MNI ASIA MARKETS ANALYSIS: Tariff Talk Leaves Stocks on Edge

HIGHLIGHTS

- Treasuries look to finish weaker, off low end of a narrow session range, dearth of economic data (NY Fed 1Y inflation exp lower than exp) - the main focus is on June FOMC minutes release Wednesday at 1400ET.

- Markets on edge as Pre Trump discussed tariffs at latest cabinet meeting: the administration could have been much harsher on trade, and could "go higher".

- Trump announced a 50% tariff on cooper and will announce more on "pharma, chips, other things.." after threatening a 200% duty on pharmaceuticals.

- Focus on Wednesday's FOMC minutes release for the June meeting at 1400ET.

US TSYS

MNI US TSYS: Tsys Hold Narrow Range Ahead June FOMC Minutes, Tariff Talk

- Treasuries look to finish moderately weaker, off low end of a narrow session range. Second consecutive day of limited economic data (NY Fed 1Y inflation exp lower than exp) with focus on Wednesday afternoon's June FOMC minutes release at 1400ET.

- The June minutes should underline the Committee's patience in making its next rate move amid heightened tariff-related economic uncertainty, as encapsulated in the meeting's Dot Plot which showed participants largely divided between no cuts and 2 cuts by year-end.

- Markets also on edge as Pres Trump discussed tariffs at latest cabinet meeting: the administration could have been much harsher on trade, and could "go higher". Trump announced a 50% tariff on cooper and will announce more on "pharma, chips, other things.." after threatening a 200% duty on pharmaceuticals.

- Commerce Secretary Lutnick said on CNBC he "expects 15-20 trade letters to go out over the next two days" while studies on pharmaceuticals and semiconductors will be done by the end of the month.

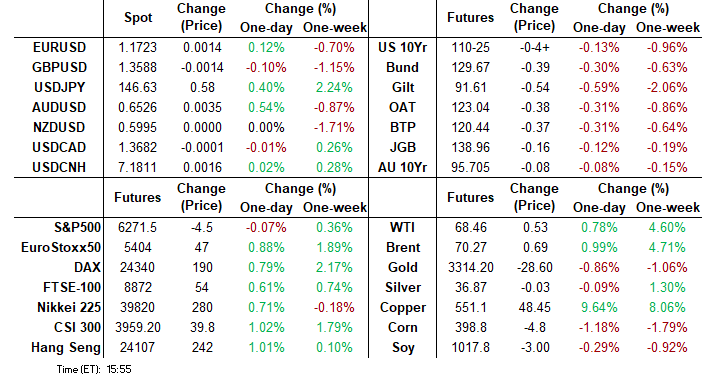

- Currently, the Sep'25 10Y trades -4 at 110-25.5 (110-21.5L / 111-01.5H), above initial technical support at 110-17 61.8% of the May 22 - Jul 1 bull leg. Curves mixed: 2s10s +2.333 at 50.608; 5s30s -0.094 at 95.467.

- USD off highs, Bbg index BBDXY +0.32 at 1196.83 vs. 1199.72 high; Gold weaker (-31.5 at 3305.0), stocks inching lower late: SPX eminis -5.5 at 6270.75.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.33% (-0.02), volume: $2.814T

- Broad General Collateral Rate (BGCR): 4.31% (-0.01), volume: $1.136T

- Tri-Party General Collateral Rate (TCR): 4.31% (-0.01), volume: $1.106T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $118B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $263B

FED Reverse Repo Operation:

RRP usage inches up to $219.415B this afternoon from $218.030B yesterday, total number of counterparties at 37. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021 - compares to yesterday's (July 1) $460.731B highest usage since December 31.

US SOFR/TREASURY OPTION SUMMARY

Two-way SOFR & Treasury option flow on moderate volumes reported Tuesday. Underlying futures remain under pressure amid ongoing tariff related headlines keeping risk tethered, curves steeper with the short end outperforming. Projected rate cut pricing largely steady vs late Monday (*) levels: Jul'25 steady at -1.2bp, Sep'25 steady at -17.3bp, Oct'25 steady at -31.7bp, Dec'25 at -48.6bp (-49.9bp).

