MNI ASIA MARKETS ANALYSIS:May Jobs Gain, Stocks at March Highs

HIGHLIGHTS

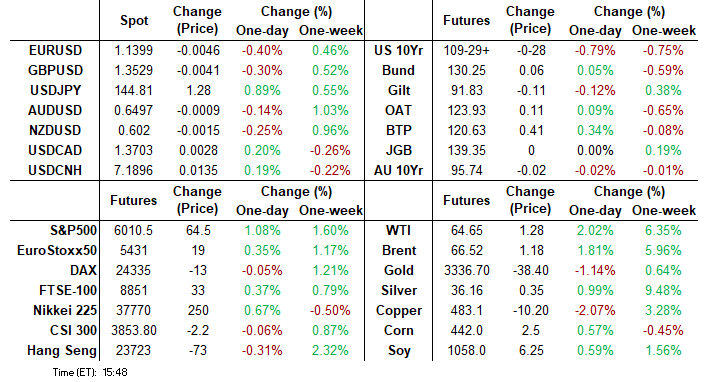

- Treasury yields climbed to just over one week highs Friday (10Y 4.5116% +.1210), initial support after better than expected Jobs gains for May.

- Stocks climbed to the best levels since early-mid March data, while Pres Trump touting a meeting with US & China trade officials in London next week underscored support for risk in late trade.

- Greenback strengthened, prompting the USD index to rise 0.5% and look set to close back above the 99.00 mark.

US TSYS

MNI US TSYS: Year End Rate Cuts Cool After Better Than Expected May Jobs Gain

- Treasuries continued to extend lower after this morning's jobs report shows modestly higher than estimated job gain for May, the unemployment rate and Labor Force Participation Rate at/near expectations.

- A sizeable beat for AHE growth (0.4% M/M vs 0.3% expected), considering the average work week was as expected at 34.3. It of course follows yesterday's surprisingly strong ULC increase for Q1 at 6.6% annualized.

- Tsy Sep'25 10Y futures currently trades -28 at 109-29.5, near technical support at 109-26, the May 29 low, where a break would open key support and the bear trigger, at 109-12+, the May 22 low.

- Curves mixed: 2s10s +0.473 at 47.104, 5s30s -4.442 at 84.023. projected rate cut pricing continued to consolidate vs. morning levels (*) as follows: Jun'25 at 0.0bp (-0.6bp), Jul'25 at -4.1bp (-8.4bp), Sep'25 at -17.9bp (-24.5bp), Oct'25 at -29.6bp (-37.9bp), Dec'25 at -44.3bp (-54.6bp).

- Cross asset: Stocks rise to earl-mid March high (SPX eminis 64.0 at 6010.0), Gold reversed early support, trades 3314.75 (-37.90).

- USD rallied against broader G10 on the higher-than-expected headline, but the net revisions left a close-to-neutral read for FX markets here: EUR/USD dipped to 1.1372 to 1.1400 by the close.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.29% (+0.01), volume: $2.685T

- Broad General Collateral Rate (BGCR): 4.27% (+0.00), volume: $1.087T

- Tri-Party General Collateral Rate (TCR): 4.27% (+0.00), volume: $1.054T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $118B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $298B

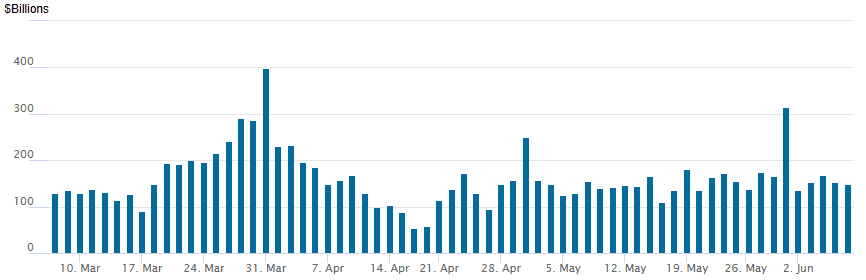

FED Reverse Repo Operation

RRP usage slips to $149.284B this afternoon from $152.727B yesterday, total number of counterparties at 24. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

US SOFR/TREASURY OPTION SUMMARY

With a few exceptions, Friday's SOFR & Treasury option trade focused on upside call buying - looking for a rebound in the late week FI selling, and vol structure selling. Some large put spread buying was reported in SOFR year end options, however, as projected rate cut pricing continued to consolidate vs. morning levels (*) as follows: Jun'25 at 0.0bp (-0.6bp), Jul'25 at -4.1bp (-8.4bp), Sep'25 at -17.9bp (-24.5bp), Oct'25 at -29.6bp (-37.9bp), Dec'25 at -44.3bp (-54.6bp).

