JGBS: Little Changed As Market Digests Yesterday's BoJ MPM Outcome

At the Tokyo lunch break, JGB futures are stronger but off bests, +12 compared to the settlement levels.

- Earlier data showed mixed June labor market conditions. The unemployment rate was steady at 2.5%. This was in line with market forecasts. The unemployment rate has been steady at 2.5% since March of this year. This is just up from cycle lows of 2.4%. However, the job to applicant ratio rose fell to 1.22 from 1.24 prior, which was also below the 1.25 consensus expectation. This is the lowest job-to-applicant ratio since 2022.

- Yesterday Governor Ueda stressed that underlying inflation remains below target and emphasised the need for more data to assess the full impact of 15% U.S. tariffs on Japan’s economy. Although some speculate an October hike is possible post-political uncertainty, the BoJ is likely to wait until early 2026, seeking clearer evidence of wage-driven inflation and minimal tariff disruption. See full MNI BoJ Review here

- Cash US tsys are slightly mixed, with a steepening bias, in today’s Asia-Pac session.

- Cash JGBs are slightly richer, led by the 5-year. The benchmark 10-year yield is 0.8bp lower at 1.549% versus the cycle high of 1.616%.

- The swaps curve is little changed.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Cheaper, Narrow Ranges, Heavy US Calendar Today & Tomorrow

ACGBs (YM -3.0 & XM -3.0) are modestly weaker on another subdued day of trading.

- Australian retail sales rose a modest 0.2%m/m in May, after a revised flat outcome in April (originally reported as a -0.1% dip). The market consensus for the May outcome was a +0.5% rise. Other data showed May building approvals up 3.2%m/m, which was slightly below the 4.0% forecast. The April fall was revised to -4.1%m/m.

- Building approvals rose 3.2% m/m (estimate +4.0%) in May versus a revised -4.1% in April.

- Cash US tsys are little changed in today’s Asia-Pac session after yesterday’s twist-flattener. Wednesday's US data focus is on MBA Mortgage Applications at 0700ET, Challenger Jobs at 0730ET followed by ADP Employment Change at 0815ET. No Fed scheduled Fed speakers. Thursday is a heavy data day with NFP added due to Independence Day holiday closure on Friday.

- Cash ACGBs are 2-3bps cheaper with the AU-US 10-year yield differential at -11bps.

- The bills strip has bear-flattened, with pricing -1 to -4.

- RBA-dated OIS pricing is slightly firmer across meetings today. A 25bp rate cut in July is given a 95% probability, with a cumulative 82bps of easing priced by year-end (based on an effective cash rate of 3.84%).

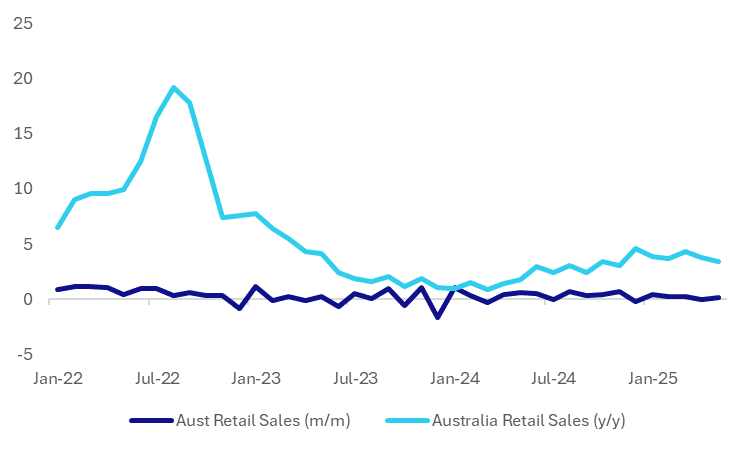

AUSTRALIA DATA: Retail Momentum Softens Further In May, Despite Clothing Bounce

Australian retail sales rose a modest 0.2%m/m in May, after a revised flat outcome in April (originally reported as a -0.1% dip). The market consensus for the May outcome was a +0.5% rise. Other data showed May building approvals up 3.2%m/m, which was slightly below the 4.0% forecast. The April fall was revised to -4.1%m/m.

- By sub category we had strong rebounds in both apparel retail sales and department store spending. Both categories were up close to 3%m/m, but this follows similar falls in April.

- The ABS noted: "‘Clothing retailers and department stores were boosted by people buying winter clothes, having held off on those purchases with the warmer-than-usual weather last month,’ Mr Ewing said."

