EM ASIA CREDIT: MNI EM Credit Market Update - Asia

Asia EM USD sovereign and agency spreads are trading wider this morning, with Thailand underperforming (PTTEPT 30s +3bp). Asian equities are also lower, with the Korean KOSPI down 2.7% amid continued trade deal uncertainty and escalating tensions with North Korea. In overnight news, KB Capital priced its USD 5Y deal in line with fair value estimates. Separately, US President Trump announced new tariffs on furniture and pharmaceutical imports. Pharmaceutical companies can avoid tariffs if they are constructing facilities in the US. No new deals announced this morning.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

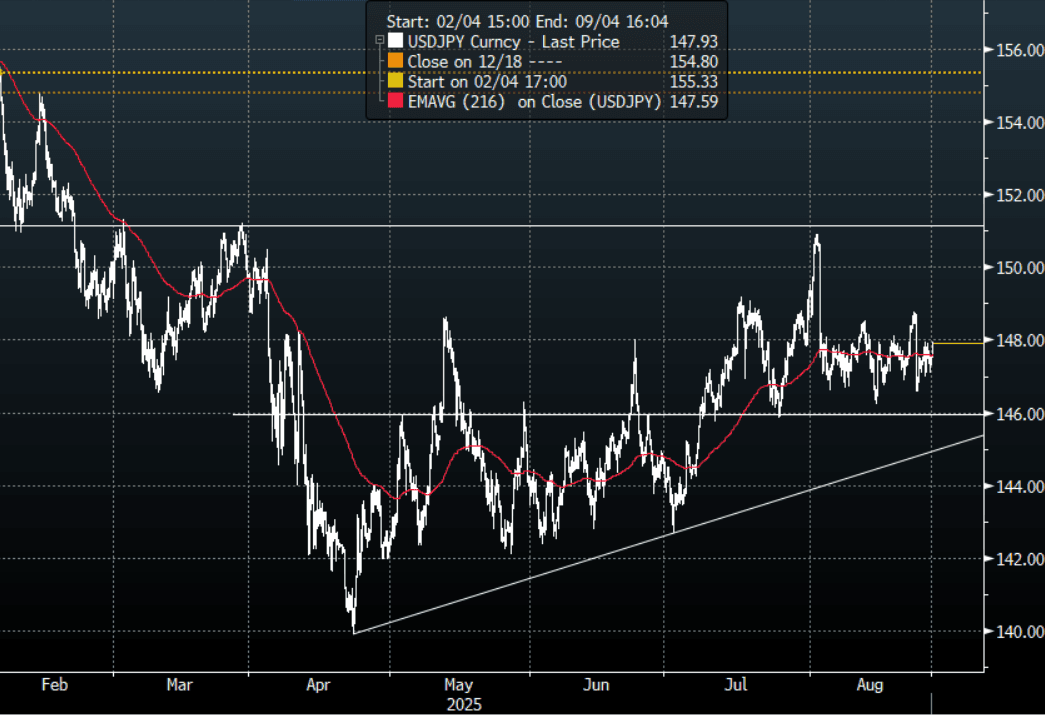

JPY: Asia Wrap - USD Demand Sees USD/JPY Move Back To 148.00

The Asia-Pac USD/JPY range has been 147.30-147.95, Asia is currently trading around 147.90, +0.35%. The demand towards 146.00 has been pretty solid all of July and August, keeping us for the most part in a 146.00-149.00 range. CFTC data for last week shows leveraged accounts again added to JPY shorts so the initial reaction to Powell would have been unwelcome and they would be breathing a little easier as the support continues to hold. We are approaching the corporate month-end so watch for USD demand today and tomorrow. This pair was bid all day today, which does hint at some USD demand flow being executed.

- Kyodo News via BBG - “Long-term interest rates rise to 1.625%, the highest level in 17 years: The yield on the newly issued 10-year government bond (379th issue, nominal interest rate 1.5%), which is an indicator of long-term interest rates, rose to 1.625% at one point, the highest level in about 17 years since October 2008.”

- (Bloomberg) - JGB traders see shorting long-term debt as the gift that keeps giving, with an assist from rising G-10 yields as well as Japan’s Ministry of Finance requesting a bigger budget for its debt financing needs. It’s a vicious cycle for JGBs -- the longer the Bank of Japan stalls in hiking interest rates, the more compensation investors demand for holding super-long bonds as stagflation fears rise.

- “HAYASHI: AKAZAWA VISIT TO THE US NOT DECIDED YET" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 147.25($765m), 147.95($1.04bm), 148.00($997m).Upcoming Close Strikes : 145.00($1.17b Aug 29), 146.50($1.14b Aug 29), 147.50($806m Aug 29) - BBG.

- CFTC data shows last week asset managers have begun to add to their JPY longs after a consistent period of reduction +71379( Last +60866), leveraged funds though again used the dip to add to their newly built short JPY position -50848(Last -41257).

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSTRALIA: Tentative Signs Of Stabilisation In Vacancies

RBA Governor Bullock noted that the vacancies/unemployment ratio was well off its highs and thus signalling that the labour market has eased. The quarterly ratio has been moving sideways for a year and remains above the historical average. However, monthly internet vacancies/unemployed appeared to stabilise in the 3 months to July around the series average. The SEEK new job ads index has moved sideways through most of 2025.

Australia SEEK new job ads index 2013=100

- SEEK reported that July vacancies rose a seasonally adjusted 0.8% m/m but are still down 4.8% y/y. However, the 3-month annualised rate turned positive for the first time since July 2022, consistent with some stabilisation. SEEK notes that the trend posted two consecutive monthly increases for the first time since mid-2022.

- There was strong job ad growth in SA and WA and in the medical and hospitality sectors. SEEK observes that skill shortages persist in mining and renewable energy.

- June applicants-per-ad also appears to have peaked after trending higher since the May 2020 trough. In June the measure fell 4% m/m but is still up 9% y/y with 3-month momentum robust. Labour supply remains elevated.

- The stabilisation in vacancies is consistent with the S&P Global PMI which noted in the preliminary August composite report that there was increased hiring to fill a pickup in new orders. August employment is released on September 18.

AUSSIE BONDS: Weaker But Away From Lows Post July CPI Beat

Aussie bond futures hold weaker, but away from session lows. Weakness has been concentrated in the front end. The 3yr (YM) future was last 96.565, off 3bps, up slightly from session lows of 96.535. The 10yr future (XM) is off less than 1bp at this stage.

- The main data focus was the July CPI print, which came in well above market expectations (headline at 2.8%y/y versus 2.3% forecast and trimmed mean to 2.7%y/y from 2.1% in June).

- The monthly data are incomplete, for instance services aren’t updated in the first month of the quarter, and headline continues to be impacted in both directions by government electricity rebates. As a result, the RBA continues to focus on the quarterly data with Q3 not released until October 29.

- This may have tempered market reaction to a degree.

- In the cash ACGB space, yields are higher across the curve, with the front end leading. We sit away from yield highs though. The 3yr last near 3.42% (highs were close to 3.44%), up 2.5bps, while the 10yr is up close to 1bp, last near 4.32%.

- There has been a slight firmed in RBA dated OIS, around 2bps for contracts out to April next year. Still a full cut is still priced for the Nov 2025 meeting. Only 20% probability of a cut is given for the Sep meeting.

- Tomorrow, we get further inputs into Q2 GDP, with Private capex out. Earlier, Q2 real value of construction work done rose 3% q/q & 4.8% y/y, highest since Q4 2023 and , stronger than expected, after -0.3% q/q & 3.0% y/y.