MNI ASIA OPEN: Tsys Hold Range Ahead June FOMC Minutes

EXECUTIVE SUMMARY

- MNI FED: FOMC Minutes: Analysts Eye Discussion Of July Cut, Tariff Inflation

- MNI US TSYS/SUPPLY: Treasury Starts Ramping Up Bill Issuance To Rebuild Cash Pile

- MNI US DATA: NY Fed Survey Adds Further Evidence Of Anchored Inflation Expectations

US

MNI FED: FOMC Minutes: Analysts Eye Discussion Of July Cut, Tariff Inflation

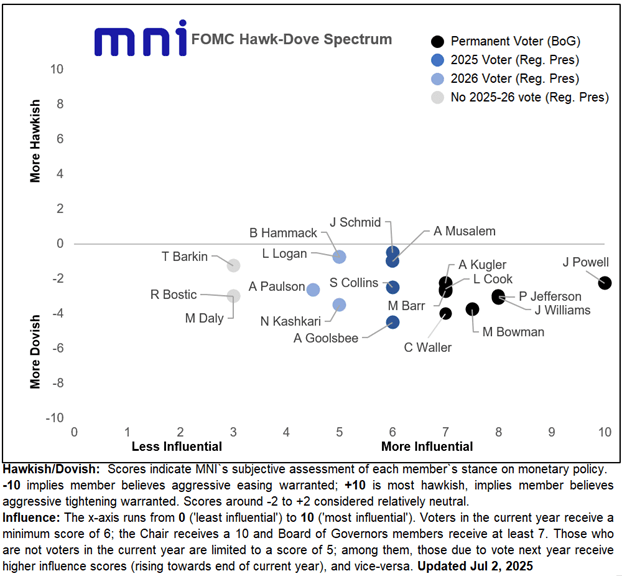

We've just published our preview to the June FOMC meeting, including what to watch for upon release; MNI's FOMC Hawk-Dove Spectrum; analyst previews; and key highlights of FOMC participant commentary since the June meeting. Download Full Report Here

- The minutes of the June 17-18 FOMC meeting (released Wednesday Jul 9 at 2pm ET) should underline the Committee's patience in making its next rate move amid heightened tariff-related economic uncertainty, as encapsulated in the meeting's Dot Plot which showed participants largely divided between no cuts and 2 cuts by year-end.

NEWS

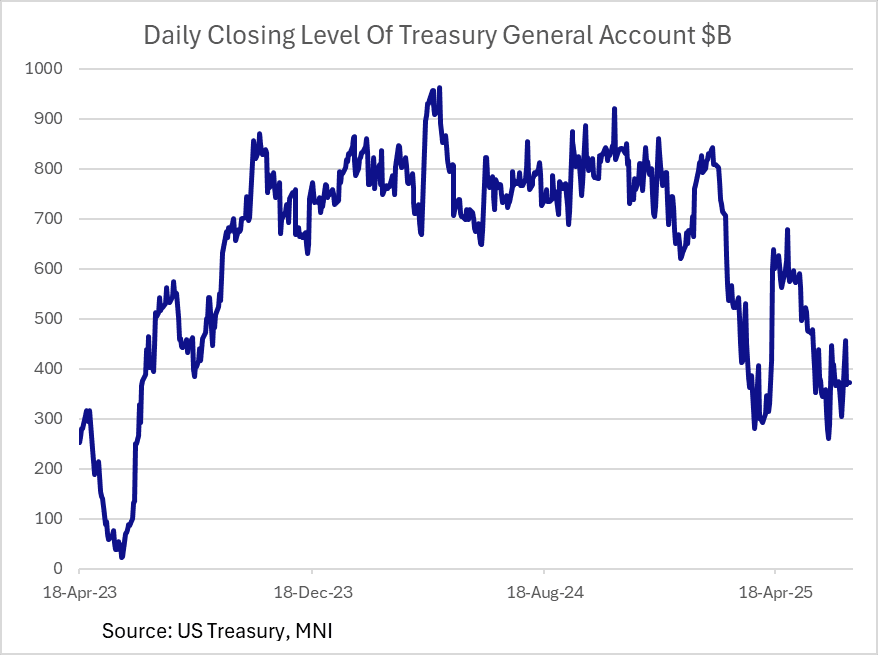

MNI US TSYS/SUPPLY: Treasury Starts Ramping Up Bill Issuance To Rebuild Cash Pile

Treasury has made its first indication of its cash management plans since last week's $5T increase in the debt limit paved the way for a rebuild in the Treasury General Account: "Treasury plans to increase issuance of Treasury bills to continue financing the government and to gradually rebuild the cash balance over time to a level more consistent with Treasury's cash balance policy."

