MNI ASIA OPEN: US/China Trade Talks Ongoing; CPI Focus

EXECUTIVE SUMMARY

- MNI US INFLATION: MNI US CPI Preview: An Important Pre-FOMC Steer

- MNI FED: Bessent Emerging As Contender for Powell Successor

- MNI US DATA: Small Businesses Increasingly Planning To Raise Prices

- MNI US DATA: Softer Redbook Retail Sales Notes Price-Conscious Shoppers Amid Tariffs

US

MNI FED: Bessent Emerging As Contender for Powell Successor - Bloomberg

Bloomberg reports that Treasury Secretary Bessent is emerging as a possible contender to succeed Fed Chair Powell when his term expires in May 2026. It followed President Trump on Friday saying he would name a successor for Powell “very soon” (see here).

- Former Fed Governor Warsh, long since seen as a front runner, was interviewed by Trump for the Tsy Sec role in November according to people familiar with the matter. Asked specifically about Warsh on Friday, Trump said: “He’s very highly thought of.” The report notes that formal interviews for the Fed Chair position have not begun according to two of the people. “I have the best job in Washington,” Bessent said in response to a request for comment. “The president will decide who’s best for the economy and the American people.”

NEWS

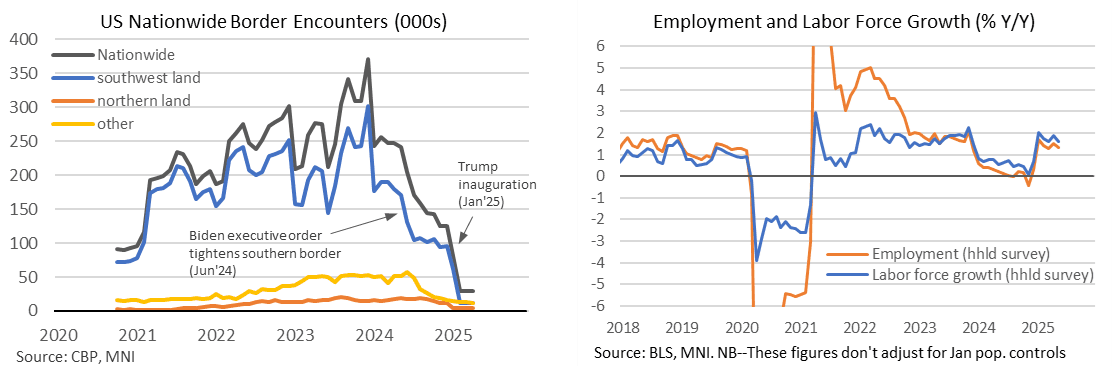

MNI US LABOR MARKET: US Planning To Send 9,000 Migrants To Guantanamo Bay

Politico reports that the US is planning to send 9,000 migrants to Guantanamo Bay, starting next week. "That would be an exponential increase from the roughly 500 migrants who have been held for short periods at the base since February and a major step toward realizing a plan President Donald Trump announced in January to use the facility to hold as many as 30,000 migrants."

- It’s another reminder of the significant changes in labor force dynamics over the past year. Immigration inflows, at least judging by border encounters, had started to fall in Jun 2024 after a Biden executive order tightened the southern border but they have since tumbled under the second Trump administration.

- April saw nationwide encounters of 29k, a -88% Y/Y reduction. For context, they averaged a monthly 144k in 2H24, 240k in 1H24 and 277k in 2023 as a whole.

- Deportations are going a step further and reducing the labor force. It increasingly puts long-term breakeven estimates of payrolls in the ~100k region into focus, in terms of how to compare the relative strength of last week’s May payrolls report as well as upcoming ones.

MNI US-CHINA: Lutnick-'Expect Talks To Go On All Day Today'

With the second day of talks in London between senior US and Chinese trade delegations starting at 10:43BST, US Commerce Secretary Howard Lutnick says on entering Lancaster House that talks are "going well" and that he expects them "to go all day today". Talks are not centered on US 'reciprocal' or other tariffs, but instead at working to mitigate Chinese export controls on rare earths and other critical minerals that are seen to threaten US supply chains.

