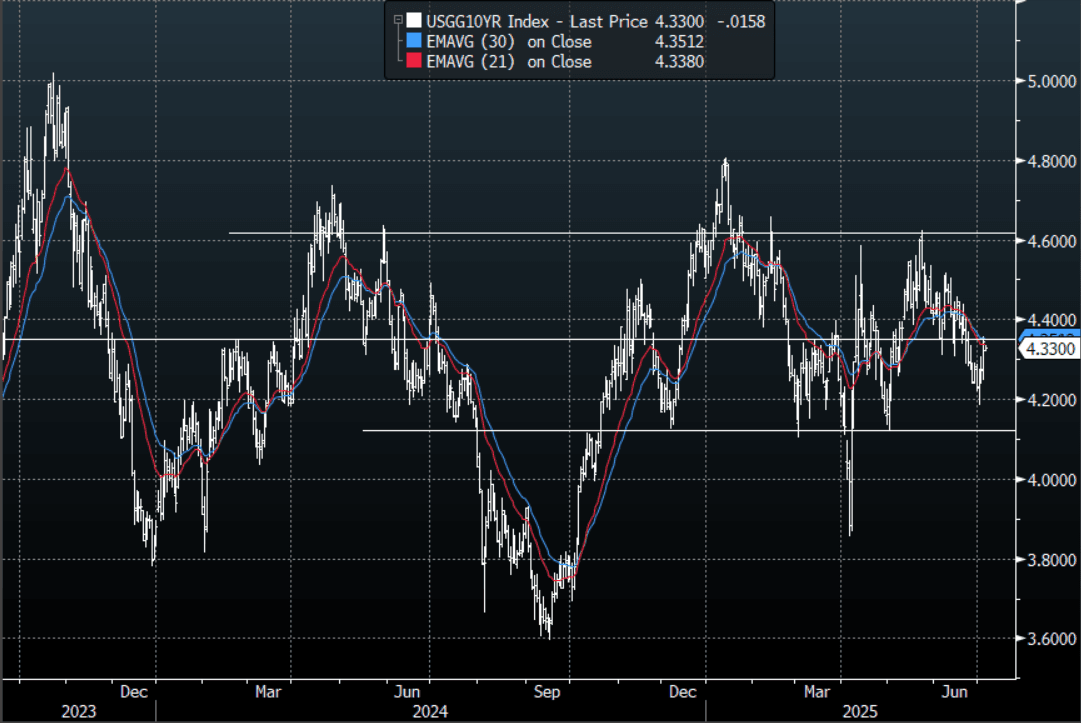

US TSYS: Asia Wrap - Yields Open Lower After Long Weekend

The TYU5 range has been 111-08+ to 111-12+ during the Asia-Pacific session. It last changed hands at 111-10+, up 0-03+ from the previous close.

- The US 2-year yield has moved lower trading around 3.855%, down 0.02 from its close.

- The US 10-year yield has edged lower trading around 4.33%, down 0.02 from its close.

- The 10-year yield saw a strong bounce in reaction to the better NFP print. This 4.35/40% area offers those who would like to express a long the opportunity to fade. A sustained close back above 4.40/4.45% area though would not be great for the bulls and would see more of the longs prepared back.

- US President Trump has posted via Truth Social that the US will start delivering letters outlining tariff levels to various countries starting 12pm Monday, US eastern time. Trade deals will also be announced at the same time.

- (Bloomberg) -- The Treasury’s willingness to fund more at the short-end of the yield curve will further compromise the Federal Reserve’s independence and increasingly leave monetary policy de facto in fiscal hands. The dollar will be a casualty, and the yield curve will steepen.

- Data/Events: Bond investors will be focusing on the Fed Minutes and the demand for 10 & 30-year maturities this week.

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Sharp Bear-Steepener, Fiscal Expansion Fears, 5Y Supply Tomorrow

JGB futures are little changed, -2 compared to settlement levels.

- Japan’s leading economic indicator was at 105.3 in May versus 104.2 in April.

- Bloomberg - "Japanese Prime Minister Shigeru Ishiba said the country is prepared for all possible tariff scenarios, speaking on Fuji TV's "Sunday News The Prime" program. Japan is ready to "stand firm" and defend its interests while anticipating every possible situation, says Ishiba."

- Cash US tsys are flat to 3bps richer in today's Asia-Pac session after resuming trading following the long weekend.

- (Bloomberg) The Treasury's willingness to fund more at the short end of the yield curve will further compromise the Federal Reserve's independence and increasingly leave monetary policy de facto in fiscal hands.

- Cash JGBs are -1bp richer to 8bps cheaper across benchmarks, with a steeper curve. The benchmark 5-year yield is 0.2bp higher at 0.973% ahead of tomorrow's supply.

- (Bloomberg) -- Ryutaro Kimura, senior fixed income strategist at AXA Investment Managers, said that fiscal expansion worries have weighed on Japanese government debt since the 30-year bond auction on July 3, and super-long-term bonds have sold off sharply.

- The swaps curve has bear-steepened, with rates flat to 5bps higher.

- Tomorrow, the local calendar will see Trade Balance and Bank Lending data alongside 5-year supply.