SOFR Options:

+8,000 SFRM6 96.25/97.00 strangles 3.5 over SFRZ5 96.12 straddles

+2,000 SFRZ5 96.00 calls, 24.0 vs. 96.13/0.64%

-5,000 SFRQ5 95.68/96.06 strangles, 2.5

-3,500 2QU5 96.50/96.87 strangles, 19.0 ref 96.67

-10,000 0QU5 97.12/98.12 call spds, 5.5 ref 96.735

+4,000 SFRU5 95.75/95.87 call spds, 6.5 ref 95.865

+7,000 SFRZ5 95.62 puts, 1.0 vs. 96.165/0.07%

+2,000 SFRZ5 96.56/96.81 call spds vs. 95.75/95.87 put spds, .25 net +c spd

3,000 SFRU5 95.62/95.75 put spds ref 95.86

8,900 SFRZ5 96.25/96.50 call spds, 6.0 ref 96.15

+2,250 SFRZ5 95.50/96.00 put spds vs. 97.00/97.50 call spds, 8.0 net ref 96.155/0.38%

Treasury Options:

appr 12,000 TYQ5 110.5/111 strangles, 44

1,500 TYU5 111/112.5 call spds 28 ref 110-23.5

Block, 10,000 FVQ5 109.25 calls, 3 ref 108-03.5

2,000 FVU5 110 calls, ref 108-04

2,000 TYQ5/TYU5 111.5 call spds, 21 ref 110-24.5

2,000 TYQ5 111.75/112.25 call spds, 7

+15,000 TYU5 113 calls, 13

1,500 TYQ5 109/109.5/110.5 broken put flys, 17 ref 110-23.5

Block, +10,000 FVQ5 109.25 calls, 3 ref 108-03.5 (laid off on screen)

-3,000 TYQ5 110/112 call over risk reversals, 7

-20,000 FVQ5 108 puts, 15 vs. 108-05.25/0.41%

-1,700 TYU5 109 puts, 15

+1,500 TYU5 109/110 put spds 2 over 113 calls ref 110-28

over 4,000 TYV5 104 puts, ref 110-24.5

MNI BONDS: EGBs-GILTS CASH CLOSE: Further Bear Steepening

European yields rose Tuesday, with continued curve steepening.

- Core FI was under pressure from the open, following on from Monday's weak close. There were multiple cause driving weakness, including supply (Netherlands, Austria, EU) along with a 3-week extension of the US's tariff negotiation deadline to Aug 1.

- While there was little immediate market reaction, the release of the UK OBR's Fiscal Risks and Sustainability Report reminded of longer-term fiscal concerns.

- Yields rose steadily all morning before before steadying in afternoon trade. 10Y Gilt yields pushed through the July 2 highs to hit the highest levels in a month.

- 10Y Bund yields hit a fresh 3-month intraday high of 2.707% but ultimately held on to the 2.70% area (mid-May highs).

- The UK and German curves both bear steepened, though short-end Gilts outperformed.

- Periphery/semi-core EGB spreads were mixed, with Greece outperforming.

- Wednesday's calendar includes appearances by ECB's Lane, Guindos and Nagel and the release of the BOE's FSR, though it's a lighter day for data including Greek June inflation. There will also be focus on EU-US trade negotiations, with President Trump saying after the European cash close that a tariff "letter" to Brussels is probably two days away.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 3.5bps at 1.872%, 10-Yr is up 4.4bps at 2.687%, and 30-Yr is up 5.4bps at 3.172%.

- UK: The 2-Yr yield is up 0.8bps at 3.872%, 5-Yr is up 3.1bps at 4.042%, 10-Yr is up 4.7bps at 4.633%, and 30-Yr is up 6.3bps at 5.454%.