- Otherwise, spending trends were either flat or down a touch. Notably food retailing fell by 0.4%m/m, after declining 0.2% in April.

- The y/y pace eased to 3.4% from 3.8% in April, see the chart below. The general trend in spending momentum is too moderate after last year's fiscal impulse for households helped drive a brief strengthening.

- The RBA meets next week, and the market has a 25bps cut priced in. Today's data is likely to reinforce easing expectations at the margin.

- Note this is the second last retail sales release, with the release to be replaced by the household spending series (the next update for this print is on Friday).

Fig 1: Australia Retail Sales Momentum Eases Further

Source: Bloomberg Finance L.P./MNI

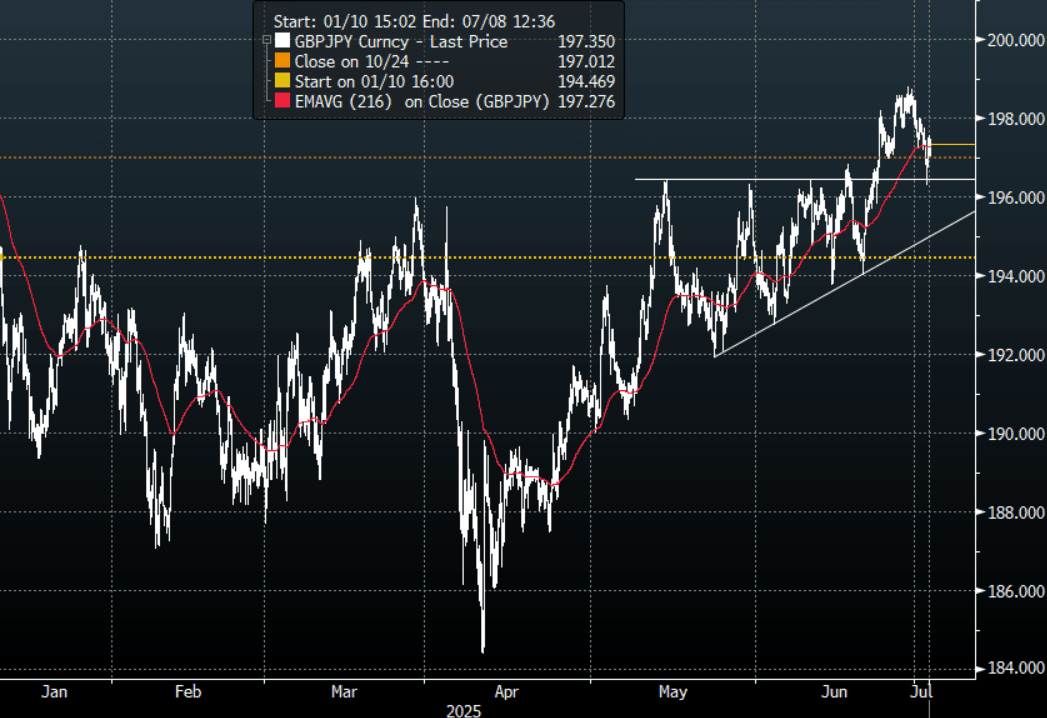

FOREX: JPY Crosses - The JPY Still Struggles In The Crosses

US stocks outperformance is now widening out to the broader market and global risk sentiment remains very positive. The JPY underperformance against the GBP and potentially the EUR seems to be stalling for now, it continues to perform best against the CNH.

- EUR/JPY - Overnight range 168.46 - 169.52, Asia is trading around 169.45. Decent demand was seen around 168.50 overnight as the pair consolidated some of its recent gains. First support is back towards the 167.50 area, a break back above 170.00 is needed to reengage the upward momentum.

- GBP/JPY - Overnight range 196.29 - 197.55, Asia trades around 197.30. Good demand seen towards the support around 196.00, the pair could look to consolidate as we look toward NFP Thursday. The pair remains in an uptrend and dips should be supported for now.

- NZD/JPY - Overnight range 87.22 - 87.67, Asia is currently dealing 87.55. NZD/JPY continues to trade sideways as it consolidates, a sustained break above 88.00 is needed for the market to turn its focus back to the 90.00 area. The longer this cross stalls up here the greater the chance of it turning back towards the 96.00 area.

- CNH/JPY - Overnight range 19.9368 - 20.0750 Asia is currently trading around 20.0475. A big reversal from the 20.50/20.60 resistance area. In the middle of its recent range awaiting clearer direction with a bias to sell rallies.

Fig 1 : GBP/JPY Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P