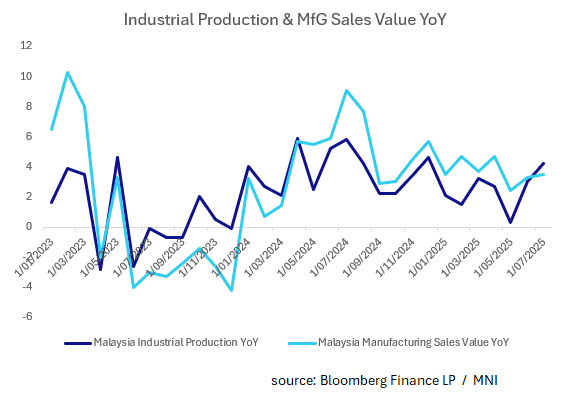

MALAYSIA: Manufacturing Rebounds in July

- Industrial production YoY for July exceeded expectations in today's release.

- Up +4.2%, it beat market estimates of +2.8% and was ahead of the June (revised) result of 2.9%.

- It was the first time the mining sector expanded since March, with a +4.3% gain (from 0.00% in June) and manufacturing was up to +4.4% from 3.6% in June.

- This was the quickest monthly expansion since late 2024.

- Manufacturing sales value has been incredibly stable and this month's result of +3.5%, was marginally up on last month's +3.3%.

- This is welcome news for the BNM that meets next in November who described their rate cut in July as 'pre-cautionary', and could see no further action from monetary policy this year.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

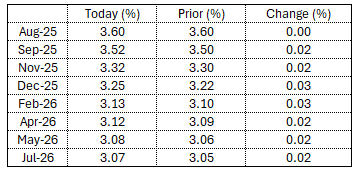

STIR: RBA Dated OIS Slightly Firmer Ahead Of Today’s RBA Decision

At the time of writing, RBA-dated OIS pricing is slightly firmer on the day across meetings ahead of today’s RBA Policy Decision.

- A 25bp rate cut this week is given a 96% probability, with a cumulative 59bps of easing priced by year-end (based on an effective cash rate of 3.84%).

Figure 1: RBA-Dated OIS – Current Vs. Yesterday

Source: Bloomberg Finance LP / MNI

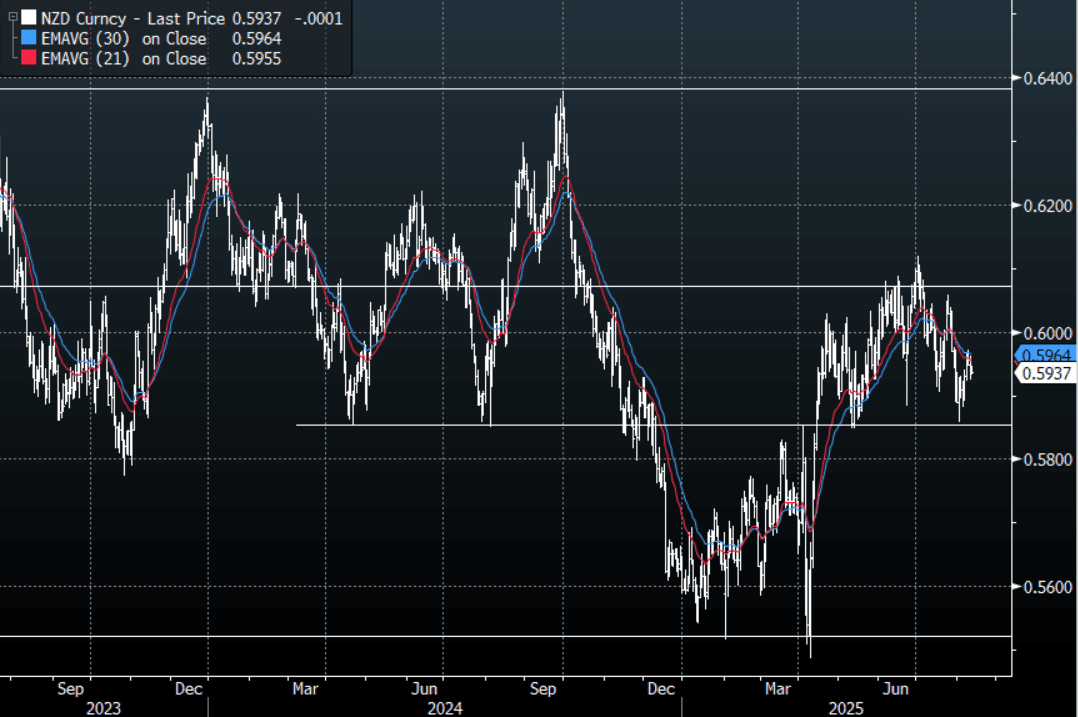

NZD: Asia Wrap - NZD/USD Consolidating On A 0.59 Handle, Awaits US CPI

The NZD/USD had a range of 0.5933 - 0.5946 in the Asia-Pac session, going into the London open trading around 0.5935, -0.05%. Risk has traded a little higher this morning, E-minis +0.10%, NQU5 +0.10%. NZD/USD bounced nicely off its 0.5850 support last week but depending on your view I would suspect sellers could return on any bounce back toward 0.6000/0.6050. For the moment firmly back in the 0.5850-0.6100 range looking for a catalyst to break and give clearer direction. The US CPI tonight might hopefully clear the picture a little.