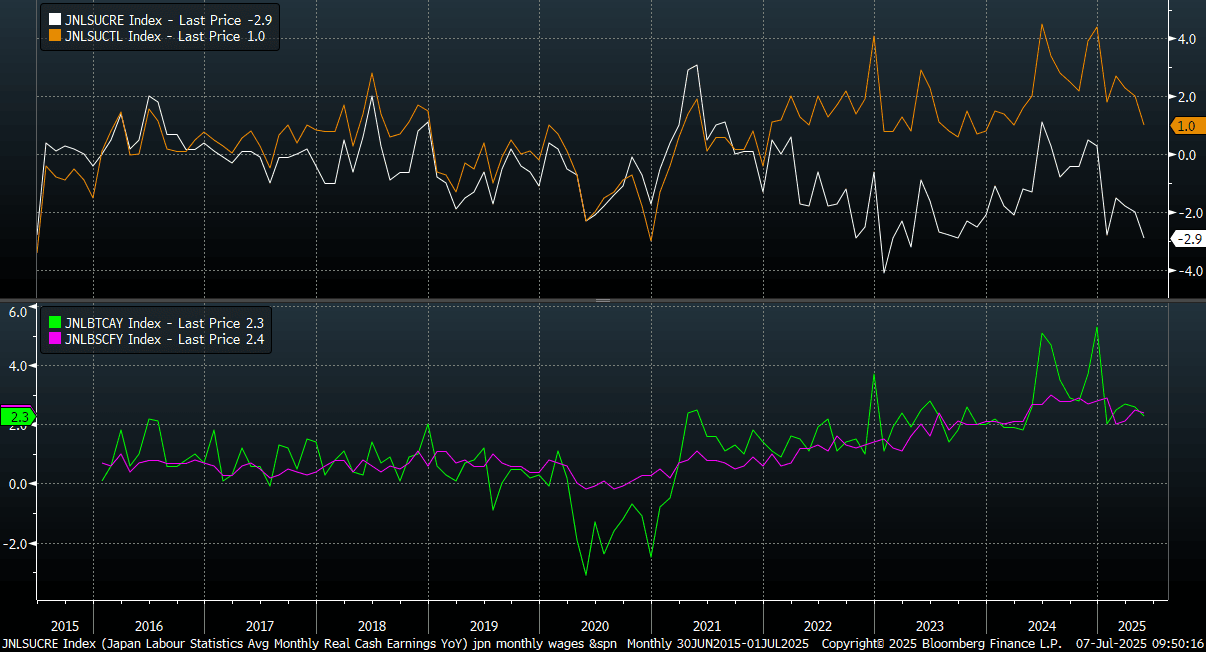

JAPAN DATA: Wages Weaker Than Forecast, Weighed By Bonus Payment Slump

Japan May labor cash earnings were weaker than forecast. Headline nominal cash earnings rose 1.0%y/y, versus a 2.4% forecast. The prior April outcome was also revised down to a 2.0% rise (initially reported as a 2.3 % gain). In real terms, earnings were down -2.9%y/y, against a -1.7% forecast and prior -2.0% outcome. For nominal earnings this is weakest outcome since Mar 2024, while in real terms it is back to Sep 2023 lows. See the top panel of the chart below. It also widens the trend with last Friday's stronger real household spending outcome.

- A slump in bonus payments, down -18.7%y/y, weighed on the headline results. Contracted and scheduled pay in y/y terms were little changed versus April levels. Bonus payments tend to be quite volatile (we were at +74.1%y/y in Feb), so there is scope for this to be less of a headwind in months ahead.

- On a same sample base, cash earnings were +2.3%y/y, below the 2.8% forecast and 2.6% prior outcome. Scheduled full time pay (on a same base) rose 2.4%y/y, also below market expectations (2.6% was the forecast and 2.5% printed in April). See the bottom panel of the chart below. These trends are more positive compared to the headline earning outcomes, but sit off 2024 highs.

- In this segment, special payments also fell 3.6%y/y, versus a +2% gain in April. Again, there is scope for this to be less of a headwind going forward.

- All in all, given the contribution of bonus payments to the headline fall it softens the negative message from today's print. The BoJ still have time on its hands to assess wages trends, with the near term bias likely to see rates left on hold.

Fig 1: Japan Labor Earnings Slowed In May, As Bonus Payments Fell

Source: Bloomberg Finance L.P/MNI

AUSSIE BONDS: Slightly Stronger, Subdued Session, RBA Policy Decision Tomorrow

ACGBs (YM +1.0 & XM +0.5) are slightly stronger ahead of tomorrow’s RBA Policy Decision.

- The RBA is widely expected to cut by 25bps. This is the sell-side consensus, albeit with a small number of economists expecting rates to be left on hold.

- May monthly CPI data should give the RBA confidence to cut. Headline inflation was close to the bottom end of the RBA's 2-3% target band, whilst the trimmed mean eased to 2.4%y/y. Services inflation is still running at a stronger pace, but we continue to move off recent highs for this sub-sector of inflation.

- RBA-dated OIS pricing is slightly softer across meetings. A 25bp rate cut this week is given a 94% probability, with a cumulative 79bps of easing priced by year-end. Notably, today's moves leave meetings pricing 15-32bps softer than levels before the May RBA Meeting.

- Cash US tsys are 1-3bps richer in today's Asia-Pac session after resuming trading following the long weekend.

- Cash ACGBs are 1bp richer with the AU-US 10-year yield differential at -15bps.

- The bills strip is little changed.

- This week, the AOFM plans to sell A$1200mn of the 4.25% 21 December 2035 bond on Wednesday and A$1000mn of the 2.75% 21 November 2029 bond on Friday.

RBA: MNI RBA Preview-July 2025: 25bps Cut Likely

- The RBA is widely expected to cut by 25bps at tomorrow’s policy meeting. This is the sell-side consensus, albeit with a small number of economists expecting rates to be left on hold. Financial market pricing is also consistent with a 25bps cut. Our bias is also for a 25bps cut, which would take the RBA cash rate to 3.60% (still above neutral rates). If realized this would be 75bps worth of easing delivered so far in this cycle.

- Data towards the end of June, for May monthly CPI, should give the RBA confidence to cut. Headline inflation was close to the bottom end of the RBA’s 2-3% target band, whilst the trimmed mean eased to 2.4%y/y. Services inflation is still running at a stronger pace, but we continue to move off recent highs for this sub-sector of inflation.

- Some focus will be on the language the RBA uses and whether it considers a 50bps cut or not (assuming a 25bps cut is delivered). We feel the most likely scenario for the RBA board will be to consider holding steady or a 25bps cut. International risks are now arguably lower compared to the first part of Q2. This outlook can change quite quickly, but at the current juncture there are likely to be less fears around the global outlook.

- See this link for the full preview.

