EM ASIA CREDIT: Meituan: Delivery companies may get regulation

(MEITUA, Baa1/A-/BBB+)

"*CHINA SEEKS TO REGULATE FOOD DELIVERY PLATFORM SERVICES: CCTV" - BBG

"*CHINA'S DRAFT RULES TO REGULATE PLATFORM FEES, PROMOTIONS: CCTV" - BBG

We have seen recently the China State Administration for Market Regulation ask the main food delivery companies, including Meituan and JD.com, to compete rationally. The State may now be moving to a more regulated arrangement, overall could be positive for margins if the price war abated. Positive for spreads.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

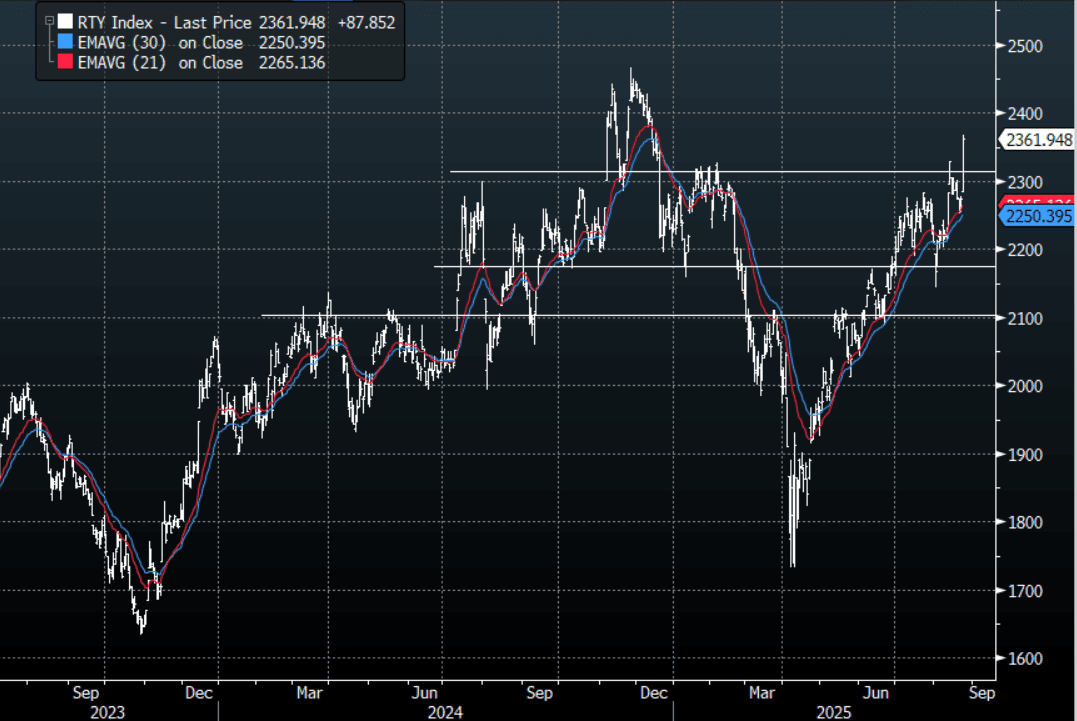

US STOCKS: Russell Explodes Through Resistance Just Above 2300

The Russell 2000 Friday night range was 2285.178 - 2366.598 closing +3.86%. The Russell 2000 has burst higher breaking back above the stubborn resistance just above 2300. I have subsequently read some varying interpretations of Powell's speech with some questioning if it really was that dovish ? So it will be interesting to watch the price action the first couple of days of this week to see if the Friday move can be firstly maintained and then potentially built on. What is clear is the huge shorts held by hedge funds in the Russell would be very uncomfortable with how things played out.

- Bloomberg - “Russell 2000 Surges to This Year’s High on Rate-Cut Prospects: Jerome Powell’s words are music to small-cap investors’ ears as rate cuts would bring huge relief to the Russell 2000, which houses a lot of struggling borrowers.”

- RenMac on X: “This is about September. If you get solid data, you’ll get a hawkish cut in September. If you get bad data, you’ll get a dovish cut. That’s how to think about this. Through the lens of an insurance cut being green lit in September. Importantly, Powell is accepting the Waller framing of the world. We had a shadow chair already. Time to give him the job.”

- Daily Chartbook on X: "EPS expectations for small caps are already extremely bullish, with earnings expected to grow by more than 80% over the next two years. Should interest rate relief be delayed, small caps will likely underperform." -@Daniel_VonAhlen @andrea_cicione @TS_Lombard.

Fig 1: Russell 2000 Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSTRALIA: RBA Minutes And July CPI This Week

In a light week, the focus will be on Wednesday’s July CPI data and Tuesday’s publication of the August RBA minutes. The Board cut rates 25bp this month. They will likely be monitored for further details on its concerns regarding lacklustre productivity growth, its view on the labour market and any discussion of the risks around its inflation outlook. The vote to ease was unanimous.

- July headline inflation is forecast to rise back to 2.3% y/y after falling to 1.9%. This would be the highest since April. The series continues to be impacted in both directions by state and federal electricity rebates. The trimmed mean moderated to 2.1% in June. The July data won’t include updates on most of the services components.

- The RBA’s attention remains on the quarterly data as the monthly CPI is still not complete with the first full release scheduled for the October release on November 26.

- The July Westpac leading index is released on Wednesday. Previous months’ prints are signalling that growth should remain sluggish but return to around trend by year end.

- Components that feed into Q2 GDP released on September 3 will be released with construction work done on Wednesday. It is forecast to rise 1.0% q/q after a flat Q1. Private capex is on Thursday and is expected to rise 0.8% q/q after falling 0.1%.

- Friday sees the RBA’s private credit data for July which is projected to rise 0.6% m/m again.

AUSSIE BONDS: Holding Richer On A Data Light Day

ACGBs (YM +3.0 & XM +4.0) are stronger.

- Cash US tsys are ~1bp cheaper in today's Asia-Pac session after Friday's strong rally.

- Cash ACGBs are 3bps richer with the AU-US 10-year yield differential at +1bp.

- The bills strip has bull-flattened, with pricing flat to +4.

- RBA-dated OIS pricing is slightly softer across meetings today. A 25bp rate cut in September is given a 29% probability, with a cumulative 36bps of easing priced by year-end (based on an effective cash rate of 3.59%).

- Today, the local calendar will be empty, ahead of the RBA Minutes on Tuesday.

- This week, the AOFM plans to sell A$1200mn of the 2.75% 21 June 2035 bond on Wednesday and A$1000mn of the 2.75% 21 November 2028 bond on Friday.