EM ASIA CREDIT: MNI EM Credit Market Update - Asia

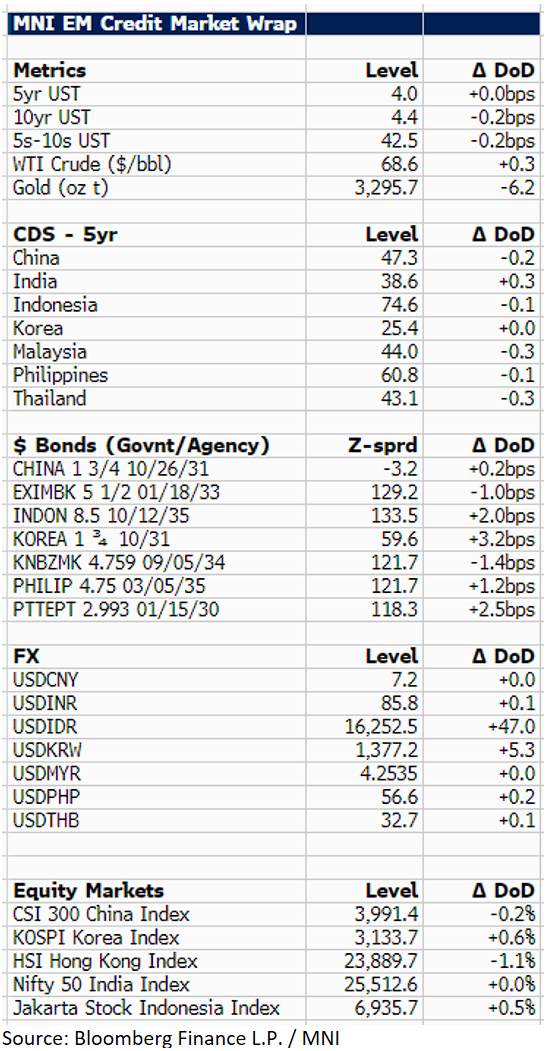

U.S Treasury yields are more or less unchanged at 4.4% with markets focused on U.S. trade talks and proposed copper tariffs.

We followed LATAM where spreads were wider in a 1-8bp range. In Asia, EM also had a softer bias with $ govie/agency spreads 1-3bp wider. The outlier being Korea (+3bp), which reported net June bank lending to households +KRW6.2T (KRW5.2T in May), the largest monthly gain since August last year.

Emerging markets newsflow was dominated by possible U.S. tariffs on copper, which has a limited direct impact on Asia emerging markets. The main producers being Chile, Canada and Mexico. Freeport Indonesia, the largest copper producer in Asia (6th globally), valuations were marginally lower, though not underperforming.

In other news, short-seller Viceroy, released a report calling into question Vedanta's debt sustainability, the VEDLN 12/31s were 1pt lower on the day. There were no new $ fixed issues or mandates.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: Goldman Look For Steeper EUR Curves, Focus On ERZ5/Z7

Goldman Sachs “continue to like Euribor Z5/Z7 steepeners as near-term risks still point towards cuts, whereas the skew of risks further into 2026/27 will be towards better growth and higher inflation vs. current pricing. This deserves an upward sloping money market curve, and this bearish view on the rates expectation curve should limit the declines in core yields other than the very front-end”.

STIR: Just Over 1x25bp ECB Cut Priced Through Year-end; Tariffs Key To Outlook

ECB-dated OIS continue to price just over one full 25bp cut through year-end, with only 3bps of easing priced through the July decision. Following the more hawkish-than-expected stance at President Lagarde’s press conference last Thursday, the bar to another sequential 25bp cut appears high. However, it’s worth remembering that a lot can change between now and July 24, particularly with tariff reprieve deadlines set to expire in this period.

- The MNI Policy Team’s sources piece last Friday noted that tariffs are pivotal for determining [the ECB’s] next moves in 2025, though one more 25-basis-point cut in either September or December is the base-case scenario.

- Euribor futures are flat to +3.0 ticks through the blues, with a flattening bias seen at the front-end. Volumes may be limited by today’s Whit Monday public holiday in some Eurozone states, alongside and the thin data calendar.

- Weekend ECBspeak saw Nagel and Vujcic note that rates were now in neutral territory (a question Lagarde avoided answering at last Thursday’s press conference). Meanwhile, Escriva remains “very comfortable with gradualism, that is, accompanying improvements in inflation with successive 25-basis-point rate cuts”.

- This week's Eurozone calendar is fairly limited, with most interest probably in Wednesday's ECB wage tracker release. The April vintage saw negotiated wages excluding one-off payments falling to 3.024% by Q4 2024.

| Meeting Date | ESTR ECB-Dated OIS (%) | Difference Vs. Current Cut Adjusted Effective ESTR Rate (bp) |

| Jul-25 | 1.893 | -3.0 |

| Sep-25 | 1.770 | -15.3 |

| Oct-25 | 1.738 | -18.5 |

| Dec-25 | 1.666 | -25.7 |

| Feb-26 | 1.653 | -27.0 |

| Mar-26 | 1.644 | -27.9 |

| Apr-26 | 1.649 | -27.4 |

| Jun-26 | 1.662 | -26.1 |

| Source: MNI/Bloomberg Finance L.P. | ||

GILTS: Modest Rally, Labour Market Data & Spending Review Eyed

Gilts rally a little, with core global FI off late Friday/Asia lows and oil off Asia highs.

- Futures comfortably in Friday’s range, topping out at 92.00.

- Yields 1-2bp lower, belly outperforms.

- 2s10s ~62bp, recent breaks below 60bp haven’t been sustained.

- 5s30s ~119bp, after forcing the first sub-120bp closes since early April last week.

- GBP STIRs still trade around levels flagged pre-gilt open, showing ~40bp of cuts through December.

- UK labour market data is due tomorrow, expect our full preview of that release later today. A reminder that the BoE has placed more weight on labour market inferences from surveys, given the long running issues with the ONS readings.

- Elsewhere, Chancellor Reeves will outline the government’s spending review on Wednesday.

- Unlike a Budget or Spring Statement, the review will not contain new forecasts from the OBR, nor will it announce new tax and spending measures.

- Instead, Reeves will detail the spending allocations for individual government departments over the next several years.

- The review is fraught with political risks for Reeves and PM Starmer, with ministers jockeying for the most beneficial outcome for their department.

- The Chancellor has already warned that due to the limited fiscal headroom, not every department will “get everything they want”, risking divisions in Cabinet and ire on the backbenches if Labour MPs do not see sufficient funds going towards areas of concern for them.