- (Bloomberg) -- Australia’s dollar is expected to lag behind its New Zealand counterpart as their economies and central bank policies diverge, according to a Barclays note. Dovish risks are higher for the RBA as Australia’s economy slows, a currency strategist at Barclays writes in a note. On the other hand New Zealand’s growth is gaining momentum and inflation has rebounded. Aussie is also vulnerable to slower global growth and weakness in the Chinese economy.

- (Bloomberg) - Shipments from China, the US’s second-largest source of imports, started drying up noticeably in the lead-up to the Aug. 11 deadline to avoid re-imposing massive reciprocal tariffs. The drop-off may add to investors’ nervousness over whether equities can extend this year’s surge in the face of President Trump’s trade war.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5825(NZD300m Aug 14). - BBG

- CFTC Data shows Asset Managers have cut their longs completely and started to rebuild a short in the NZD -1811(Last +3903), the Leveraged community added to their shorts slightly -6778(Last -6250).

- AUD/NZD range for the session has been 1.0964 - 1.0983, currently trading 1.0980. The Cross continues to trade sideways after stalling towards the 1.1000 area once more. The range looks to be 1.0850-1.1000 for now.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

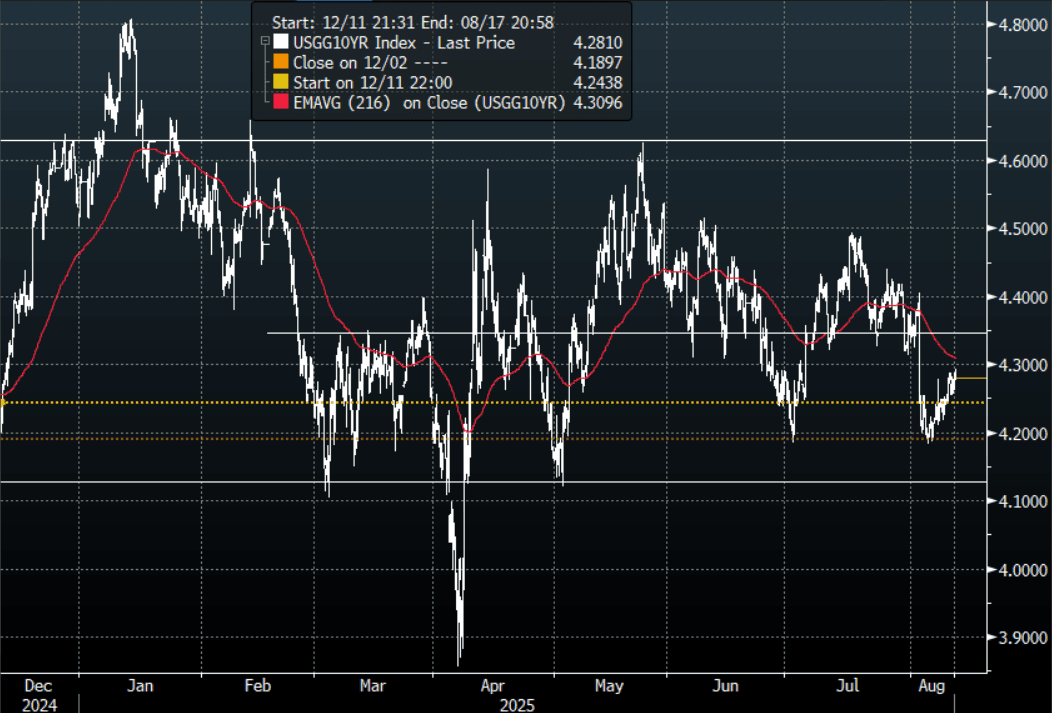

US TSYS: Asia Wrap - Market Eyes CPI, Very Quiet Asian Session

The TYU5 range has been 111-23 to 111-26 during the Asia-Pacific session. It last changed hands at 111-25, down 0-03+ from the previous close. All eyes on the US CPI tonight to confirm if there any signs of inflation taking hold.

- The US 2-year yield is trading around 3.768%.

- The US 10-year yield is trading around 4.283%.

- The 10-year yield had a powerful move lower in reaction to the NFP data, breaking below its 4.30% pivot within the wider range 4.10% - 4.65%. This now turns momentum lower in yields and you could expect buyers of treasuries on bounces back towards 4.30/35% now looking to initially test the 4.10% area.

- MNI US CPI Preview: High Early Bar To September Fed Hold. The CPI report for July is released on Tuesday Aug 12, at 0830ET. Consensus sees core CPI inflation at a seasonally adjusted 0.3% M/M in June and unrounded analyst estimates broadly echo this with a median 0.32% M/M. It would mark a further acceleration from 0.23% M/M in June and 0.13% M/M in May for its fastest pace since January, with the latest firming seen coming from core goods inflation doubling to 0.4% M/M.

- Truflation on X: “July BLS CPI FORECAST: 2.8% YoY. Tariffs are biting, the labor market is cooling, and consumers are wobbling, pointing to slower growth. Could this signal upside risks to inflation? July highlights, goods prices accelerating as tariffs pass through; services cooling (but still supported by wage growth). Biggest upward contributors: Education +0.7% MoM (+2.9% YoY) · Utilities +0.6% (+4.6%) · Health +0.5% (+3.0%) · Alcohol & Tobacco +0.6% (+3.1%). Biggest downward contributors: Food −0.6% MoM (+2.7% YoY) · Housing −0.5% (+0.8% YoY)

- Data/Events: NFIB Small Business Optimism, CPI, Federal Budget Balance

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P