MNI US: President Trump Latest Comments/Headlines on Trade Deals

- President Trump states that August 01 is not a change of deadline, it’s a clarification and that the incentive remains for countries to deal in the US. Trump believes the administration is picking out low and fair tariff numbers, with most rates lower than what the US is being charged. Trump reiterates his prior threats on a 10% tariff for nations in BRICS, saying that anybody in BRICS will be getting that charge pretty soon.

- Moving onto the dollar, Trump states that if people want to challenge dollar, they'll pay price.

- On negotiations with the EU, Trump says the EU was much worse than China in dealing with, but that Von Der Leyen has been very nice recently and that a letter to the EU is probably two days away.

- Regarding some other letters, Trump says “we have some 60, 70%. Those are ones with massive you know, where we have massive trade deficits because they've treated us very badly. But I would say in every case, I'm treating them better than they treated us over the years.

- Trump says that the administration could have been much harsher on trade, and that they have the ability to go higher with tariffs.

US TSYS

MNI US TSYS: Tsys Hold Narrow Range Ahead June FOMC Minutes, Tariff Talk

- Treasuries look to finish moderately weaker, off low end of a narrow session range. Second consecutive day of limited economic data (NY Fed 1Y inflation exp lower than exp) with focus on Wednesday afternoon's June FOMC minutes release at 1400ET.

- The June minutes should underline the Committee's patience in making its next rate move amid heightened tariff-related economic uncertainty, as encapsulated in the meeting's Dot Plot which showed participants largely divided between no cuts and 2 cuts by year-end.

- Markets also on edge as Pres Trump discussed tariffs at latest cabinet meeting: the administration could have been much harsher on trade, and could "go higher". Trump announced a 50% tariff on cooper and will announce more on "pharma, chips, other things.." after threatening a 200% duty on pharmaceuticals.

- Commerce Secretary Lutnick said on CNBC he "expects 15-20 trade letters to go out over the next two days" while studies on pharmaceuticals and semiconductors will be done by the end of the month.

- Currently, the Sep'25 10Y trades -4 at 110-25.5 (110-21.5L / 111-01.5H), above initial technical support at 110-17 61.8% of the May 22 - Jul 1 bull leg. Curves mixed: 2s10s +2.333 at 50.608; 5s30s -0.094 at 95.467.

- USD off highs, Bbg index BBDXY +0.32 at 1196.83 vs. 1199.72 high; Gold weaker (-31.5 at 3305.0), stocks inching lower late: SPX eminis -5.5 at 6270.75.

OVERNIGHT DATA

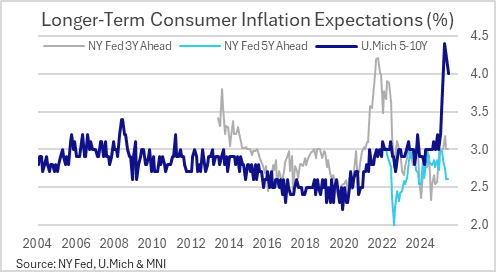

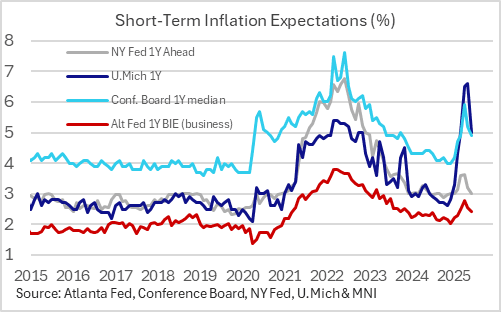

MNI US DATA: NY Fed Survey Adds Further Evidence Of Anchored Inflation Expectations

Overall inflation expectations receded in June for the 2nd consecutive month in the New York Fed's Survey of Consumer Expectations, following April's apparent peak amid tariff announcements. It adds to evidence that inflation expectations are "well anchored", or at least, certainly not becoming de-anchored even as tariffs are expected to start feeding into goods price inflation over the coming months.