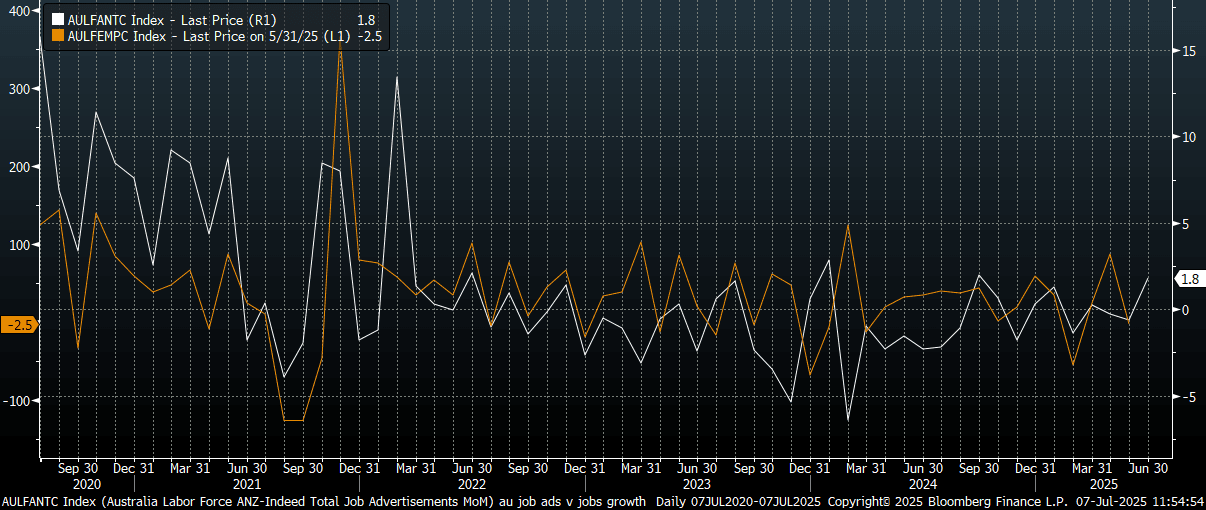

AUSTRALIA DATA: ANZ Job Ads Rise In June, Pointing To Resilient Labor Market

The ANZ June job ads print was +1.8%m/m, after a revised fall of 0.6% in May (originally reported as a -1.2% decline). In y/y terms, jobs ads are -0.4%. At the start of the year we were at -13.7%. This was the best m/m increase for the index since Sep last year. It points to continued resilience in terms of labor market conditions. The chart below plots the ANZ job ads m/m change versus monthly employment growth in Australia.

- The RBA meets tomorrow, with a 25bps cut widely expected. The central bank is likely to continue to emphasize the tight labor market, but this is unlikely to be enough to offset greater comfort around inflation trends, which should see them ease further.

Fig 1: ANZ Job Ads Post Solid Rise in June

Source: Bloomberg Finance L.P/ANZ/MNI

BONDS: NZGBS: Closed Slightly Richer, RBNZ Policy Decision On Wednesday

NZGBs closed mid-range, 2bps richer.

- Cash US tsys are flat to 3bps richer in today's Asia-Pac session after resuming trading following the long weekend.

- Swap rates closed 1-2bps lower.

- Tomorrow, the local calendar will be empty, with the next major event on the calendar being the RBNZ Monetary Policy Review on Wednesday.

- A majority of members in the NZIER Monetary Policy Shadow Board recommend that the RBNZ keep the cash rate on hold at 3.25%.

- RBNZ dated OIS pricing is little changed across meetings today. 3bps of easing is priced for this week's meeting, with a cumulative 31bps by November 2025.

- Notably, pricing is 9-15bps firmer across 2025 meetings compared to pre-RBNZ decision levels on May 28

- (Bloomberg) RBNZ Chief Economist Paul Conway will give a speech about global tariffs on July 24, from 1:30 pm in Wellington, the central bank says in an emailed advisory. Speech will cover the various ways global tariffs will impact us here in New Zealand, and how the RBNZ is thinking through the impacts on inflation and the economy more broadly.

- On Thursday, the NZ Treasury plans to sell NZ$250mn of the 3.00% Apr-29 bond and NZ$200mn of the 4.50% May-35 bond.

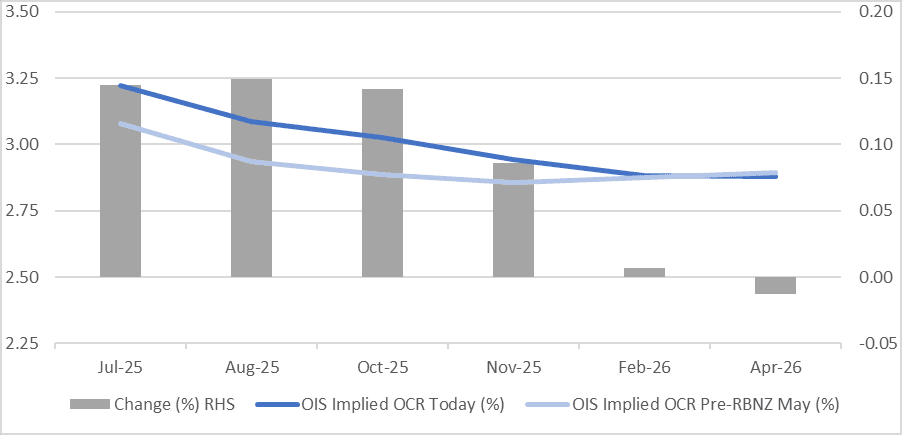

STIR: RBNZ-Dated OIS Firmer Than Pre-RBNZ Decision Levels (May)

RBNZ dated OIS pricing is little changed across meetings today. 3bps of easing is priced for this week's meeting, with a cumulative 31bps by November 2025.

- Notably, pricing is 9-15bps firmer across 2025 meetings compared to pre-RBNZ decision levels on May 28.

- (Bloomberg) -- A majority of members in the NZIER Monetary Policy Shadow Board recommend that the Reserve Bank of New Zealand keep the cash rate on hold at 3.25% at the July 9 review. While activity remains soft in the New Zealand economy, there are both upside and downside risks to inflation in the near term, given the recent pick-up in annual CPI inflation and heightened global risks.