US TSYS

MNI US TSYS: Narrow Ranges Ahead Midweek CPI Inflation Data

- Treasuries look to finish mixed, off midmorning highs on narrow ranges and light volume (TYU5 under 870k). Market focus on Wednesday morning's key CPI inflation data at 0830ET.

- Analyst unrounded estimates see core CPI inflation accelerating mildly to 0.27% M/M (median, 0.28% average) in May after 0.24% M/M in April. We’ve seen an unrounded range of 0.23-0.34% M/M, with some sizeable discrepancies in used cars and lodging away from home as well as a CPI-specific airfares.

- Officials are still working out technical details as US/China trade talks are expected to reconvene in London at 0800 PM (local time). "LUTNICK: CHINA TALKS WENT REALLY REALLY WELL .. TALKS COULD GO INTO TOMORROW IF NEED BE" Bbg.

- No new developments from California as US Marines deployed to quell any deportation unrest.

- Stocks gaining slightly after the bell after some late program selling tempered support with focus on Wednesday morning's CPI inflation data.

- Cross asset roundup: Bbg US$ index scaling back support late (BBDXY +.99 at 1210.39); crude weaker (WTI -.59 at 64.70), Gold making modest gains: +5.22 at 3331.40.

OVERNIGHT DATA

MNI US INFLATION: MNI US CPI Preview: An Important Pre-FOMC Steer

Analyst unrounded estimates see core CPI inflation accelerating mildly to 0.27% M/M (median, 0.28% average) in May after 0.24% M/M in April. We’ve seen an unrounded range of 0.23-0.34% M/M, with some sizeable discrepancies in used cars and lodging away from home as well as a CPI-specific airfares. The broad assumption is that May could have started to see a greater tariff impact than April but that firmer increases are more likely to show in summer months.

MNI US DATA: Small Businesses Increasingly Planning To Raise Prices

Price components in today’s NFIB small business survey reinforce a view that May CPI – released tomorrow – might not see stronger tariff-driven inflation until the summer months. Whilst actual price changes held steady back close to their 2024 average, the breadth of planned price increases tilted higher again for the highest in just over a year even if it's still markedly lower than the surge in 2021/22.

- The NFIB small business survey was stronger than expected in May at 98.8 (cons 96.0) after 95.8 in April, at what had been its lowest since Oct 2024. Whilst off a high of 105.1 in December ahead of Trump’s inauguration in January, it’s still elevated compared to levels through most of 2022-24 when it averaged closer to 90.

MNI US DATA: Softer Redbook Retail Sales Notes Price-Conscious Shoppers Amid Tariffs

Johnson Redbook retail sales showed some signs in slowing the first week of June, rising 4.7% Y/Y (week ending Jun 7), vs a targeted gain of 5.7%. A continued rise at the current pace would mark the softest month since January, and a continued deceleration from 6.7% in April (was 5.5% in May).

- May's Census Bureau retail sales (out next Tuesday) is seen printing 0.0% M/M after 0.1% in April. Roughly speaking that would translate into 4.8% Y/Y growth, after 5.2% in the prior two months, so also reflecting an early summer slowdown. All of these series are in nominal terms.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA up 61.94 points (0.14%) at 42824.02

S&P E-Mini Future up 25.75 points (0.43%) at 6036.5

Nasdaq up 103.1 points (0.5%) at 19694.15

US 10-Yr yield is down 0.8 bps at 4.4659%

US Sep 10-Yr futures are up 2/32 at 110-7

EURUSD up 0.0006 (0.05%) at 1.1428

USDJPY up 0.32 (0.22%) at 144.89

WTI Crude Oil (front-month) down $0.57 (-0.87%) at $64.70

Gold is up $7.89 (0.24%) at $3333.99

European bourses closing levels:

EuroStoxx 50 down 6.14 points (-0.11%) at 5415.38

FTSE 100 up 20.8 points (0.24%) at 8853.08

German DAX down 186.76 points (-0.77%) at 23987.56

French CAC 40 up 12.86 points (0.17%) at 7804.33

US TREASURY FUTURES CLOSE

3M10Y +0.452, 12.249 (L: 7.415 / H: 13.122)

2Y10Y -1.22, 45.612 (L: 44.92 / H: 47.202)

2Y30Y -1.353, 92.076 (L: 91.596 / H: 94.242)

5Y30Y -0.75, 84.839 (L: 84.537 / H: 86.906)

Current futures levels:

Sep 2-Yr futures down 0.625/32 at 103-16.125 (L: 103-15.625 / H: 103-18)

Sep 5-Yr futures up 0.5/32 at 107-23 (L: 107-20.25 / H: 107-27.25)

Sep 10-Yr futures up 2.5/32 at 110-7.5 (L: 110-02 / H: 110-14)

Sep 30-Yr futures up 10/32 at 112-21 (L: 112-10 / H: 113-02)

Sep Ultra futures up 13/32 at 115-31 (L: 115-18 / H: 116-17)

MNI US 10YR FUTURE TECHS: (U5) Bearish Threat Remains Present

- RES 4: 111-30 76.4% retracement of the May 1 - 22 downleg

- RES 3: 111-19+ 1.0% 10-dma envelope

- RES 2: 111-14+ High Jun 5 & 61.8% of the May 1 - 22 downleg

- RES 1: 110-20 50-day EMA

- PRICE: 110-07+ @ 11:13 BST Jun 10

- SUP 1: 109-26 Low May 29

- SUP 2: 109-12+ Low May 22 and the bear trigger

- SUP 3: 109-09+ Low Apr 11 and key support

- SUP 4: 108-25+ 0.764 proj of the Apr 7 - 11 - May 1 price swing

The recent reversal lower in Treasury futures, undermines the current bullish theme. An extension down would expose support at 109-26, the May 29 low, where a break would open key support and the bear trigger, at 109-12+, the May 22 low. Key short-term resistance has been defined at 111-14+, a Fibonacci retracement and the Jun 5 high. Clearance of this hurdle would be bullish.

SOFR FUTURES CLOSE

Jun 25 +0.003 at 95.680

Sep 25 -0.005 at 95.855

Dec 25 -0.010 at 96.095

Mar 26 -0.015 at 96.30

Red Pack (Jun 26-Mar 27) -0.015 to -0.005

Green Pack (Jun 27-Mar 28) steadysteady0 to +0.010

Blue Pack (Jun 28-Mar 29) +0.010 to +0.015

Gold Pack (Jun 29-Mar 30) +0.020 to +0.020

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.29% (+0.00), volume: $2.643T

- Broad General Collateral Rate (BGCR): 4.27% (+0.00), volume: $1.071T

- Tri-Party General Collateral Rate (TCR): 4.27% (+0.00), volume: $1.038T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $114B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $289B

FED Reverse Repo Operation

RRP usage inches up to $182.725B this afternoon from $179.315B yesterday, total number of counterparties at 31. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

MNI PIPELINE: Corporate Bond Update: $9.85B to Price Tuesday

- Date $MM Issuer (Priced *, Launch #)

- 06/10 $3B #Lloyds $1.25B 4NC3 +83, $500M 4NC3 SOFR+106, $1.25B 11NC10 +160

- 06/10 $2.75B #ANZ $500M 3Y +38, $1B 3Y SOFR+62, $1.25B 11NC10 +135

- 06/10 $1.5B #M&T $750M 3NC2 +75, $750M 6NC5 +110

- 06/10 $600 #Omega Healthcare 5Y +132

- 06/10 $500M #Lineage OP 5Y +140

- 06/10 $500M #PVH Corp WNG 5Y +145

- 06/10 $500M #CAF WNG Perp5.5 6.75%

- 06/10 $500M *Experian Finance 10Y +90

MNI BONDS: EGBs-GILTS CASH CLOSE: Rally Extends On Softening UK Jobs Data

European yields fell for the second day this week Tuesday, with Gilts outperforming Bunds.