- 1Y ahead median expected inflation fell to a 5-month low 3.02% (3.20% prior), well down from the 3.63% peak in April. 3Y expectations were steady at 3.00%, and has now been at a rounded 3.0% for 6 of 7 months with the exception being 3.2% in April. And longer-term expectations were also steady, with the 5Y median remaining at 2.61%, a joint 16-month low.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA down 172.11 points (-0.39%) at 44231.33

S&P E-Mini Future down 5 points (-0.08%) at 6271.25

Nasdaq up 1.5 points (0%) at 20417.76

US 10-Yr yield is up 3.2 bps at 4.4112%

US Sep 10-Yr futures are down 4.5/32 at 110-25

EURUSD up 0.0014 (0.12%) at 1.1723

USDJPY up 0.58 (0.4%) at 146.63

WTI Crude Oil (front-month) up $0.54 (0.79%) at $68.46

Gold is down $32.19 (-0.96%) at $3304.79

European bourses closing levels:

EuroStoxx 50 up 30.41 points (0.57%) at 5371.95

FTSE 100 up 47.65 points (0.54%) at 8854.18

German DAX up 133.24 points (0.55%) at 24206.91

French CAC 40 up 43.24 points (0.56%) at 7766.71

US TREASURY FUTURES CLOSE

3M10Y +2.607, 5.223 (L: -6.699 / H: 7.99)

2Y10Y +2.333, 50.608 (L: 48.455 / H: 51.974)

2Y30Y +1.205, 103.061 (L: 101.865 / H: 106.154)

5Y30Y -0.475, 95.086 (L: 95.086 / H: 98.53)

Current futures levels:

Sep 2-Yr futures down 0.125/32 at 103-20.75 (L: 103-19.75 / H: 103-21.875)

Sep 5-Yr futures down 2.25/32 at 108-4.75 (L: 108-02.75 / H: 108-09.25)

Sep 10-Yr futures down 4/32 at 110-25.5 (L: 110-21.5 / H: 111-01.5)

Sep 30-Yr futures down 4/32 at 113-3 (L: 112-21 / H: 113-17)

Sep Ultra futures down 2/32 at 116-6 (L: 115-15 / H: 116-22)

MNI US 10YR FUTURE TECHS: (U5) Breaches The 50-Day EMA

- RES 4: 113-07 76.4% retracement of the Apr 7 - 11 bear leg

- RES 3: 112-23 High May 1 and key resistance

- RES 2: 112-12+/15 High Jul 1 / 61.8% of the Apr 7 - 11 sell-off

- RES 1: 111-07+/111-28 20-day EMA / High Jul 3

- PRICE: 110-23.5 @ 1415 ET Jul 08

- SUP 1: 110-17 61.8% of the May 22 - Jul 1 bull leg

- SUP 2: 110-10+ Low Jun 16

- SUP 3: 110-03 76.4% of the May 22 - Jul 1 bull leg

- SUP 4: 109-28 Low Jun 6 and 11

Treasury futures maintain a softer short-term tone as the contract extends the pullback that started Jul 1. Price has traded through support at the 50-day EMA, at 110-31. This undermines a recent bull theme and paves the way for an extension lower near-term. Sights are on 110-17 next, a Fibonacci retracement point. A break would strengthen a bearish threat. Resistance to watch is at 111-28, the Jul 3 high.

SOFR FUTURES CLOSE

Sep 25 -0.010 at 95.855

Dec 25 -0.020 at 96.135

Mar 26 -0.025 at 96.380

Jun 26 -0.025 at 96.60

Red Pack (Sep 26-Jun 27) -0.025 to -0.02

Green Pack (Sep 27-Jun 28) -0.025 to -0.02

Blue Pack (Sep 28-Jun 29) -0.02 to -0.015

Gold Pack (Sep 29-Jun 30) -0.015 to -0.01

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.33% (-0.02), volume: $2.814T

- Broad General Collateral Rate (BGCR): 4.31% (-0.01), volume: $1.136T

- Tri-Party General Collateral Rate (TCR): 4.31% (-0.01), volume: $1.106T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $118B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $263B

FED Reverse Repo Operation

RRP usage inches up to $219.415B this afternoon from $218.030B yesterday, total number of counterparties at 37. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021 - compares to yesterday's (July 1) $460.731B highest usage since December 31.

MNI PIPELINE: Corporate Bond Update: $2.25B American Honda 3Pt Launched

- Date $MM Issuer (Priced *, Launch #)

- 07/08 $3B *IADB (Inter-American Development Bank) 10Y SOFR+61

- 07/08 $2.25B #American Honda $900M 2Y +65, $600M 2Y SOFR+87, $750M 7Y +100

- 07/08 $1.25B #BFCM $650M 3.25Y +72, $600M 3.25Y SOFR+99

- 07/08 $750M Gray Media 7NC investor calls

- Potential roll-over from Monday:

- 07/?? $Benchmark Nissan Motor 5Y 7.25%a, 7Y 7.75%a, 10Y 8%a

- 07/?? $Benchmark NTT Finance Corp multi tranche investor calls: 2Y, 3Y fix/SOFR, 5Y fix/SOFR, 7Y, 10Y, 12Y -- in addition to EUR issuance 2Y, -4Y, 8Y and 12Y

MNI BONDS: EGBs-GILTS CASH CLOSE: Further Bear Steepening

European yields rose Tuesday, with continued curve steepening.