Figure 1: RBNZ Dated OIS Today vs. Pre-May RBNZ Decision Levels (%)

Source: MNI - Market News / Bloomberg

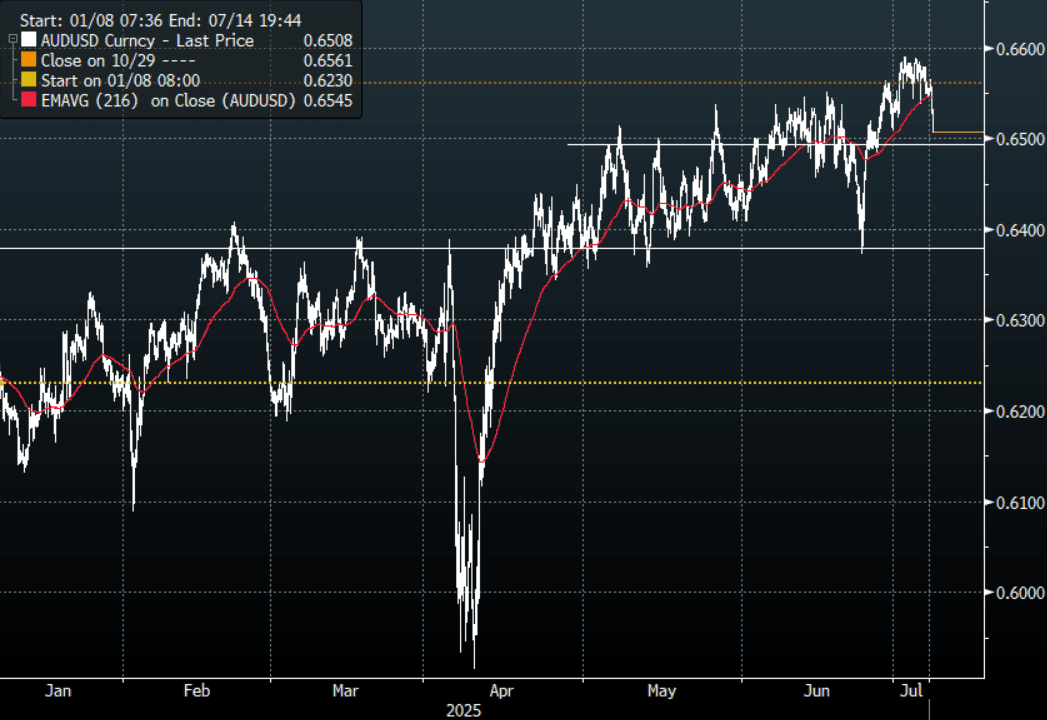

AUD: Asia Wrap - AUD/USD Trades Heavy As Market Eyes Tariff Deadline

The AUD/USD had a range Friday night of 0.6507- 0.6565, Asia is trading around 0.6510. The AUD/USD drifted off the 0.6600 area once again as stocks pared back some of its recent gains as the market eyes the tariff deadline approaching this week. Look for more consolidation again in the AUD/USD as the pair continues to try build a base from which to move higher. The risk to this is clearly around President Trump escalating trade tensions this week, which could make it a choppy week. First support is towards 0.6500 then more importantly the 0.6350/0.6400 area.

- (Bloomberg) -- “Australia’s May spending data presents a conundrum — are consumers struggling, or thriving? Weak retail trade data on Wednesday suggests consumers, plagued by uncertainty, are keeping their wallets shut. Stronger-than-expected broader spending data on Friday shows a weather-related pickup in winter clothes shopping was complemented by a discretionary surge in car sales and hospitality spending.”

- The AUD/USD is attempting to break through the top of its recent range as the pressure on the USD increases. The move higher does seem to be stalling though as the market eyes the tariff deadline. First support is towards 0.6500 then more importantly the 0.6350/0.6400 area.

- The AUD needs a sustained break above 0.6600 to potentially start building momentum for an extended move higher, a close back above 0.6600 and the focus would turn back to 0.6900/0.7000.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD884m), 0.6500(AUD 510m), 0.6700(AUD 652m). Upcoming Close Strikes : 0.6650(AUD857m July 10), 0.6375(AUD722m July 8)

Fig 1: AUD/USD spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

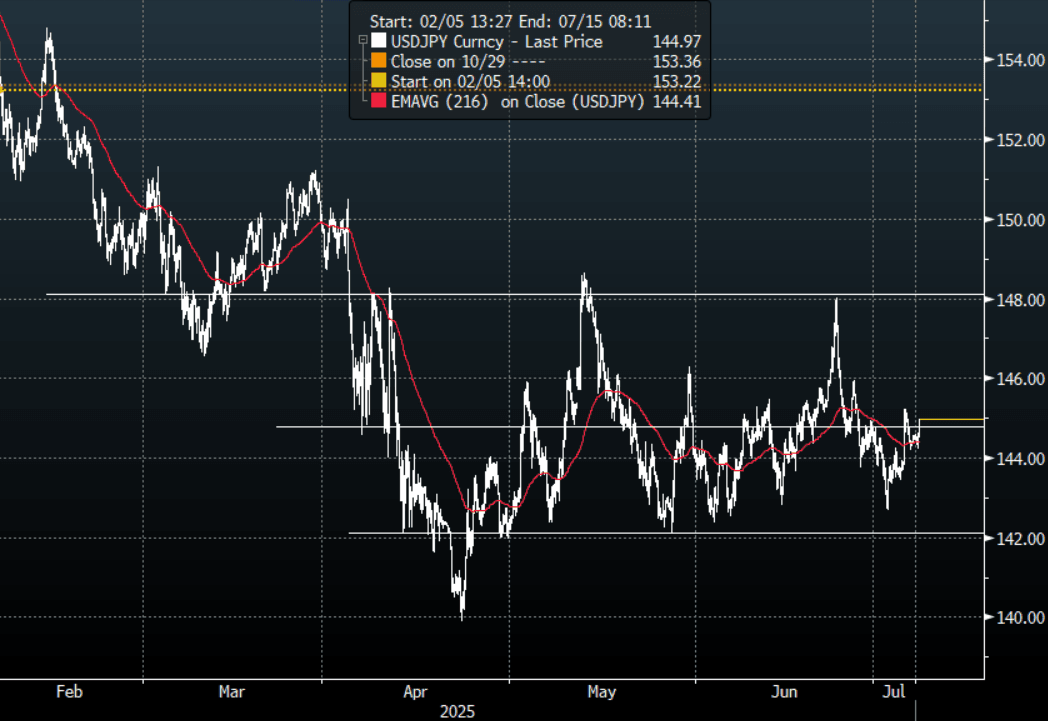

JPY: Asia Wrap - USD/JPY Finds Demand, Still Trades In The Middle Of Its Range

The Asia-Pac USD/JPY range has been 144.23 - 144.99, Asia is currently trading around 144.95, +0.35% having found decent demand back towards the 144.20 area in our session. Price is now back in the middle of the wider 142.00 - 148.00 range and the pair will probably continue to take its cue from the US rates market which opened again this morning after the long weekend.

