MNI ASIA MARKETS ANALYSIS: Plying Sidelines Ahead CPI

HIGHLIGHTS

- Off early session highs Treasuries look to finish near the low end of a narrow range on light volume (TYU5 under 870k by the bell, markets await Wednesday's key CPI inflation data.

- Analyst unrounded estimates see core CPI inflation accelerating mildly to 0.27% M/M (median, 0.28% average) in May after 0.24% M/M in April.

- Officials are still working out technical details as US/China trade talks are expected to reconvene in London at 0800 PM (local time)

US TSYS

MNI US TSYS: Narrow Ranges Ahead Midweek CPI Inflation Data

- Treasuries look to finish mixed, off midmorning highs on narrow ranges and light volume (TYU5 under 870k). Market focus on Wednesday morning's key CPI inflation data at 0830ET.

- Analyst unrounded estimates see core CPI inflation accelerating mildly to 0.27% M/M (median, 0.28% average) in May after 0.24% M/M in April. We’ve seen an unrounded range of 0.23-0.34% M/M, with some sizeable discrepancies in used cars and lodging away from home as well as a CPI-specific airfares.

- Officials are still working out technical details as US/China trade talks are expected to reconvene in London at 0800 PM (local time). "LUTNICK: CHINA TALKS WENT REALLY REALLY WELL .. TALKS COULD GO INTO TOMORROW IF NEED BE" Bbg.

- No new developments from California as US Marines deployed to quell any deportation unrest.

- Stocks gaining slightly after the bell after some late program selling tempered support with focus on Wednesday morning's CPI inflation data.

- Cross asset roundup: Bbg US$ index scaling back support late (BBDXY +.99 at 1210.39); crude weaker (WTI -.59 at 64.70), Gold making modest gains: +5.22 at 3331.40.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.29% (+0.00), volume: $2.643T

- Broad General Collateral Rate (BGCR): 4.27% (+0.00), volume: $1.071T

- Tri-Party General Collateral Rate (TCR): 4.27% (+0.00), volume: $1.038T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $114B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $289B

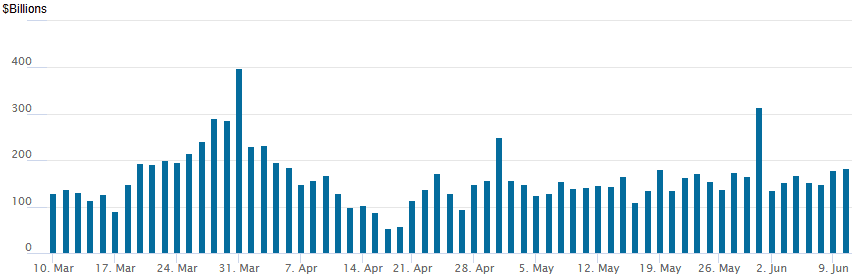

FED Reverse Repo Operation

RRP usage inches up to $182.725B this afternoon from $179.315B yesterday, total number of counterparties at 31. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

US SOFR/TREASURY OPTION SUMMARY

Modest SOFR & Treasury option flow Tuesday, leaning towards wing buyer and at-the-money selling on light volumes as markets await Wednesday's key CPI inflation data. Projected rate cut pricing steady to gaining slightly vs. this morning (*) as follows: Jun'25 steady at 0.0bp, Jul'25 steady at -3.6bp, Sep'25 at -16.9bp (-17.9bp), Oct'25 at -28.6bp (-30.1bp), Dec'25 at -44.2bp (-46.2bp).

SOFR Options:

5,000 SFRZ5 95.75/96.00 put spds ref 96.09

-2,500 SFRZ5 97.12/SFRM6 96.50 straddle strip 127.0 to 126.5

+2,000 0QZ5 97.50/98.50 call spds 2.75 over SFRZ5 97.00/98.0 call spds

1,700 0QM5/0QN5 96.75 call spds

+2,500 SFRZ5 95.62/96.00 1.25 over 0QZ5 96.12/96.50 put spds

+18,000 0QV5 95.87/96.12/96.37 put trees, 4.25-4.5 ref 96.64 to -.62(+25k Mon 3.5-4.25)

+4,000 SFRN5 95.68/95.75/95.81 2x3x1 put flys, 0.5 ref 95.87

+10,000 0QU5 96.37/96.62/96.87 call flys, 4.5 ref 96.665 to -.605/0.05%

-3,500 SFRU5 95.75/95.93/96.00 broken put trees, 2.0 ref 95.865

Treasury Options:

2,000 TYU5 116 calls ref 110-07

5,000 TYN5 109.5 puts, 10 ref 110-12.5

2,000 TYQ5 107/109 put spds ref 110-13.5

4,000 wk1 TY 111/112/112.5 call flys ref 110-12.5 (exp 7/3)

