EU CONSUMER CYCLICALS: Loomis: 2Q results

(LOOMBS 29s; NR/BBB)

"*LOOMIS 2Q NET SALES SEK7.41B, EST. SEK7.44B

*LOOMIS 2Q ADJ. EBIT SEK882M, EST. SEK818.8M" -bbg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURJPY TECHS: Trend Needle Points North

- RES 4: 171.09 High Jul 23 ‘24

- RES 3: 170.47 76.4% Fibonacci retracement for Jul - Aug ‘24 downleg

- RES 2: 169.91 1.236 proj of the Feb 28 - Mar 18 - Apr 7 price swing

- RES 1: 169.71 High Jun 23

- PRICE: 168.64 @ 07:27 BST Jun 25

- SUP 1: 167.46 Low Jun 23

- SUP 2: 166.12 20-day EMA

- SUP 3: 164.95 Low Jun 13

- SUP 4: 164.40 50-day EMA

The trend set-up in EURJPY is unchanged, it remains bullish and Monday’s strong start to this week’s session, reinforces a bullish theme. The cross has recently cleared 166.69, the Oct 31 ‘24 high. Scope is seen for a climb towards 170.47, a key Fibonacci retracement point. Note that the cross is overbought, a pullback would unwind this condition. Support to watch lies at 166.12, the 20-day EMA.

BUNDS: Finding a bid on the Cash Open

- Not much Change in Bund post cash open, there's a small bid on the Cash Open, but the contract is well within the Resistance and support.

- These stands at 131.28 (resistance) and 131.05 (the 2.60% Yield level).

- On the Margin the US Tnotes is in Focus, as the 10yr Yield keeps testing the 4.30% level, printed a 4.2886% low for now.

- For outright futures, the next outright resistance is at 111.25, and in terms of Yield, 111.28+ would equate to 4.25%.

- There's no Tier 1 data for the session, the Spanish GDP is final reading, and on the other side of the Pond, US NHS (New Home Sales) is unlikely to move the needle.

- SUPPLY: Italy €3bn 2027 (equates to 26.3k short 2yr BTP) could somewhat weigh, the 2031 linker won't impact BTP. UK £3.25bn 2040 (equates to 35.8k Gilt) will weigh, US Sells $70bn of 5yr Notes and $28bn of 2yr FRN reopening, the FRN won't impact Treasuries.

- SPEAKERS: BoE Lombardelli, US Goolsbee, Powell.

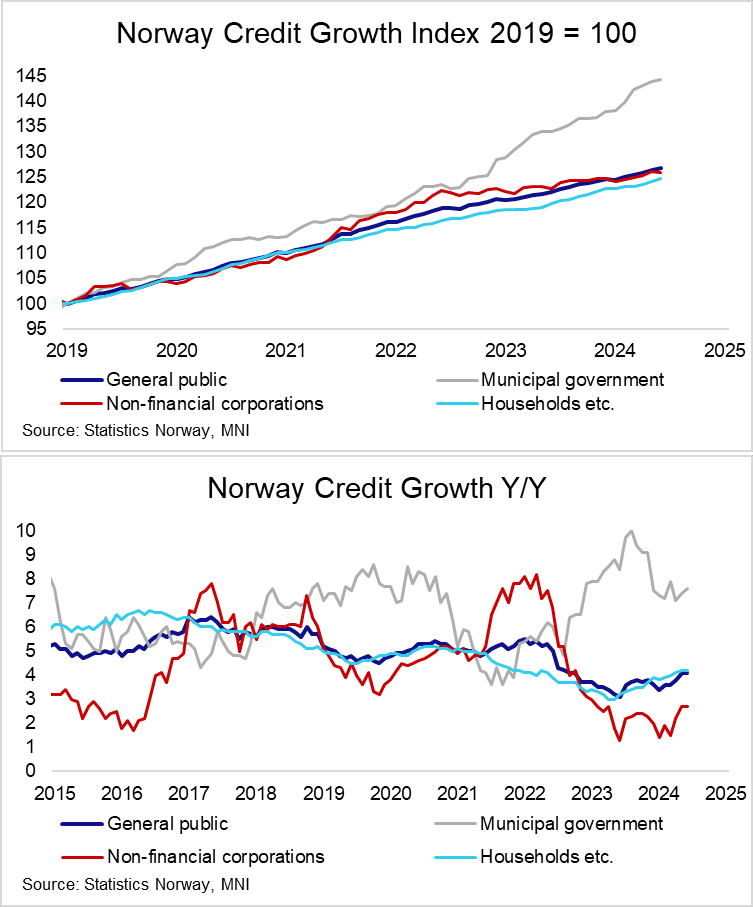

NORWAY: Credit Growth Steady In May; Focus On Labour Market Data

Norwegian credit growth was steady at 4.1% Y/Y in May, with household lending growth unchanged at 4.2% and non-financial corporate lending growth at 2.7% Y/Y. Municipal government credit growth accelerated to 7.6% Y/Y (vs 7.4% prior), though this only represents 10% of the total stock of loans.

- Norges Bank projected household credit growth at 4.2% in 2025 and 4.3% in 2026 in the June MPR.

- In the report, Norges Bank noted that “household debt growth has increased since spring 2024. Higher house prices and lower interest rates suggest higher debt growth ahead, while a low supply of new homes has a dampening effect. A rise in housing investment further out will pull up credit growth. Overall, a gradual increase in household debt growth is expected. Household income growth is expected to outpace credit growth somewhat, resulting in a slight decline in the debt-to-income ratio through the projection period. A lower policy rate will reduce the household interest burden in the coming years.”

- A reminder that in December 2024, the Government loosened regulations on household mortgage lending, raising the maximum LTV for mortgages from 85% to 90%.

- This week’s Norwegian calendar is headlined by labour market data (LFS tomorrow and registered unemployment on Friday). While an easing in inflationary pressures was the main reason Norges Bank opted to cut rates last Thursday, we think considerable attention was also given to the slight rise in unemployment rates since March. Tracking these metrics will be important to determine the likelihood of the next cut in September.