AUSSIE BONDS: Little Changed On A Subdued Data-Light Session

ACGBs (YM -0.5 & XM -1.0) are little changed on a data-light session.

- Cash US tsys are flat to 1bp cheaper, with a steepening bias, in today's Asia-Pac session after yesterday's twist-flattener.

- Cash ACGBs are 1bp cheaper with the AU-US 10-year yield differential at +2bps.

- The latest ACGB Mar-36 auction saw strong demand, with the weighted average yield coming in 0.21bps through prevailing mid-yields, according to Yieldbroker, continuing the trend of firm pricing at recent ACGB auctions. However, the cover ratio collapsed to 3.3111x from 4.45x.A$1000mn of the 3.00% 21 November 2033 bond is planned for Friday.

- The bills strip is weaker, with pricing -1 to -3.

- RBA-dated OIS pricing is little changed across meetings today. A 25bp rate cut in August is given a 100% probability, with a cumulative 63bps of easing priced by year-end (based on an effective cash rate of 3.84%).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

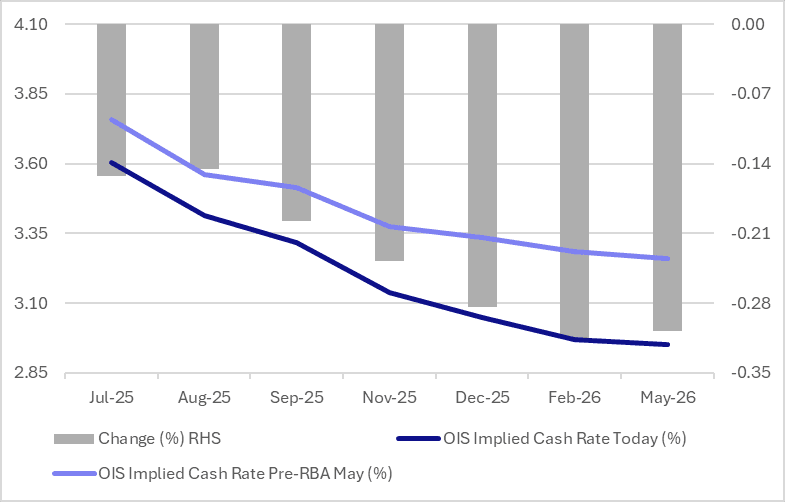

STIR: RBA Dated OIS Priced For A 25bp Cut Tomorrow

At the time of writing, RBA-dated OIS pricing is slightly softer on the day across meetings ahead of tomorrow’s RBA Policy Decision.

- A 25bp rate cut this week is given a 93% probability, with a cumulative 78bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- Notably, today’s moves leave meetings pricing 15-32bps softer than levels before the May 20 RBA Meeting.

Figure 1: RBA-Dated OIS – Current Vs. Pre-RBA (May)

Source: Bloomberg Finance LP / MNI

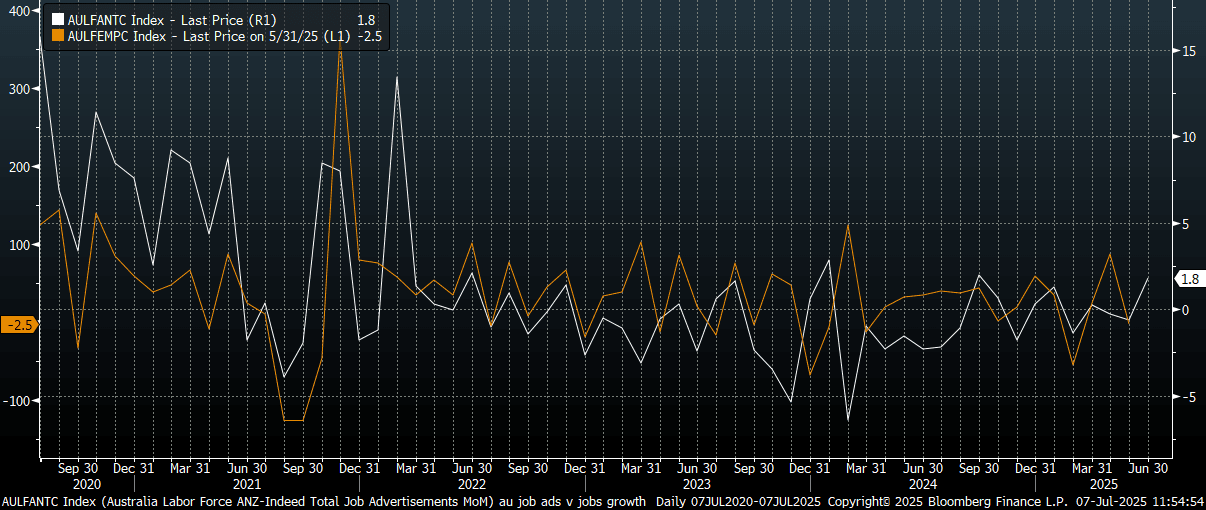

AUSTRALIA DATA: ANZ Job Ads Rise In June, Pointing To Resilient Labor Market

The ANZ June job ads print was +1.8%m/m, after a revised fall of 0.6% in May (originally reported as a -1.2% decline). In y/y terms, jobs ads are -0.4%. At the start of the year we were at -13.7%. This was the best m/m increase for the index since Sep last year. It points to continued resilience in terms of labor market conditions. The chart below plots the ANZ job ads m/m change versus monthly employment growth in Australia.