SOFR Options:

+47,000 SFRZ5 95.37/95.62 put spds, 1.50-1.75 ref 96.09

+30,000 SFRU5 95.93 calls, 10.5 vs. 95.855/0.25%

Block, 8,000 0QM5 96.37/96.50 put spds, 6.5vs. 96.44/0.32%

+20,000 SFRU5 95.50/95.75/96.00 puyt fly vs. 95.68/95.93/96.18 put fly spd, 7.75-8.0

Block, 5,000 SFRH6 96.00 puts, 16.5 vs. 96.31/0.30%

+10,000 SFRU5 96.75/97.50 call spds, 1.5 ref 95.86

+10,000 SFRV5 95.75/95.87/96.00 put flys, 1.75 ref 96.11

+10,000 SFRH6 98.00/99.00 2x3 call spds 5.5

+5,000 SFRN5/SFRQ5/SFRU5 95.75/95.93/96.00/96.18 call condor strip, 13.0 red 95.865

Update, +35,000 SFRH6/SFRM6 98.62 call strip, 6.0

Block, 5,000 SFRZ5 95.43/95.56/95.62/95.75 put condors, 2.5 vs. 96.13/0.04%

Block: +7,000 SFRZ5/SFRH6 95.68/95.87 put spd spd, 2.0 net/Dec over

Block/total, -18,500 SFRU5 95.25/95.75 put spds, 5.5

Block, -8,500 SFRU5 95.25/95.75 put spds, 5.5 ref 95.86

+2,000 2QU5 96.50 straddles, 45.5

-5,000 SFRU5 96.00 calls, 9.0 ref 95.86

+10,000 SFRZ5 95.62/95.87/96.12/96.37 call condors 6.0 over 96.25/96.50/96.75/97.00 call condor roll-down

-1,500 0QM5 96.50 straddles, 12.5

-5,000 SFRU5 96.00 calls, 9.5 rtef 95.86

-5,000 0QN5 96.68 puts, 17.5

-2,500 SFRZ5 96.25/96.43 call spds, 5.0 ref 96.135

-4,000 0QM5 96.50 calls, 7.5 ref 96.52

-5,000 SFRV5 97.00/98.00 call spds 3.75-4.0

+4,000 0QM5 96.43/96.50 put spds, 2.0 ref 96.59

-3,000 SFRN5/SFRQ5 96.25 call strip vs. 0QN5/0QQ5 97.25 call strip, 0.0

+2,000 0QN5 96.37/96.50/96.62 put flys, 2.0 ref 96.68

4,500 SFRN5 96.25/0QN5 97.25 call spds

+2,000 SFRZ5 96.50/97.00 call spds, 8.5 ref 96.21

Treasury Options:

-10,000 TYN5/TYU5 109.5 put calendar spread, 47 net/Sep over

2,000 FVN5 108.75/109.25/109.75 call flys

8,800 TUN5/TUQ5 104 call spds, 5

5,750 FVN5 108.25/109 call spds, .5 ref 107-21

over 5,000 TYN5 110.25 straddles

+8,000 TYN5 109.5 puts, 15

-15,000 USN5 115 calls, 15

over 9,600 TUN5 104 calls, 2 ref 103-17.5 to -17.88

2,300 TYN5 110.75 calls, 20 ref 110-11.5

2,200 wk1 TY 110.75/111/111.25 put trees (exp today)

over +/-12,400 TYN5 112 calls, 11-10

+4,000 wk1 Fri FV 108.75 calls, 2 (exp today)

+2,500 FVU5 109/111/113 call flys, 17

2,000 FVN5 106.5/107/108 2x3x1 broken put flys

2,000 wk2 FV 108 puts, 13.5

1,500 TYN5 108.5/109.5 put spds ref 110-27

1,900 TUN5 103.88 calls

MNI BONDS: EGBs-GILTS CASH CLOSE: Bunds Partially Fade Post-ECB Selloff

Core EGBs erased most of a nascent rally Friday, with Gilt yields finishing wider.

- The German curve bull flattened in early trade, fading the bear steepening following Thursday's ECB meeting, and weak French and German industrial production numbers helping the bid.

- Gilts ticked higher in sympathy but didn't keep pace with core EGBs.

- A solid US employment report in early afternoon saw Bunds and Gilts weaken in line with Treasuries, reversing much of the earlier yield drop.