- MNI Brief: Japan’s May Negative Real Wage Widens. Japan’s inflation-adjusted real wages, a key gauge of household purchasing power, remained negative for the fifth straight month in May, falling 2.9% y/y following April’s 2.0% decline, preliminary data from the Ministry of /health, Labour and Welfare showed Monday. The drop marks the steepest decline since September 2023, when real wages also fell 2.9%.

- Bloomberg - “Japanese Prime Minister Shigeru Ishiba said the country is prepared for all possible tariff scenarios, speaking on Fuji TV’s “Sunday News The Prime” program. Japan is ready to “stand firm” and defend its interests while anticipating every possible situation, says Ishiba.”

- “We will be pushing for zero tariffs on automobiles," Ishiba adds. He notes that Japan is the largest investor in the US and the biggest job creator there.”

- "AOKI: JAPAN, US CONTINUING ACTIVE TARIFF DISCUSSIONS”- BBG

- The rejection of 148.00 points to a potential top being in place now and shows just how quick the market is to return to selling USD’s. USD/JPY was looking for a fresh catalyst to probe the lower end of its range again but NFP did not provide that so we are now back in the middle of the range. The JPY bulls will be hoping the move higher in US yields is capped as a break higher in rates would begin to make a long JPY market vulnerable with its preference to express a short.

- Options : Close significant option expiries for NY cut, based on DTCC data: 143.85($550m).Upcoming Close Strikes : 144.50($840m July9), 142.75(AUD$855m July8).

Fig 1 : USD/JPY Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

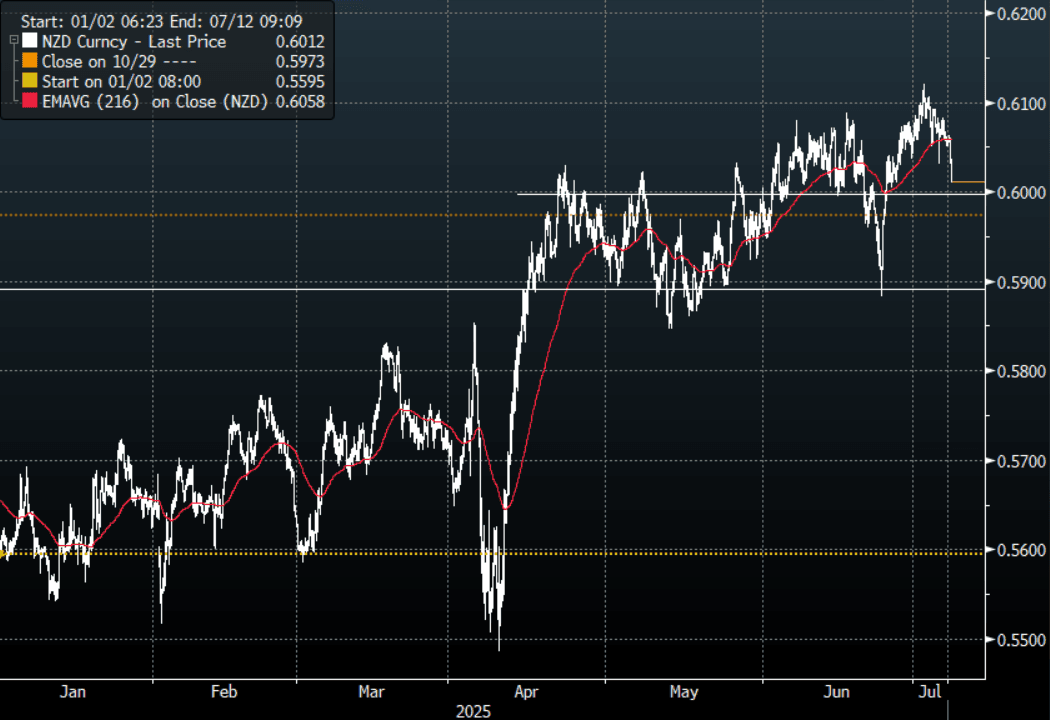

NZD: Asia Wrap - NZD/USD Trades Soft As Risk Eyes Tariff Deadline

The NZD/USD had a range of 0.6009 - 0.6063 in the Asia-Pac session, going into the London open trading around 0.6010, -0.83%. The pair has traded under pressure for most of our session as the deadline for tariffs approaches and the risk this presents to global growth. The NZD should find support again around the 0.6000 area as it tries to build a base from which to move higher, a sustained break below here though would risk a deeper correction back to 0.5850/0.5900.

- "RBNZ SHADOW BOARD RECOMMENDS CASH RATE IS HELD THIS WEEK: NZIER" - BBG

- (Bloomberg) - “This week’s antipodean central bank meetings could set the stage for an Australian dollar rally against the kiwi — and spark a selloff in Aussie government bonds.”

- “The Reserve Bank of Australia is widely expected to deliver a second consecutive interest-rate cut, its first back-to-back easing in six years, while the Reserve Bank of New Zealand is likely to hold firm. That policy divergence is sharpening tactical positioning in FX and rates markets.”

- US President Trump has posted via Truth Social that the US will start delivering letters outlining tariff levels to various countries starting 12pm Monday, US eastern time. Trade deals will also be announced at the same time.

- A huge bounce from sub 0.5900 and the NZD has established a foothold above 0.6000, with the USD breaking lower the NZD/USD looked to be building for a potential break higher of its own. A sustained break back below 0.6000 though could negate this and risk a deeper reversion back to the 0.5850/0.5900 area.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6075(NZD519m July 9), 0.6000(NZD407m July10).

- AUD/NZD range for the session has been 1.0811 - 1.0832, currently trading 1.0825. The cross is struggling to get any momentum for now. It looks to be in a 1.0750 - 1.0850 range for now as it awaits a catalyst to provide some clearer direction.

