LNG: LNG Cargoes Divert Course Towards Europe

Two US LNG cargoes on tankers Bushu Maru and Grace Dahlia have diverted from a course towards Asia and are now heading to Europe, according to Bloomberg ship tracking.

- European demand is supported by the reduction in Russian pipeline gas supplies while demand in Asia has reduced due to the higher spot prices.

- China is trying to resell LNG cargoes after the recent surge in global prices and weak domestic demand according to importer ENN Group. Several firms are offering cargoes for February and March.

- NW European received 21 LNG cargo arrivals in Jan. 1-9 with another 18 tankers currently scheduled to arrive this month, according to Bloomberg ship tracking data. A total of 63 vessels arrived during December and 80 in January 2024.

- However, the US LNG netbacks favour supply to Asia over Europe in February, according to BNEF. Profitability of US LNG exports to Asia is $9.61/mmbtu and to Europe is $8.98/mmbtu.

- TTF FEB 25 down 2.9% at 43.7€/MWh

- JKM Feb 25 down 1.8% at 14$/mmbtu

- JKM-TTF Feb 25 up 0.2$/mmbtu at 0.81$/mmbtu

- US Natgas FEB 25 up 3.5% at 3.83$/mmbtu

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

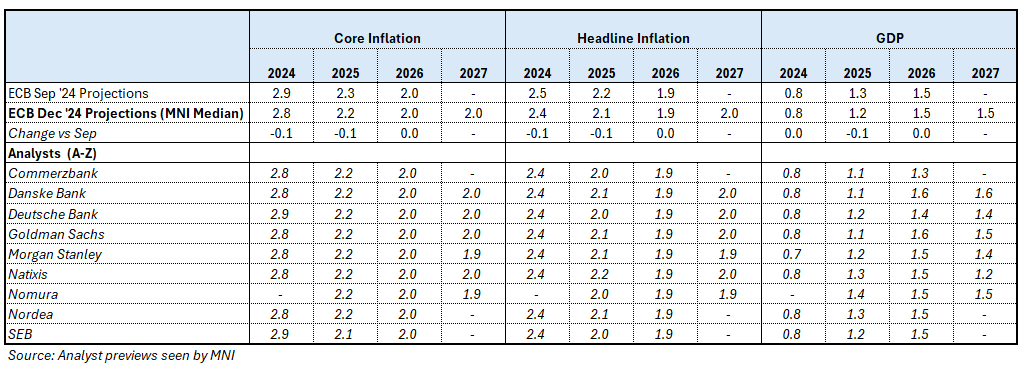

ECB: Analysts Expect Small Downward Revisions To Headline, Core and GDP F'casts

Analysts expect the ECB to make small downward revisions to its inflation and GDP projections in the December projection round, which has been compiled by Eurosystem (i.e. national central bank) staff. Note that 2027 projections will also be presented for the first time.

- Based on the previews MNI has seen, the median expectation for 2025 core inflation is 2.2% (vs 2.3% in the September projection round). The core inflation projection is expected to be 2.0% in 2026 and 2027. Morgan Stanley and Nomura see the 2027 core inflation projection at 1.9%.

- The 2025 headline inflation projection is expected at 2.1% (vs 2.2% in September).

- Although crude oil futures were around 6% lower around the December projection cut-off date compared to September, analysts note that this is offset by higher gas/electricity prices and a weaker Euro.

- Q3 GDP exceeded ECB forecasts at 0.4% Q/Q (vs 0.2% projected), but this was in part due to temporary effects from the Paris Olympics. Weak momentum into Q4, alongside heightened uncertainty from US trade policy and French/German politics means analysts expect a downward revision to the ECB’s 2025 real GDP forecast to 1.2% (vs 1.3% in September). 2027 real GDP projection expectations range from 1.2% (Natixis) to 1.6% (Danske).

- See the table below for a full summary. MNI’s ECB preview is here.

JPY: USD/JPY Whiplash on BoJ Report

The BoJ are said to see little cost to waiting for the next rate hike, according to Bloomberg sources. They write that officials see less risk of a weaker JPY driving up inflation, and see the next hike as a matter of time.

USD/JPY rallying hard off lows and now higher than pre-headline levels (151.02 low, now just shy of overnight highs) - mixed headlines there from the BoJ story - this read hawkish: "SOME BOJ OFFICIALS NOT AGAINST RATE HIKE IN DEC", however the follow-up headline provided a solid counterargument: "BOJ SAID TO SEE LITTLE COST TO WAITING FOR NEXT HIKE".

- Comfortably the best volumes of the day on that report: 15,000 contracts traded inside 60 seconds - that's a cash equivalent of $1.3bln.

SONIA: Outright put buyer

SFIH5 95.30p, bought for 1.25 in 5k.