- Italian BTP spread up 0.2bps at 85bps /Greek down 0.6bps at 68.8bps

MNI OPTIONS: Pickup In Bund Option Activity, As Mixed Rates Trades Continue

Tuesday's Europe rates/bond options flow included:

- OEQ5 117.25/117.50cs sold at 12 in 8k

- RXQ5 128.50/127.50 put spread 3K given at 15.

- RXQ5 130.5/131.5cs vs 128p, bought the cs for 3 in 2k.

- ERZ5 98.3125/98.4375/98.5625c fly vs 97.9375p, bought the fly for flat in 3.5k.

- ERZ5 98.00/97.9375ps, bought for 1.5 in 3k.

- ERM6 98.375/98.25/97.9375p ladder, bought for flat up to half in 9k

- SFIZ5 96.15p x2 vs 96.50c x1, sold the Call at -2.75 in 4k

- SFIH6 96.80/97.00 call spread paper paid 3.75 on 5K

MNI FOREX: AUD Remains Higher Post RBA, JPY Weakness Extends

- The greenback is consolidating another positive session on Tuesday, with the USD index extending its latest recovery and rising ~0.3%. Renewed tariff related uncertainty appears to be underpinning the renewed optimism, with the latest rhetoric from President Trump doing little to change the tone.

- In similar vein to Monday’s session, the Japanese yen is one of the poorest performing currencies in G10 amid the specific uncertainty related to a US trade deal with Japan and the Japanese PM stating that comprehensive negotiations will continue in the weeks ahead. USDJPY has also benefitted from the higher core yields backdrop, and rose as high as 146.98, further narrowing the gap to the June 23 spike high of 148.03.

- At the other end of the spectrum, the Australian dollar continues to outperform in G10 following the surprise RBA rate hold, against firm market expectations for a 25bp cut. The pair has settled around the 0.6520 mark and a bullish trend set-up is maintained, with the latest pullback considered technically corrective.

- Standing out on the chart is AUDJPY (+1.10%), which has risen above an important area of resistance around 95.75 which aligns with the March and May highs from earlier in the year. Further upside would target a move towards the February highs at 97.33. Notably, CHFJPY is now trading above 184.00, fresh record highs for the cross. This extends the rally from the June lows to 5.8%.

- China’s CPI/PPI data will precede Wednesday’s calendar highlight of the RBNZ decision, where a majority of analysts expect a rate hold at 3.25%. Later on Wednesday, FOMC minutes are scheduled.

MNI OPTIONS: Expiries for Jul09 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600(E536mln), $1.1675-90(E742mln), $1.1700(E1.7bln)

- USD/JPY: Y144.00-10($1.4bln), Y144.50($860mln)

- EUR/GBP: Gbp0.8655-65(E633mln)

- AUD/USD: $0.6425(A$700mln), $0.6550(A$557mln)

- NZD/USD: $0.6075(N$519mln)

MNI US STOCKS: Late Equities Roundup: Tariff Talk Tethers Stocks

- Stocks continue to drift near steady (SPX eminis) to moderately mixed in late Tuesday trade, the DJIA still weaker vs. gains in the Nasdaq. Pres Trump's latest cabinet meeting did little to improve risk appetites. Currently, the DJIA trades down 150.42 points (-0.34%) at 44255.3, S&P E-Minis down 2.5 points (-0.04%) at 6273.25, Nasdaq up 14.1 points (0.1%) at 20426.34.

- Regarding some trade "letters", Trump said “we have some 60, 70%. Those are ones with massive you know, where we have massive trade deficits because they've treated us very badly. But I would say in every case, I'm treating them better than they treated us over the years."

- Trump says that the administration could have been much harsher on trade, and that they have the ability to go higher with tariffs. A few minutes later, Trump announced a 50% tariff on cooper and will announce more on "pharma, chips, other things.." after threatening a 200% duty on pharmaceuticals.

- Utilities and Consumer Staples sectors underperformed in late trade, alternative energy stocks weighed on the former: NRG Energy -4.55%, NextEra Energy -3.06% and Vistra -2.47% while broadline retailers weighed on Consumer Staples: Dollar General -2.82%, Kroger Co -2.13% and Walmart -1.85%.