- Core FI was under pressure from the open, following on from Monday's weak close. There were multiple cause driving weakness, including supply (Netherlands, Austria, EU) along with a 3-week extension of the US's tariff negotiation deadline to Aug 1.

- While there was little immediate market reaction, the release of the UK OBR's Fiscal Risks and Sustainability Report reminded of longer-term fiscal concerns.

- Yields rose steadily all morning before before steadying in afternoon trade. 10Y Gilt yields pushed through the July 2 highs to hit the highest levels in a month.

- 10Y Bund yields hit a fresh 3-month intraday high of 2.707% but ultimately held on to the 2.70% area (mid-May highs).

- The UK and German curves both bear steepened, though short-end Gilts outperformed.

- Periphery/semi-core EGB spreads were mixed, with Greece outperforming.

- Wednesday's calendar includes appearances by ECB's Lane, Guindos and Nagel and the release of the BOE's FSR, though it's a lighter day for data including Greek June inflation. There will also be focus on EU-US trade negotiations, with President Trump saying after the European cash close that a tariff "letter" to Brussels is probably two days away.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 3.5bps at 1.872%, 10-Yr is up 4.4bps at 2.687%, and 30-Yr is up 5.4bps at 3.172%.

- UK: The 2-Yr yield is up 0.8bps at 3.872%, 5-Yr is up 3.1bps at 4.042%, 10-Yr is up 4.7bps at 4.633%, and 30-Yr is up 6.3bps at 5.454%.

- Italian BTP spread up 0.2bps at 85bps /Greek down 0.6bps at 68.8bps

MNI FOREX: AUD Remains Higher Post RBA, JPY Weakness Extends

- The greenback is consolidating another positive session on Tuesday, with the USD index extending its latest recovery and rising ~0.3%. Renewed tariff related uncertainty appears to be underpinning the renewed optimism, with the latest rhetoric from President Trump doing little to change the tone.

- In similar vein to Monday’s session, the Japanese yen is one of the poorest performing currencies in G10 amid the specific uncertainty related to a US trade deal with Japan and the Japanese PM stating that comprehensive negotiations will continue in the weeks ahead. USDJPY has also benefitted from the higher core yields backdrop, and rose as high as 146.98, further narrowing the gap to the June 23 spike high of 148.03.

- At the other end of the spectrum, the Australian dollar continues to outperform in G10 following the surprise RBA rate hold, against firm market expectations for a 25bp cut. The pair has settled around the 0.6520 mark and a bullish trend set-up is maintained, with the latest pullback considered technically corrective.

- Standing out on the chart is AUDJPY (+1.10%), which has risen above an important area of resistance around 95.75 which aligns with the March and May highs from earlier in the year. Further upside would target a move towards the February highs at 97.33. Notably, CHFJPY is now trading above 184.00, fresh record highs for the cross. This extends the rally from the June lows to 5.8%.

- China’s CPI/PPI data will precede Wednesday’s calendar highlight of the RBNZ decision, where a majority of analysts expect a rate hold at 3.25%. Later on Wednesday, FOMC minutes are scheduled.

MNI OPTIONS: Expiries for Jul09 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600(E536mln), $1.1675-90(E742mln), $1.1700(E1.7bln)

- USD/JPY: Y144.00-10($1.4bln), Y144.50($860mln)

- EUR/GBP: Gbp0.8655-65(E633mln)

- AUD/USD: $0.6425(A$700mln), $0.6550(A$557mln)

- NZD/USD: $0.6075(N$519mln)

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 09/07/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 09/07/2025 | 0930/1030 | BOE Financial Stability Report | ||

| 09/07/2025 | 1000/1100 | BOE FSR Press Conference | ||

| 09/07/2025 | 1045/1245 | ECB Lane At House of the Euro | ||

| 09/07/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 09/07/2025 | 1100/1300 | EC De Guindos Closing Remarks At Conference | ||

| 09/07/2025 | 1400/1000 | ** | Wholesale Trade | |

| 09/07/2025 | 1400/1000 | ** | Wholesale Trade | |

| 09/07/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 09/07/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 09/07/2025 | 1800/1400 | *** | FOMC Minutes |