EM ASIA CREDIT: MNI EM Credit Overnight – CEEMEA & LATAM

Emerging Markets were softer overnight, with CEEMEA USD benchmark spreads 5–7bp wider. We reviewed the IMF Staff-Level Agreement (SLA) on Côte d’Ivoire and shared fair value estimates for the Kingdom of Bahrain’s dual-tranche USD bonds. In LATAM, USD benchmark spreads widened 5–10bp, while we highlight a new USD mandate from a Brazilian oil & gas company Prio and the Moody’s outlook change on Mexico’s Southern Copper/Minera México.

Cote D'Ivoire: IMF’s SLA, supportive read: https://mni.marketnews.com/4nGkPis

Kingdom of Bahrain: FV for $ L8Y Sukuk & 12Y conv’l deals : https://mni.marketnews.com/4gUsQ0S

Prio: Mandate Investor Meetings: https://www.mnimarkets.com/articles/prio-mandate-investor-meetings-1759348816224

Southern Copper/ Minera Mexico: Moody’s Outlook to Stable: https://mni.marketnews.com/48tKdUf

CEEMEA: https://mni.marketnews.com/46yCNh4

LATAM: https://mni.marketnews.com/4nzOE4q

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GOLD: Precious Metals Rise On Fed Cut Expectations

Gold and silver had another good day on Monday supported by market pricing of a September Fed rate cut approaching 90% after US core PCE prices printed in line with consensus but August consumer sentiment moderated. Friday’s payroll data will be key. Gold rose 0.8% to $3476.07/oz after a high of $3489.85. It is currently around $3480.9. The USD index was little changed.

- Bullion remains in an uptrend with the bull trigger at $3500.1, 22 April record high. Initial firm support is $3371.9, 20-day EMA.

- Silver rose 2.5% to $40.697 after reaching $40.799. It couldn’t hold breaks above initial resistance at $40.798. It is trading around $40.69 today. The metal continues to make higher highs and higher lows confirming the uptrend. Initial support is $38.363, 20-day EMA. Bloomberg reported that in August ETF buying of silver rose for the 7th straight month.

- Silver has also been added to the US list of critical minerals. It is a key component of solar panels.

- European equities were stronger with the Euro stoxx +0.3% and FTSE +0.1%. The S&P e-mini is down 0.1% so far on Tuesday after rising 0.2% on Tuesday. Oil rallied with WTI +0.9% to $64.61/BBL. Copper fell 0.4%.

JGBS: Futures Threatening Fresh Break Lower, 10yr Auction/BoJ Speech In Focus

JGB futures finished Monday trade at 137.24, -.06 versus settlement levels post the Tokyo close. Intra-session lows for Monday were at 137.21. Downside momentum in JGB futures was supported by offshore developments, with generally negative leads from EU and US markets. There may also be some nervousness creeping into markets ahead of today's 10yr debt auction. Recall last week there was quite a poor bid to cover ratio at the 2yr auction.

- In terms of JGB futures technicals, a bear threat remains present and the contract is trading closer to its recent lows. A resumption of weakness would signal scope for an extension towards 136.57, a Fibonacci projection.

- Before the 10yr auction we have August monetary base figures, while BoJ Deputy Governor Himino speaks at 10:30am local time. Focus will for the speech will be any hiking hints ahead of year end. The end Oct meeting has a market implied rate of just above 0.60%, against a current effective policy rate near 0.48%.

- In the cash JGB space, the 10yr yield ended yesterday at 1.635. The 10yr swap rate was last close to 1.445%.

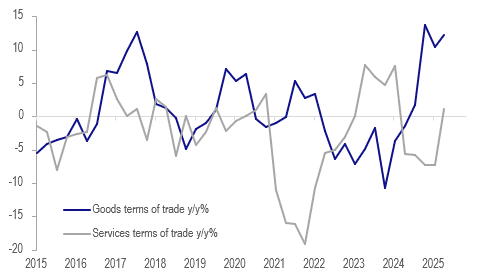

NEW ZEALAND: Goods Terms Of Trade Continues Moving Higher

NZ saw the largest improvement in the merchandise terms of trade in Q2 since Q1 2024. It rose 4.1% q/q, the sixth consecutive quarterly increase, to be up 12.2% y/y after 10.3% y/y in Q1. While domestic demand remains soft, this rise in the terms of trade will be providing some welcome support to growth. The services terms of trade fell 0.4% q/q but rose 1.0% y/y after falling 7.3% y/y.

NZ terms of trade y/y%

- A 3.7% q/q fall in imported goods prices drove the terms of trade rise as export prices rose only 0.25% but they are up 11.7% y/y. Dairy export prices rose 2.0% q/q to be up 19.7% y/y after +10.5% & 26.8% in Q1.

- Services saw a 1.8% q/q fall in export prices and -1.4% for imports leaving them up 5% y/y and 4% y/y respectively.

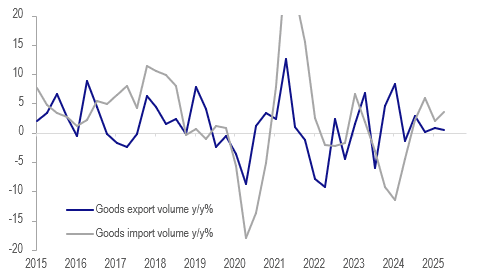

- Goods export volumes fell 3.7% q/q to be up only 0.4% y/y driven by a 7.9% q/q decline in dairy shipments. Import volumes rose 4.2% q/q to be up 3.5% y/y. This signals that Q2 net exports could detract from GDP growth when it is released on September 18.

- Consumption goods import volumes fell 1.3% q/q to be up only 0.5% y/y after -0.1% q/q & +2.3% y/y in Q1. This was the third straight quarterly decline signalling that household spending remains weak.

NZ merchandise trade volumes y/y%

Source: MNI - Market News/LSEG