- The RBA meets tomorrow, with a 25bps cut widely expected. The central bank is likely to continue to emphasize the tight labor market, but this is unlikely to be enough to offset greater comfort around inflation trends, which should see them ease further.

Fig 1: ANZ Job Ads Post Solid Rise in June

Source: Bloomberg Finance L.P/ANZ/MNI

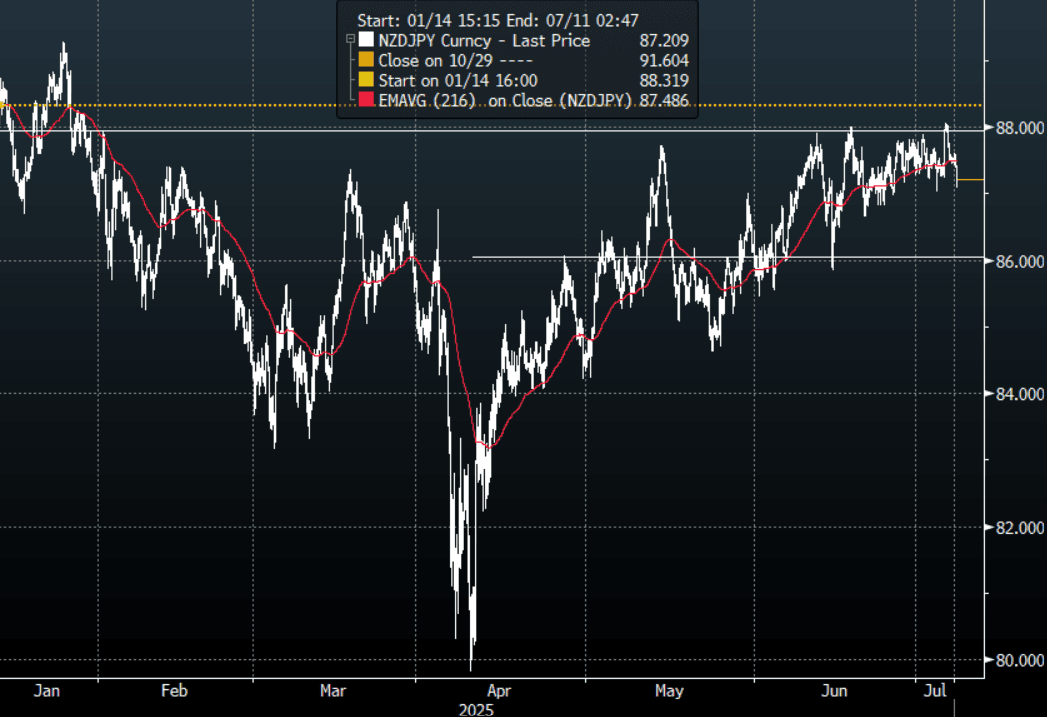

FOREX: JPY Crosses - JPY Underperformance Stalls As Risk Eyes Tariff Deadline

This morning has seen US futures open a little higher but still off the highs from last week, ESU5 -0.40%, NQU5 -0.50%. This week the tariff deadline will be closely watched by a market that looks to have a lot of positives already baked in the price. The JPY is bouncing back in the crosses as risk appetite dwindles as the deadline approaches.

- EUR/JPY - Friday night range 169.85 - 170.33, Asia is trading around 170.15. The pair failed to build any upward momentum through 170.00 on Friday. With risk stalling and the JPY beginning to outperform we could see some reversion back towards the 168.50 area.

- GBP/JPY - Friday night 196.91 - 197.41, Asia trades around 197.00. The pair bounced strongly off its support around 196.00, with risk stalling the market will be watching to see if this demand is still around if we dip back down there.

- NZD/JPY - Friday night range 87.45 - 87.70, Asia is currently dealing 87.20. NZD/JPY had a false break above 88.00 and has turned quickly back lower. With risk stalling the danger is this pair drifts back to test its support around 86.00.

- CNH/JPY - Friday night range 20.1322 - 20.1799 Asia is currently trading around 20.1625. A big reversal from the 20.50/20.60 resistance area. In the middle of its recent range awaiting clearer direction with a bias to sell rallies.

Fig 1 : NZD/JPY Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P