- On the positive side, Energy and Materials sectors outperformed - oil and gas leading gainers in the former: Devon Energy +7.54%, Halliburton +7.08%, APA +6.08%, Occidental Petroleum +5.72% and Diamondback Energy +5.17%. Stocks supporting the Materials sector included: Albemarle +9.15%, LyondellBasell Industries +5.40%, Dow Inc +5.28%, Freeport-McMoRan Inc +3.55% and Eastman Chemical +3.34%.

- Reminder, the latest corporate earning cycle kicks off next week Tuesday with banks and financial stocks reporting: Blackrock, JPMorgan Chase & Co, Wells Fargo & Co, Bank of New York Mellon, State Street Corp and Citigroup.

MNI EQUITY TECHS: E-MINI S&P: (U5) Bulls Remain In The Driver’s Seat

- RES 4: 6402.44 1.382 proj of the May 23 - Jun 11 - 23 price swing

- RES 3: 6381.00 1.764 proj of the Apr 7 - 10 - 21 price swing

- RES 2: 6356.12 1.236 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6333.25 High Jul 3

- PRICE: 6275.75 @ 14:38 BST Jul 8

- SUP 1: 6235.50 Low Jul 2

- SUP 2: 6151.56/6011.49 20- and 50-day EMA values

- SUP 3: 5811.50 Low May 23

- SUP 4: 5645.75 Low May 7

The trend condition in S&P E-Minis is unchanged, the outlook remains bullish. Resistance at 6128.75, the Jun 11 high, has recently been breached. The break confirmed a resumption of the uptrend that started Apr 7. This has been followed by a breach of key resistance and a bull trigger at 6277.50, the Feb 21 high. Sights are on 6356.12, a Fibonacci projection. Key support is at the 50-day EMA, at 6011.49.

MNI COMMODITIES: Copper Spikes As Trump Announces 50% Tariff, Gold Falls, WTI Gains

- Copper has surged by over 10.0% today to $554/lb after President Trump said he would impose a 50% tariff on the red metal.

- The move saw copper futures spike as high as $589.6, before paring some of the move as the market anticipates the higher price for the US consumer.

- For copper, a bull cycle remains in play and recent gains strengthen a bullish condition. Today’s gains have seen price pierce $546.15, the March 26 high and a key resistance, with sights on round number resistance at $560 next.

- Meanwhile, spot gold briefly pushed through yesterday's low, before paring losses slightly, currently 0.9% down on the session at $3,305/oz.

- Gold has been relatively rangebound in recent weeks, amid continued tariff and geopolitical uncertainty.

- Near-term focus will be on the remaining US "tariff letters" to be sent out over the coming days, although so far these announcements have been taken in their stride, limiting any positive spillovers into gold.

- The recent move lower in gold resulted in a breach of the 50-day EMA, signalling scope for a deeper correction, and opening $3,245.5, the May 29 low.

- A resumption of gains would refocus attention on $3,451.3, the June 16 high.

- Elsewhere, WTI is higher today as the market weighs a new US tariff deadline as well as the August increase in OPEC+ supply and a further potential hike in September.

- WTI Aug 25 is up by 0.6% at $68.3/bbl.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 09/07/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 09/07/2025 | 0930/1030 | BOE Financial Stability Report | ||

| 09/07/2025 | 1000/1100 | BOE FSR Press Conference | ||

| 09/07/2025 | 1045/1245 | ECB Lane At House of the Euro | ||

| 09/07/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 09/07/2025 | 1100/1300 | EC De Guindos Closing Remarks At Conference | ||

| 09/07/2025 | 1400/1000 | ** | Wholesale Trade | |

| 09/07/2025 | 1400/1000 | ** | Wholesale Trade | |

| 09/07/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 09/07/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 09/07/2025 | 1800/1400 | *** | FOMC Minutes |