Fig 1: NZD/USD Spot hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Stocks Weaken Ahead of Tariff Deadlines

As the July 9 deadline for trade talks draws near, risk appetite worsened in Asia as major bourses fell. Trump has not helped by claiming that those BRIC countries whose policies are not aligned with the US will face an additional 10% levy, weighing heavy on Asia's currencies today.

- China's major bourses are all down today in a weak start to the week. The Hang Seng is down -0.45%, the CSI 300 down -0.59%, Shanghai Comp down -0.20% and the Shenzhen Comp down -0.15%.

- In Taiwan the TAIEX fell -0.93% today.

- The KOSPI was one of the few gainers, up +0.18% today ahead of this week's decision by the BOK.

- The FTSE Malay KLCI is down -0.83% whilst the Jakarta Composite down by just -0.05%.

- The FTSE Straits Times in Singapore was up +0.30% whilst the PSEi in the Philippines was up +0.07%.

- The NIFTY 50 ended Friday up +0.22% but is down in Monday morning trade by -0.11%.

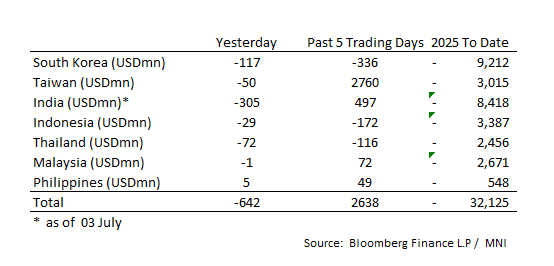

ASIA STOCKS: Strong Regional Outflows to end the Week

Ahead of a Potentially Volatile Period as the tariff deadline approaches, outflows were strong across major bourses.

- South Korea: Recorded outflows of -$117m Friday, bringing the 5-day total to -$336m. 2025 to date flows are -$9,212. The 5-day average is -$67m, the 20-day average is +$18m and the 100-day average of -$82m.

- Taiwan: Had outflows of -$50m Friday, with total inflows of +$2,760 m over the past 5 days. YTD flows are negative at -$3,015. The 5-day average is +$552m, the 20-day average of +$480m and the 100-day average of -$10m.

- India: Had outflows of -$305m as of the 3rd, with total inflows of +$497m over the past 5 days. YTD flows are negative -$8,418m. The 5-day average is +$99m, the 20-day average of +$127m and the 100-day average of $0m.

- Indonesia: Had outflows of -$29 on Friday, with total outflows of -$172m over the prior five days. YTD flows are negative -$3,387m. The 5-day average is -$34m, the 20-day average -$22m and the 100-day average -$32m.

- Thailand: Recorded outflows of -$72m as of Friday, with outflows totaling -$116m over the past 5 days. YTD flows are negative at -$2,456m. The 5-day average is -$23m, the 20-day average of -$15m and the 100-day average of -$21m.

- Malaysia: Recorded outflows as of -$1m on Friday, totaling +$72m over the past 5 days. YTD flows are negative at -$2,671m. The 5-day average is +$14m, the 20-day average of -$9m and the 100-day average of -$19m.

- Philippines: Recorded inflows of +$5m on Friday, with net inflows of +$49m over the past 5 days. YTD flows are negative at -$548m. The 5-day average is +$10m, the 20-day average of -$2m the 100-day average of -$4m.

- Following the decision that the OPEC+ increase in production in August will be greater than expected, oil's fall continued decline continued today.

- WTI declined -1.3% to US$66.24 bbl

- Brent declined -0.75% to US$67.98 bbl.

- OPEC+ had speculated that the rise in August output could be in the region of 400k barrels a day. Instead it announced a 548k increase citing summer demand at a time when global growth is challenged by the US tariffs.

- It has been one of President Trump's key policies (lower gas prices) and his ongoing pressure on OPEC+ appears to be paying off.

- The OPEC+ group has not finalized its output decision for September but speculation remains for a further increase.

