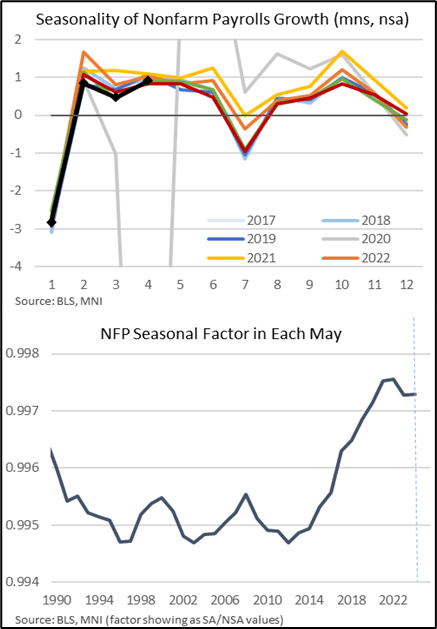

US OUTLOOK/OPINION: May Seasonality Could Test "Low Firing, Low Hiring" Market

Jun-05 19:40

- May is similar to April when it comes to seasonal patterns, typically seeing strong non-seasonally adjusted net increases in employment with 818k in 2024, 883k in 2023 and 830k in 2022.

- As such, it offers a good test of hiring demand at a time of uncertainty, and a better test than would ordinarily be the case in next month’s release for June when net hiring tends to soften (average of 680k in the past three years including 466k in 2024) before outright declines in July.

- This seasonality didn’t appear to materially test the current “low firing, low hiring” nature of the labor market back in April, which was close to the initial unveiling of reciprocal tariffs, but could be a larger factor with this month’s release.

- Seasonal factors for May have been increasingly favorable in recent years but it’s not a new phenomenon, with the most favorable (trimming the NSA level of payrolls by the least amount) coming in 2022.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Near Late Highs, Curves Off Highs As Bonds Gain Ahead Wednesday FOMC

May-06 19:38

- Treasuries look to finish near late Tuesday session highs, early curve steepening consolidating as 30Y Bonds pulled higher late. Main focus on Wednesday's FOMC policy annc.

- Steady rate and no meaningful changes in the Statement expected, though any signal that the Fed is looking seriously at “soft” survey data to assess the outlook could be significant.

- Final March trade data confirmed a new record (-$140.5B nominal) deficit and the largest on a relative basis since 2005/06 in the imbalances ahead of the Great Financial Crisis. However, pharmaceutical tariff front-running and continued heavy imports of gold are greatly clouding interpretation of underlying trends.

- Early short end support after latest tariff-related headlines: EU to target E100B of US goods if trade negotiations fail. Meanwhile, decent $42B 10Y Note auction stops 1.3bp through: drawing 4.342% high yield vs. 4.355% WI.

- Tsy Jun'25 10Y futures currently +7.5 at 111-09.5 vs. 111-11.5 high, initial technical resistance well above at 112-01.5 (High May 2). For bulls, price needs to trade above key short-term resistance at 112-20+, the May 1 high, to reinstate a bullish theme.

- Cross asset roundup: Bbg US$ index near late lows (BBDXY -3.49 at 1217.28), Gold plowing higher late (3416.95 - not for off April 22 all-time high of 3494.52), Crude rebounding (WTI +1.87 at 59.0.

AUDUSD TECHS: Bulls Remain In The Driver’s Seat

May-06 19:30

- RES 4: 0.5682 High Nov 12 ‘24

- RES 3: 0.6550 61.8% retracement of the Sep 30 ‘24 - Apr 9 bear leg

- RES 2: 0.6528 High Nov 29 ‘24

- RES 1: 0.6494 High May 05

- PRICE: 0.6486 @ 17:02 BST May 6

- SUP 1: 0.6366/6327 20- and 50-day EMA values

- SUP 2: 0.6275 Low Apr 14

- SUP 3: 0.6181 Low Apr 11

- SUP 4: 0.6116 Low Apr 10

AUDUSD traded higher Monday and a bullish theme remains intact. The recent breach of 0.6450, the Apr 29 high, marks the end of the recent pause in the bull cycle and confirms a resumption of the uptrend. Note that moving average studies are in a bull-mode position, highlighting an uptrend. Sights are on 0.6528, the Nov 29 ‘24 high. Initial key support to monitor is 0.6327, the 50-day EMA.

US OUTLOOK/OPINION: Macro Since Last FOMC: Inflation - Expectations Surge [2/2]

May-06 19:14

- Soft data point to significant inflationary pressures ahead, with businesses reporting sharp increases in prices paid and consumer inflation expectations soaring.

- On the business side, the ISM manufacturing prices paid index wasn’t quite as high as expected in April but at 69.8 it has still climbed since a recent low of 50.3 (coinciding with the US presidential election) to its highest since Jun 2022.

- This is echoed by the final April manufacturing PMI from S&P Global which found that “tariffs reportedly led to steep increases in both input costs and selling prices” and the highest output charge inflation in over two years. The latter is clearly important from cost passthrough point.

- Previous Fed Beige Book entries have noted difficulty passing price increases onto customers although the latest on April 23 still expects costs to be passed on: “Most businesses expected to pass through additional costs to customers. However, there were reports about margin compression amid increased costs, as demand remained tepid in some sectors, especially for consumer-facing firms.” Directly with respect to tariffs and US trade policy: “Many firms have already received notices from suppliers that costs would be increasing. Firms reported adding tariff surcharges or shortening pricing horizons to account for uncertain trade policy.”

- On the consumer side, the U.Mich survey has seen both short- and long-run inflation expectations surge to multi-decade highs including its 1Y figure at the highest since 1981. Further increases look possible judging by a useful chart U.Mich provided (currently found here) with responses throughout the month demonstrating strong increases after Apr 2 tariff announcements before some pulling back after the Apr 9 reciprocal ‘pause’.