- On the day, the German curve twist flattened, with Gilts underperforming Bunds and the UK belly underperforming.

- For the week however, Gilts outperformed Bunds. There was light bear steepening registered in both the German (2Y +1.8bp, 10Y +8bp) and UK (2Y -1.0bp, 10Y -0.3bp) curves.

- 10Y BTP/Bund spreads closed at another 4-year low. with periphery/semi-core EGBs broadly strengthening.

- Next week brings the UK April/May labour market report (Tuesday) and 2025 Spending Review (Wednesday), with the ECB Wage Tracker also out (Wednesday).

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.7bps at 1.88%, 5-Yr is up 0.4bps at 2.175%, 10-Yr is down 0.6bps at 2.576%, and 30-Yr is down 1.6bps at 3.009%.

- UK: The 2-Yr yield is up 0.6bps at 4.013%, 5-Yr is up 2.9bps at 4.155%, 10-Yr is up 2.8bps at 4.644%, and 30-Yr is up 1.4bps at 5.339%.

- Italian BTP spread down 1.8bps at 92.6bps / Greek down 2.4bps at 69.8bps

MNI EGB OPTIONS: Notable Bund Put Spread, Euribor Call Condor Buying

Friday's Europe rates/bond options flow included:

- RXN5 130.00/129.50ps bought for 13.5 in 20k

- ERU5 98.37/98.50/96.62c fly, sold at 0.5 in 6k.

- ERU5 98.06/98.18/98.25/98.37c condor, bought for 4.5 in 12k

- ERZ5 98.125/98.00/97.9375p ladder, bought for 2.25 in 2.25k

- 0RU5 98.00p, bought for 7.25 up to 7.5 in 10k (ref 98.165)

MNI FOREX: USD Index Rises 0.5% Following ‘Solid’ Jobs Report

- After some initial two-way price action in the immediate aftermath of the US employment report, the greenback has strengthened, prompting the USD index to rise 0.5% and look set to close back above the 99.00 mark. Optimistic price action for equities has weighed on the Japanese Yen, which underperforms across G10.

- A higher-than-expected 139k change in nonfarm payrolls was offset by lower revisions to the April figure and a high unrounded unemployment rate of 4.244%. However, the dollar was well supported as markets focus on the sizeable beat for average hourly earnings growth, which of course follows yesterday's surprisingly strong ULC increase for Q1 at 6.6% annualized. The Fed’s Harker said he sees steadiness in 'solid' latest job data.

- After a quick spike to 144.68, USDJPY quickly faded but the pair was subsequently well supported on a dip to 144.10. Fresh weekly highs then ensued, with the pair rallying as high as 145.09, essentially matching the initial target of the 50-day exponential moving average. The latest headlines/timeline on a US/China meeting has likely provided an additional tailwind, feeding into the cautious optimism surrounding global trade negotiations.

- While moving average studies have remained in a bear-mode position, they have continued to be tested in recent weeks. A close above the 50-day EMA, intersecting at 145.15, would bolster a bullish threat for USDJPY, while key short-term resistance has been defined at 146.28, the May 29 high.

- Elsewhere, adjustments for the likes of EUR, AUD, NZD and GBP are more reflective of the broader dollar index shift, with the Canadian dollar slightly outperforming following the above-expected Canadian employment data. USDCAD temporarily breached support on Thursday – trading below 1.3643 for the first time since early October last year. Below here, attention will be on 1.3579, the 1.5 Fibonacci projection of the Feb 3 - 14 - Mar 4 price swing, before the September lows at 1.3420 will garner attention.

- The most recent trend of a strengthening Mexican peso is prevailing as we approach the weekend. A close at current levels below 19.15 would provide another lowest USDMXN close for the cycle, bolstering bearish conditions following the significant range breakout in April. Potential is seen for an extension towards 18.7774, the 50.0% retracement of the Apr 9 ‘24 - Feb 3 bull leg, followed by the Aug ’24 lows around the 18.60 mark.

- Chinese CPI/PPI and trade data will take focus on Monday. US CPI is due Wednesday.

MNI FX OPTIONS: Expiries for Jun09 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1300(E797mln), $1.1350(E1.4bln), $1.1375(E572mln), $1.1425(E1.9bln), $1.1500(E775mln), $1.1520-30(E828mln), $1.1600(E1.6bln)

- USD/JPY: Y143.55-65($982mln), Y144.00($660mln), Y145.00($512mln)

- EUR/GBP: Gbp0.8440-50(E680mln)

MNI US STOCKS: Late Equities Roundup: US/China Talks in London Next Week

- Stocks maintained positive footing late Friday, back near the highest levels since early to mid-March after this morning's better than expected jobs gains were reported for May. Pres Trump touting a meeting with US & China trade officials in London next week underscored support for risk in late trade.