- Gains were basically steady throughout the session, as some of last week's ECB-related selloff continued to reverse.

- Data out early in the session confirmed that the UK labour market is softening at an increasing pace, with AWE wage data on track to come in even lower in Q2 than the BOE’s Q1 forecast miss, and HMRC payrolls data pointing to growing slack. Our analysis of the release is here (PDF).

- The data saw BOE cut pricing rise to nearly 50bp for the year, up from 41bp prior.

- The UK curve leaned bull steeper, with the belly outperforming. Germany's bull flattened.

- Periphery / semi-core EGB spreads were mixed, with BTPs once again outperforming and 10Y now targeting the 90bp level vs Bunds.

- Wednesday is light for European data, with the main highlight expected to be the ECB Wage tracker. Most attention will be on US CPI. We also hear from ECB's Lane, Makhlouf, and Cipollone.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1.7bps at 1.847%, 5-Yr is down 3.3bps at 2.123%, 10-Yr is down 4.4bps at 2.523%, and 30-Yr is down 4.2bps at 2.97%.

- UK: The 2-Yr yield is down 8.4bps at 3.919%, 5-Yr is down 9bps at 4.048%, 10-Yr is down 9bps at 4.542%, and 30-Yr is down 7.4bps at 5.254%.

- Italian BTP spread down 0.7bps at 91.3bps / French OAT unchanged at 67.2bps

MNI FOREX: GBP Remains Moderately Lower Post Soft UK Labour Market Data

- Currency markets have traded in a more subdued fashion Tuesday, as market participants continue to await any details on developments regarding US/China trade talks, which remain ongoing in London as the European session comes to an end. As of 1730BST, the dollar index is just 0.1% green, giving back a small portion of yesterday’s decline.

- GBP if off its worst levels, but remains a standout underperformer following the softer set of UK labour market data releases. Weakness in GBP came in two phases in early trade, first on the weak payrolls data, and then again on the SONIA open, with GBPUSD briefly piercing 1.3462, its 20-day EMA. A clear break of this average would suggest potential for a deeper correction and expose the 50-day EMA for direction, at 1.3299. Cable has since recovered back above 1.35 as we approach the APAC crossover.

- EURGBP stands 0.35% higher on the day, and in the process has breached a key short-term resistance at 0.8440, the 50-day EMA. A clear break of the average is required to highlight a stronger reversal, potentially exposing 0.8541, the May 02 high.

- Dips below the 0.8400 handle have been well supported in recent months, and key support has been defined at 0.8356, the May 29 low. Clearance of this level would be required to resume the technical downtrend.

- USDJPY had some early volatility on Tuesday, as initial Ueda comments prompted the pair to trade up to 145.29 and eclipse the post-payrolls high. Spot then subsequently moved lower following some temporary weakness for equities but found solid support between 144.40/50.

- Aside from potential headlines on US/China developments, all attention now turns to the US May inflation data due Wednesday, an important pre-FOMC steer.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 11/06/2025 | 0630/0730 | BOE Saporta Speech At Bank of Finland and SUERF Conference | ||

| 11/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 11/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 11/06/2025 | 0930/1130 | ECB Lane At 2025 Government Borrowers Forum | ||

| 11/06/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 11/06/2025 | 1130/1230 | Chancellor Reeves presents Spending Review to Parliament | ||

| 11/06/2025 | - | *** | Money Supply | |

| 11/06/2025 | - | *** | New Loans | |

| 11/06/2025 | - | *** | Social Financing | |

| 11/06/2025 | 1200/1400 | ECB Cipollone On Digital Payments Panel | ||

| 11/06/2025 | 1230/0830 | * | Building Permits | |

| 11/06/2025 | 1230/0830 | *** | CPI | |

| 11/06/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 11/06/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 11/06/2025 | 1800/1400 | ** | Treasury Budget |