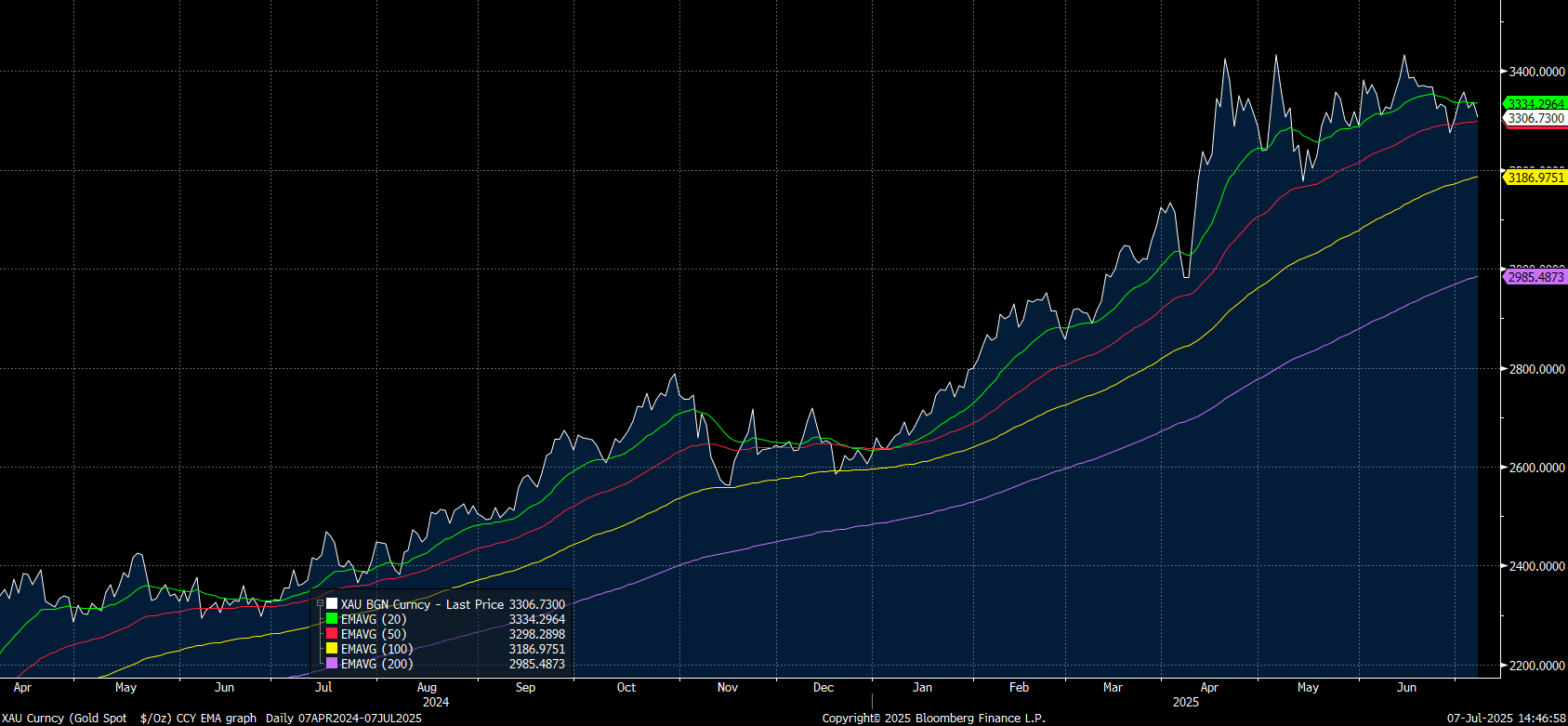

Gold Falls Ahead of Tariff Deadline

- Gold edged lower in the Asia trading day ahead of a week that could be dominated by tariff headlines.

- As the July 9 deadline for US tariffs draws nearer, some of the major equity bourses fell as did gold.

- Gold had opened at US$3,337.16 at this morning's open and by early afternoon was down -0.90% at $3,307.38.

- With the US Treasury Secretary Scott Bessent indicating that there could possibly be extensions due ongoing negations, it seems likely that risk appetite for many asset classes could remain muted this week.

The move lower sees gold edge towards the 50-day EMA of $3,298.28.

source: Bloomberg Finance LP / MNI

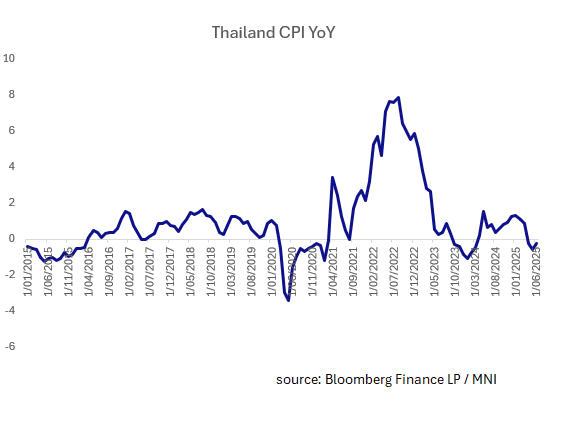

THAILAND: CPI Falls More than Expected

- Thailand's June CPI declined -0.25% YoY, surpassing market estimates of -0.10%.

- This is the third consecutive month of declines in worrying signs for the nation gripped in yet another period of political turmoil.

- The CPI NSA MoM figure barely stayed positive at +0.02%, down from +0.26% in May.

- Core CPI YoY rose +1.06% in June, down modestly from +1.09% in May.

- Meanwhile Thailand has submitted a revised trade proposal to the US in a bid to avert a punitive 36% export levy threatened by the Trump administration before the July 9 deadline, according to Finance Minister.

- Thailand will push ahead with plans to stimulate the economy and pass the budget for next year as planned, despite an ongoing political crisis.

- The government will inject an additional 48 billion baht into the economy over the remaining three months of the current fiscal year, and the $115 billion budget bill is on track to be passed by parliament by the end of August.

BOK: PREVIEW: BOK To Remain on Hold this Week

- The Bank of Korea ("BOK") expects the Korean economy to expand between +1.6% -1.7% for 2025, despite the economy contracting in Q1. This forecast is underpinned by the rate cuts the BOK has undertaken, with the most recent being at the meeting in May.

- Korea has been through a period of serious political upheaval which since the election of a new government in June is hoped to be in the past, with the incoming government expected to implement a further supplementary budget soon.

- A significant risk to the export oriented economy is the threat posed by US tariffs and as we approach the US tariff deadline, the chance that volatility rises grows.

- The market has begun to price out rate cuts with only 2bps of change priced in over the next 3 months.

- Since March the market has gone from pricing in -37bps of cuts over a 12 month time horizon to now less than half of that. Given that the likelihood that the tariff discussions are fully resolved by the time of the BOK meeting, we see limited scope for a further BOK cut and for them to remain at 2.50%.

BNM: PREVIEW: BNM to Hold Rates Steady this Week.

- The Bank Negara Malaysia ("BNM") maintains a cautiously optimistic outlook for the Malaysian economy projecting the economy to grow between +4.5% and +5.5% this year to follow on from +5.1% in 2024. The BNM expects the growth to be underpinned by robust domestic demand, strong investment activity and household expenditure. Inflation has remained subdued and below the BNM's expected range.

- Headline CPI was at +1.5% for Q1, with core at +1.9% against an expected range of +2.0% -3.5%.

- The BNM has been on hold since May 2023 at 3.00% with the only key change in that time being the reduction in the statutory reserve requirement ratio by 100bps in May, which caught markets by surprise. Estimates are that this released approximately MYR19bn of liquidity into the system, a move seen as a strong signal of the BNM's support.

- The risks to the outlook for growth are influenced by the outcome of the talks with the US on tariffs. Exports were robust in May and June's PMI whilst remaining in contraction, showed signs of an improving outlook for sentiment. Until the outcome of the trade talks is concluded, the cut in RRR seems sufficient support for the economy and as such we see the BNM on hold at its meeting on July 09.