10,000 Wed wkly FV 107.75 puts, 7.5 ref 107-26

3,000 wk2 TY 109.5/110.5 put spds ref 110-11.5 (exp Fri)

2,000 FVN5 106.25/107.25 put spds, ref 107-26.5

2,000 TYN5 111.25/112/112.25 broken call trees ref 110-11

1,100 USN5 117/120/121 broken call flysref 112-29

-2,000 wk2 FV 107.75 puts, 7.5

+4,000 TYN5 111.25 calls, 9

Block, +6,000 wk2 TY 111 calls, 5 ref 110-12 (exp Fri)

+3,000 TYQ5 108.5/112 call spds 151 vs. 110-11.5/0.55%

1,250 TUQ5 103.75/104 2x3 call spds vs. 2,500 TUQ5 103.12 puts ref 103-17.62

Block, +10,000 USN5 115 calls, 13 ref 112-28

+3,500 TYU5 107/108 put spds, 11 vs. 111-09/0.08%

+4,500 Wed wkly TY 109.25/109.5/109.75/110 put condors, 3 vs. 110-11.5/0.5%

+1,500 TYN5 108.75/112.25 strangles, 6

MNI BONDS: EGBs-GILTS CASH CLOSE: Rally Extends On Softening UK Jobs Data

European yields fell for the second day this week Tuesday, with Gilts outperforming Bunds.

- Gains were basically steady throughout the session, as some of last week's ECB-related selloff continued to reverse.

- Data out early in the session confirmed that the UK labour market is softening at an increasing pace, with AWE wage data on track to come in even lower in Q2 than the BOE’s Q1 forecast miss, and HMRC payrolls data pointing to growing slack. Our analysis of the release is here (PDF).

- The data saw BOE cut pricing rise to nearly 50bp for the year, up from 41bp prior.

- The UK curve leaned bull steeper, with the belly outperforming. Germany's bull flattened.

- Periphery / semi-core EGB spreads were mixed, with BTPs once again outperforming and 10Y now targeting the 90bp level vs Bunds.

- Wednesday is light for European data, with the main highlight expected to be the ECB Wage tracker. Most attention will be on US CPI. We also hear from ECB's Lane, Makhlouf, and Cipollone.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1.7bps at 1.847%, 5-Yr is down 3.3bps at 2.123%, 10-Yr is down 4.4bps at 2.523%, and 30-Yr is down 4.2bps at 2.97%.

- UK: The 2-Yr yield is down 8.4bps at 3.919%, 5-Yr is down 9bps at 4.048%, 10-Yr is down 9bps at 4.542%, and 30-Yr is down 7.4bps at 5.254%.

- Italian BTP spread down 0.7bps at 91.3bps / French OAT unchanged at 67.2bps

MNI FOREX: GBP Remains Moderately Lower Post Soft UK Labour Market Data

- Currency markets have traded in a more subdued fashion Tuesday, as market participants continue to await any details on developments regarding US/China trade talks, which remain ongoing in London as the European session comes to an end. As of 1730BST, the dollar index is just 0.1% green, giving back a small portion of yesterday’s decline.

- GBP if off its worst levels, but remains a standout underperformer following the softer set of UK labour market data releases. Weakness in GBP came in two phases in early trade, first on the weak payrolls data, and then again on the SONIA open, with GBPUSD briefly piercing 1.3462, its 20-day EMA. A clear break of this average would suggest potential for a deeper correction and expose the 50-day EMA for direction, at 1.3299. Cable has since recovered back above 1.35 as we approach the APAC crossover.

- EURGBP stands 0.35% higher on the day, and in the process has breached a key short-term resistance at 0.8440, the 50-day EMA. A clear break of the average is required to highlight a stronger reversal, potentially exposing 0.8541, the May 02 high.

- Dips below the 0.8400 handle have been well supported in recent months, and key support has been defined at 0.8356, the May 29 low. Clearance of this level would be required to resume the technical downtrend.

- USDJPY had some early volatility on Tuesday, as initial Ueda comments prompted the pair to trade up to 145.29 and eclipse the post-payrolls high. Spot then subsequently moved lower following some temporary weakness for equities but found solid support between 144.40/50.

- Aside from potential headlines on US/China developments, all attention now turns to the US May inflation data due Wednesday, an important pre-FOMC steer.

