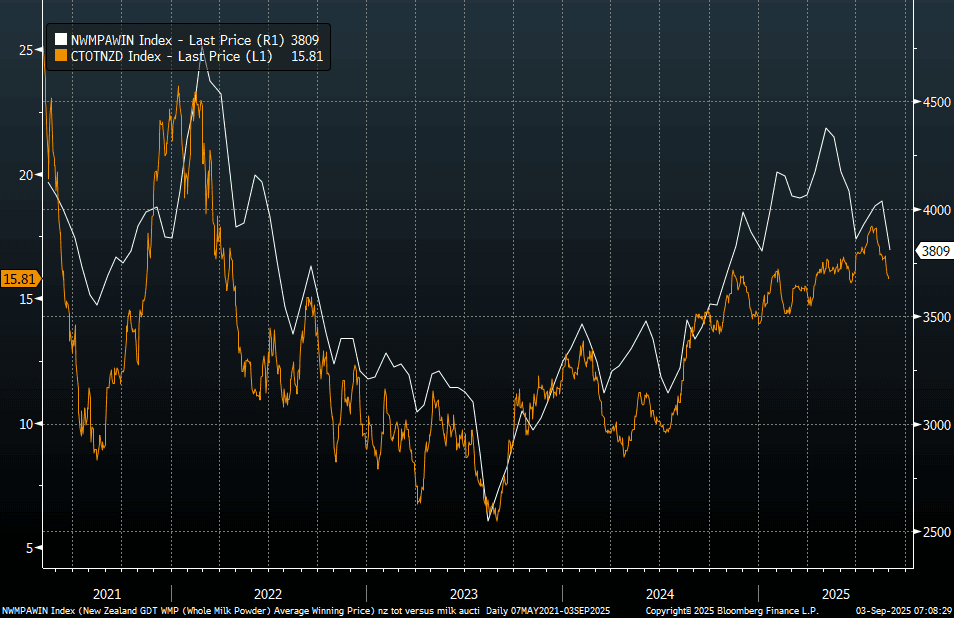

NEW ZEALAND: Milk Power Auction Price Falls, Back To Late 2024 Levels

Overnight the average price for whole milk powder fell to $3809 versus $4036 at the previous auction, per GDT . This was a 5.3% drop. The chart below plots this price index against the Citi NZ terms of trade proxy. The whole milk powder price is now at fresh lows for 2025. The terms of trade proxy has matched this fall recently.

- BBG noted: "The GDT price index change, which is a weighted average of the percentage changes in individual milk products between trading events, was a decrease of 4.3%."

- Later today we get NZ ANZ commodity prices for August.

Fig 1: Whole Milk Powder Prices & Citi NZ Terms Of Trade Proxy

Source: Citi/Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USD: Goldman Sachs See Renewed USD Downside Risks, Likes Short USD/JPY

The global bank weighs in on the USD outlook post Friday's jobs report, noting it re-asserts USD downside risks. It likes USD/JPY, see below for more details.

Goldman Sachs: "USD: Whiplash week. For much of the week, our Dollar views were on the wrong side of market moves, but the substantial revisions to the employment situation should, in turn, revise the emerging narrative that the FX reaction to tariffs has changed again. On the tariff narrative, we see three key aspects to our view that the Deals should not derail Dollar downside. First, and most fundamentally, we expect that the US will bear most of the cost of the tariffs, which will weigh on its terms of trade. This is partly because of the breadth of the tariff increases, which will make it difficult for US firms and consumers to find suitable substitutes. This is where we disagree with the market and media narrative this week that individual deals were more negative for trading partners because of the disparity in tariff rates. Second, it is likely that a part of the Dollar’s depreciation in April stemmed from expected US underperformance—as the elevated occurrence of “sell America” days demonstrates—and arguably that has looked less compelling lately. This is where the NFP revisions are most important, as they change the picture from the labor market looking—in Chair Powell’s words—“quite solid” to now aligned with the softer growth data. Third, we and others noted that part of the Dollar’s decline was due to the back-and-forth nature of the implementation and hard-to-pin policy goals. Admittedly, this has changed somewhat—or at least has become less surprising—since the initial Liberation Day market response, and it is hard to make an exact attribution to each of these factors. But we think concerns over institutional governance will continue to weigh on the Dollar. And while rate cuts are not required for further Dollar downside, they obviously would still help. With the changing labor market landscape, we expect markets will price some likelihood of nearer, deeper and faster Fed cuts. That should be especially important for the Yen, which would benefit both from rising recession concerns and shifting hedging costs when the curve bull steepens, which is why we now recommend investors go short USD/JPY. While we acknowledge the difficult trading environment, we think the price and positioning cleanse this week offer compelling entries to re-engage on the Dollar downside thesis, and think the employment report supports this view."

JGB TECHS: (U5) NFP Tips Prices Sharply Higher

- RES 3: 147.74 - High Jan 15 and bull trigger (cont)

- RES 2: 146.53 - High Aug 6

- RES 1: 141.48/142.95 - High May 2 / High Apr 7

- PRICE: 138.63 @ 17:23 GMT Aug 1

- SUP 1: 137.32 - Low Jul 25

- SUP 2: 136.57 - 1.382 proj of the Jan 28 - Feb 20 - Feb 26 bear leg

- SUP 3: 134.89 - 2.000 proj of the Jan 28 - Feb 20 - Feb 26 bear leg

JGBs rallied sharply alongside global bond markets Friday, piercing mid-week resistance in the process. The first important resistance to watch is 141.48, the May 2 high. A break of this level would be viewed as an early bullish signal. A return lower would signal scope for an extension towards 136.57, a Fibonacci projection.

USDCAD TECHS: Slips Sharply on USD Downdraft

- RES 4: 1.4111 Apr 10

- RES 3: 1.4019 38.2% retracement of the Feb 3 - Jun 16 bear leg

- RES 2: 1.3920 High May 21

- RES 1: 1.3879 High Aug 1

- PRICE: 1.3794 @ 17:42 BST Aug 1

- SUP 1: 1.3716/3557 20-day EMA / Low Jul 03

- SUP 2: 1.3540 Low Jun 16 and the bear trigger

- SUP 3: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

- SUP 4: 1.3473 Low Oct 2 2024

A short-term bullish corrective phase in USDCAD remains in play despite sharp weakness Friday. On the recent run higher, price traded through the 50-day EMA at 1.3739 and this has been followed by a break of resistance at 1.3798, the Jun 23 high. Clearance of 1.3798 represents an important short-term bullish development, signalling scope for a stronger recovery. Sights are on 1.3920 next, the May 21 high. On the downside, initial firm support to watch lies at 1.3716, the 20-day EMA.