- Currently, the DJIA trades up 433.02 points (1.02%) at 42752.77, S&P E-Minis up 67 points (1.13%) at 6012.75, Nasdaq up 266.7 points (1.4%) at 19564.98.

- Energy and Consumer Discretionary sectors continued to outperform in late trade, oil and gas stocks leading gainers in the Energy sector as crude prices inexplicably gained (WTI +1.25 at 64.65) after Saudi Arabia expressed interest earlier in the week for raising production: APA +3.50%, Coterra Energy +2.94%, Devon Energy +2.56% and EOG Resources +2.55%.

- The Consumer Discretionary sector was buoyed by a rebound in Tesla by +5.45% after losing over 11% late Thursday. Meanwhile, Best Buy gained 3.80%, Airbnb +2.98% and Starbucks +2.72%. Of note, Lululemon Athletica fell -20.04% on downgrades and tariffs sapping profits since early April Liberation Day.

- Conversely, Utilities and Consumer staples sectors continued to underperform, PG&E -1.85%, CenterPoint Energy -0.65%, Consolidated Edison -0.54% and Dominion Energy -0.46% weighed on the former. Meanwhile, leading laggers in the Consumer Staples included Dollar Tree -2.39%, Kimberly-Clark -1.11%, PepsiCo -0.88% and Hershey -0.76%.

MNI EQUITY TECHS: E-MINI S&P: (M5) Bullish Trend Sequence

- RES 4: 6124.00 High Feb 24

- RES 3: 6080.75 High Feb 26

- RES 2: 6057.00 High Mar 3

- RES 1: 6016.50 High Junb 5

- PRICE: 6003.75 @ 14:19 BST Jun 6

- SUP 1: 5871.05/5780.89 20- and 50-day EMA values

- SUP 2: 5756.50 Low May 23

- SUP 3: 5596.00 Low May 7

- SUP 4: 5455.50 Low Apr 30

The trend condition in S&P E-Minis is unchanged, it remains bullish and the contract traded to a fresh cycle high yesterday. The recent break of 5993.50 last week, the May 20 high and a bull trigger, highlights a resumption of the uptrend and maintains a price sequence of higher highs and higher lows. A continuation would open 6057.00 next, the Mar 3 high. Key support lies at 5780.89, the 50-day EMA.

COMMODITIES

MNI AMERICAS OIL: WTI crude has risen today on improved sentiment

Americas End-of-Day Oil Summary: WTI crude has risen today on improved sentiment after higher-than-expected nonfarm payrolls showed a resilient US labor market, while Navarro said a US-China meeting was likely within a week. Prices faced pressure earlier in the week after reports that Saudi Arabia was seeking further large OPEC+ output hikes. However, another decline in the rig count provided late support.

- China's official news agency Xinhua reported that US President Donald Trump and Chinese President Xi Jinping spoke Thursday. Trump acknowledged that the trade relationship had 'gotten off track'.

- Geopolitical concerns over Russian and Iran and tight near-term fundamentals supported by Canadian wildfires have driven upside pressure on oil markets this week.

- The headline oil supply increase of 411k b/d m/m for July by OPEC+ will likely translate into a boost of 225k b/d, according to an FGE note cited by Bloomberg.

- OPEC+ members are expected to agree to two large output hikes for August and September at their next meetings, HSBC research said.

- US President Donald Trump has told reporters in the Oval Office that he will greenlight new sanctions on Russia if he sees a moment "when we're not going to make a deal and this thing won't stop."

- WTI July futures were up 1.9% at $64.58

- WTI Aug futures were up 1.9% at $63.65

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 09/06/2025 | 0500/1400 | Economy Watchers Survey | ||

| 09/06/2025 | 0900/1100 | ECB Elderson On Rule Of Law At Italian Court | ||

| 09/06/2025 | - | *** | Trade | |

| 09/06/2025 | 1400/1000 | ** | Wholesale Trade | |

| 09/06/2025 | 1400/1000 | ** | Wholesale Trade | |

| 09/06/2025 | 1500/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 09/06/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 09/06/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 10/06/2025 | 2301/0001 | * | BRC-KPMG Shop Sales Monitor |