MNI FX OPTIONS: Expiries for Jun11 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1300(E2.2bln), $1.1400(E2.2bln), $1.1498-00(E1.0bln)

- USD/JPY: Y143.00($889mln), Y144.90-00($1.2bln)

- GBP/USD: $1.3450(Gbp758mln), $1.3600-05(Gbp565mln)

- AUD/USD: $0.6350-65(A$1.0bln) $0.6495-00(A$799mln)

- USD/CAD: C$1.3760($570mln), C$1.3800($527mln)

MNI US STOCKS: Late Equities Roundup: Modest Gains Inside Narrow Ranges

- Stocks hold mildly higher levels late Tuesday, inside narrow ranges after some late program selling tempered support with focus on Wednesday morning's CPI inflation data. Officials are still working out technical details as US/China trade talks are expected to reconvene in London at 0800 PM (local time).

- Currently, the DJIA trades up 50.6 points (0.12%) at 42808.12, S&P E-Mini Futures 22.25 points (0.37%) at 6032.5, Nasdaq up 74.9 points (0.4%) at 19666.14.

- Energy and Communication Services sectors continued to lead gainers in late trade, the former buoyed by APA Corp +4.37%, Schlumberger +3.68%, Halliburton +3.33%, ConocoPhillips +3.33% and EOG Resources +3.02%

- Interactive media shares supported the Communication Services sector: Warner Bros Discovery +5.19%, Interpublic Group +2.69%, Walt Disney +2.49%, AT&T +2.44% and Comcast +2.41%

- Industrials and Financials underperformed in late trade, the former weighed by General Electric -4.07, GE Vernova -3.23%, Howmet Aerospace -2.78%, Axon Enterprise -2.76% and Quanta Services -2.52%

- Laggers in the Financials led by insurance names with Brown & Brown -3.35%, Arch Capital Group -2.52%, Marsh & McLennan -2.01% and Progressive -1.92% and Allstate Corp -1.75%.

MNI EQUITY TECHS: E-MINI S&P: (M5) Uptrend Remains Intact

- RES 4: 6124.00 High Feb 24

- RES 3: 6080.75 High Feb 26

- RES 2: 6057.00 High Mar 3

- RES 1: 6040.75 Intraday high

- PRICE: 6021.50 @ 14:38 BST Jun 10

- SUP 1: 5896.00/5798.36 20- and 50-day EMA values

- SUP 2: 5756.50 Low May 23

- SUP 3: 5596.00 Low May 7

- SUP 4: 5455.50 Low Apr 30

The trend condition in S&P E-Minis is unchanged, it remains bullish and the contract has again traded to a fresh cycle high, today. The recent break of 5993.50, the May 20 high and a bull trigger, highlights a resumption of the uptrend and maintains a price sequence of higher highs and higher lows. A continuation would open 6057.00 next, the Mar 3 high. Key support lies at 5798.36, the 50-day EMA.

MNI COMMODITIES: Crude, Gold Edge Lower As US-China Talk Developments Awaited

- Crude markets have erased earlier gains to lose ground on the day, as the market awaits developments from a second day of US-China trade talks in London.

- WTI Jul 25 is down by 0.9% at $64.7/bbl.

- US Commerce Secretary Lutnick described negotiations yesterday as “fruitful” and have continued throughout today.

- Elsewhere, the Iranian Foreign Ministry has reported that a sixth round of indirect talks between Iran and the US will take place in the Omani capital, Muscat, on Sunday, 15 June.

- WTI futures remain above the 50-day EMA, signalling scope for an extension towards $65.82 next, the Apr 4 high.

- It is still possible that the recovery since early May is a correction, however, and support to watch lies at $59.74, the May 30 low.

- Meanwhile, spot gold has struggled for direction as the outcome of the US-China talks remain key for near-term sentiment. The yellow metal has edged down by 0.1% to $3,323/oz.

- The latest pullback in gold appears corrective in nature, and medium-term trend signals remaining bullish.

- Initial support to monitor in the event of a positive tariff outcome is the 50-day EMA at $3,242.4, which shields key support at $3,121.0, the May 15 low.

- Should these support levels hold, or if talks do not bring a de-escalatory outcome, it may provide a platform to build back towards the June 5 high at $3,403.5 and the May 7 high of $3,435.6.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 11/06/2025 | 0630/0730 | BOE Saporta Speech At Bank of Finland and SUERF Conference | ||

| 11/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 11/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 11/06/2025 | 0930/1130 | ECB Lane At 2025 Government Borrowers Forum | ||

| 11/06/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 11/06/2025 | 1130/1230 | Chancellor Reeves presents Spending Review to Parliament | ||

| 11/06/2025 | - | *** | Money Supply | |

| 11/06/2025 | - | *** | New Loans | |

| 11/06/2025 | - | *** | Social Financing | |

| 11/06/2025 | 1200/1400 | ECB Cipollone On Digital Payments Panel | ||

| 11/06/2025 | 1230/0830 | * | Building Permits | |

| 11/06/2025 | 1230/0830 | *** | CPI | |

| 11/06/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 11/06/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 11/06/2025 | 1800/1400 | ** | Treasury Budget |