CHINA: Country Wrap: IPOs Surge in Hong Kong

- China will replicate 77 pilot measures from the China (Shanghai) Pilot Free Trade Zone (FTZ) in other FTZs and across the country, among efforts to align with high-standard international economic and trade rules and advance high-level institutional opening-up, according to a State Council circular released on Thursday. The measures span seven key areas: services trade, goods trade, digital trade, intellectual property protection, government procurement reform, behind-the-border management systems reform, and risk prevention and control. (source China Daily)

- Chinese Premier Li Qiang said Sunday that BRICS countries should strive to become the vanguard in advancing the reform of global governance. Li made the remarks when addressing the plenary session of "Peace and Security and Reform of Global Governance" of the 17th BRICS Summit, calling on the bloc to safeguard world peace and tranquility, and promote the peaceful settlement of disputes. (source Global Times)

- Applications for initial public offerings (IPOs) in Hong Kong had surged to around 200 so far in 2025 as investors are bullish about the Hong Kong bourse in the second half of this year, Paul Chan, financial secretary of the Hong Kong Special Administrative Region government, wrote on his blog on Sunday. Companies from the Middle East and Southeast Asia were among the applicants for IPOs, said Chan. A total of 42 IPOs in the first six months raised over 107 billion Hong Kong dollars (13.63 billion U.S. dollars), landing Hong Kong the top spot in the world in terms of IPO proceeds. (source XINHUA)

- China's major bourses are all down today in a weak start to the week. The Hang Seng is down -0.45%, the CSI 300 down -0.59%, Shanghai Comp down -0.20% and the Shenzhen Comp down -0.15%.

- Yuan Reference Rate at 7.1506 Per USD; Estimate 7.1656

- The CBG 10yr is unchanged at 1.64% today

INDIA: Country Wrap: Trade Agreement Close

- Union Commerce and Industry Minister Piyush Goyal on Sunday told domestic businesses that India’s free trade agreements (FTAs) will never come at the cost of national interest, as talks with the US for an interim trade deal ahead of the July 9 deadline seemed to stall. Speaking at the FTII Traders Conclave in Srinagar, Goyal said the government is committed to ensuring that all trade deals are reciprocal and protect Indian interests. (source NDTV)

- India and the US are close to a final agreement on trade with officials confirming that agriculture is to be left out. (source Times of India)

- India's foreign exchange reserves rose to $702.78b in the week of June 27 from $697.9b in the week of June 20, according to the Reserve Bank of India. Foreign exchange reserves rose $4.849b from a week earlier (source BBG)

- The NIFTY 50 ended Friday up +0.22% but is down in Monday morning trade by -0.11%.

- The rupee is down consistent with regional trends by -0.3% at 85.67

- Bonds are quiet during the morning session with the IGB10yr at 6.29%

INDONESIA: Country Wrap: Weak IDR Weighs on Budget

- The Indonesian government will need to allocate Rp 552.14 trillion (approximately $34 billion) in the 2025 state budget solely to service interest on its public debt, according to projections released by the Finance Ministry on Sunday. The total consists of Rp 496.98 trillion in domestic interest payments and Rp 55.1 trillion in interest on foreign debt. “For the second half of 2025, interest payment obligations are projected to reach Rp 295.05 trillion -- Rp 261.83 trillion in domestic interest and Rp 33.22 trillion in foreign interest,” the ministry said in its fiscal outlook. A weakened rupiah in the first four months of this year has contributed to rising costs on foreign-denominated debt. However, the currency has shown signs of strengthening over the past two months and is expected to remain relatively stable throughout the second half of 2025. (source Jakarta Globe)

- Australia is hoping that the upcoming review on its trade agreement with Indonesia will make room for critical mineral cooperation, particularly on lithium, according to its diplomat. Indonesia already has a comprehensive economic partnership agreement (CEPA) with Australia, a deal that not only grants zero tariffs for virtually all products, but also provides greater certainty for investors. The Indonesia-Australia CEPA came into effect in 2020. When Australian Prime Minister Anthony Albanese visited Jakarta in mid-May, the two economies agreed to review the CEPA trade pact next year for improvements. (source Jakarta Globe)

- The Jakarta Composite has had a slow start to the week, down just -0.05%.

- The Rupiah is down -0.35% on regional weakness, at 16,241

- Bonds were mixed with the front end rallying whilst the 10YR is lower by -0.05bp at 6.58%.

ASIA FX: USD Higher Amid Fresh Tariff Threats, USD/CNH Testing 20-day EMA

In North East Asia FX, we are seeing uniform losses versus the USD. Market sentiment skittish in the first part of trade, as the US tariff deadline approaches. US President Trump stated that letters detailing tariff levels for some countries (as well as trade deals) would go out 12pm EST US time on Monday. This was followed by Trump comments that any country who aligns with anti-American policies of BRICs countries would face an additional 10% tariff charge.

- USD/CNH has risen around 0.15%, the pair last near 7.1740, which is close to the 20-day EMA resistance point. Earlier lows were at 7.1633, as had another shift down in the USD/CNY fixing. This comes after recent successful negotiations to implement trade talk outcomes that had been agreed to. It remains to be seen what and how this new tariff might be applied by the Trump administration.

- Spot USD/KRW is up around 0.30%, last near 1367/68, which is through the 20-day EMA resistance point. The likes of AUD and NZD have lost around 0.80% against the USD, which has likely driven some negative spill over to the won. The Kospi is holding higher, outperforming the rest of the region. The 50-day EMA is back above 1380 for spot USD/KRW.

- USD/TWD has also risen, the pair up over 0.30%, to be last near 29.00. Recent lows were just under 28.80.

- USD/HKD is holding close to 7.8500. Hibor rates are moving higher but from a low base.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 07/07/2025 | 0600/0800 | ** | Industrial Production | |

| 07/07/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 07/07/2025 | 0900/1100 | ** | Retail Sales | |

| 07/07/2025 | - | ECB Lagarde and Cipollone In Eurogroup Meeting | ||

| 07/07/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 07/07/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 08/07/2025 | 2350/0850 | Balance of Payments | ||

| 08/07/2025 | 0430/1430 | *** | RBA Rate Decision | |

| 08/07/2025 | 0500/1400 | Economy Watchers Survey | ||

| 08/07/2025 | 0600/0800 | ** | Trade Balance | |

| 08/07/2025 | 0645/0845 | * | Foreign Trade | |

| 08/07/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 08/07/2025 | 1000/0600 | ** | NFIB Small Business Optimism Index | |

| 08/07/2025 | - | ECB de Guindos At ECOFIN Meeting | ||

| 08/07/2025 | 1255/0855 | ** | Redbook Retail Sales Index |