JGBS: Futures Weaker Overnight, US PCE Higher Than Expected

Jul-31 23:31

In post-Tokyo trade, JGB futures closed weaker, -8 compared to settlement levels, after a modestly weak close for US tsys.

- Both headline and core PCE inflation were stronger than Fed tracking in June, at least going off Fed Chair Powell's comments in yesterday's FOMC press conference, although they don't look too surprising considering an upward surprise in yesterday's Q2 advance release. It continues trend stabilization in core PCE inflation comfortably above the 2% inflation target, most recently at 2.8% Y/Y, whilst market-based services inflation (a component of interest for the more hawkish members) is still at 3.3% Y/Y.

- MNI JAPAN: The governing Liberal Democratic Party (LDP) will hold a General Assembly meeting of lawmakers from both houses of the National Diet on 8 August. This event could prove crucial in determining whether PM Shigeru Ishiba remains in office or faces a formal move to call a snap party leadership election.

- "Bank of Japan Governor Kazuo Ueda kept investors guessing over the timing of his next interest-rate hike with comments that cooled expectations of a near-term move." - BBG

- June Jobless Rate at 2.5% (2.5% est) and Job-To-Applicant Ratio at 1.22 (1.25 est).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Futures Curve Bear-Flattens In Line With US Tsys, Bldg Apps & RS D

Jul-01 23:21

ACGBs (YM -4.0 & XM -1.5) are weaker with a flatter curve following Tuesday’s twist-flattening by US tsys. US yields finished 5bps higher to 1bp lower.

- The JOLTS report for May saw stronger-than-expected job openings. All pointed to broad stabilisation in the labour market rather than showing signs of further moderation.

- Wednesday’s US data focus is on MBA Mortgage Applications at 0700ET, Challenger Jobs at 0730ET followed by ADP Employment Change at 0815ET. No Fed scheduled Fed speakers. Thursday is a heavy data day with NFP added due to Independence Day holiday closure on Friday.

- Cash ACGBs are 2-3bps cheaper with the AU-US 10-year yield differential at -11bps.

- The bills strip is cheaper, with pricing -2 to -4.

- RBA-dated OIS pricing is slightly firmer across meetings today. A 25bp rate cut in July is given a 94% probability, with a cumulative 81bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- Today, the local calendar will see Building Approvals and Retail Sales data.

- The AOFM plans to sell A$1200mn of the 2.75% 21 June 2035 bond today and A$1000mn of the 2.25% 21 May 2028 bond on Friday.

BONDS: Cheaper With US Tsys, Milk Prices Down, Syn Tap Of May-31

Jul-01 23:08

In local morning trade, NZGBs are 2bps cheaper after US tsys finished Tuesday with a twist-flattening, with yields 5bps higher to 1bp lower.

- The JOLTS report for May saw stronger-than-expected job openings. All pointed to broad stabilisation in the labour market rather than showing signs of further moderation.

- Overnight, the whole milk price auction saw a sharp fall. We fell to $3859 from $4084 prior, which was a 5.1% drop between the two auctions (see this link to the GDT website). The whole milk price is off close to 12% from its highs at the start of May.

- Swap rates are 2bps higher.

- RBNZ dated OIS pricing is little changed across meetings. 4bps of easing is priced for July, with a cumulative 33bps by November 2025.

- Today, the local calendar will be empty.

- The NZ Treasury is launching the syndicated tap of the May 2031 nominal bond. Treasury expects to issue at least NZ$4bn and will cap it at NZ$6bn. Issue will be priced July 3 with initial price guidance +21-24 bps over the May 2030 nominal bond. JLM are ANZ Bank, Bank of New Zealand, CBA and Westpac. Given the timing of the launch, the Treasury has cancelled the July 3 bond auction.

COMMODITIES: Gold and Oil Gain Overnight

Jul-01 22:56

- As the President's tax bill passes through senate, the ever present fiscal concerns return to investors and fellow republicans thoughts. House Republicans are pushing back on the bill citing concerns over spending reductions and medicaid cuts and if at least three republicans do not support, the bill's passage through the House may not be assured.

- Fed Chairman Powell "Really Can't Say" If July Too Soon To Seriously Consider Cut. Fed Chair Powell speaking on an ECB forum panel asked if July is too soon to seriously consider a rate cut and he certainly doesn't categorially rule it out, even if it's couched in typical central bank-speak: "Yeah, I really can't say - it's going to depend on the data. And we are going meeting by meeting. I mentioned, you know, how I'm thinking about that, but I wouldn't take any meeting off the table or put it directly on the table, it's going to depend on how the data evolve."

- Powell's comments comes as the May JOLTS report saw stronger job openings than expected and other data points to stabilization of the labour market.

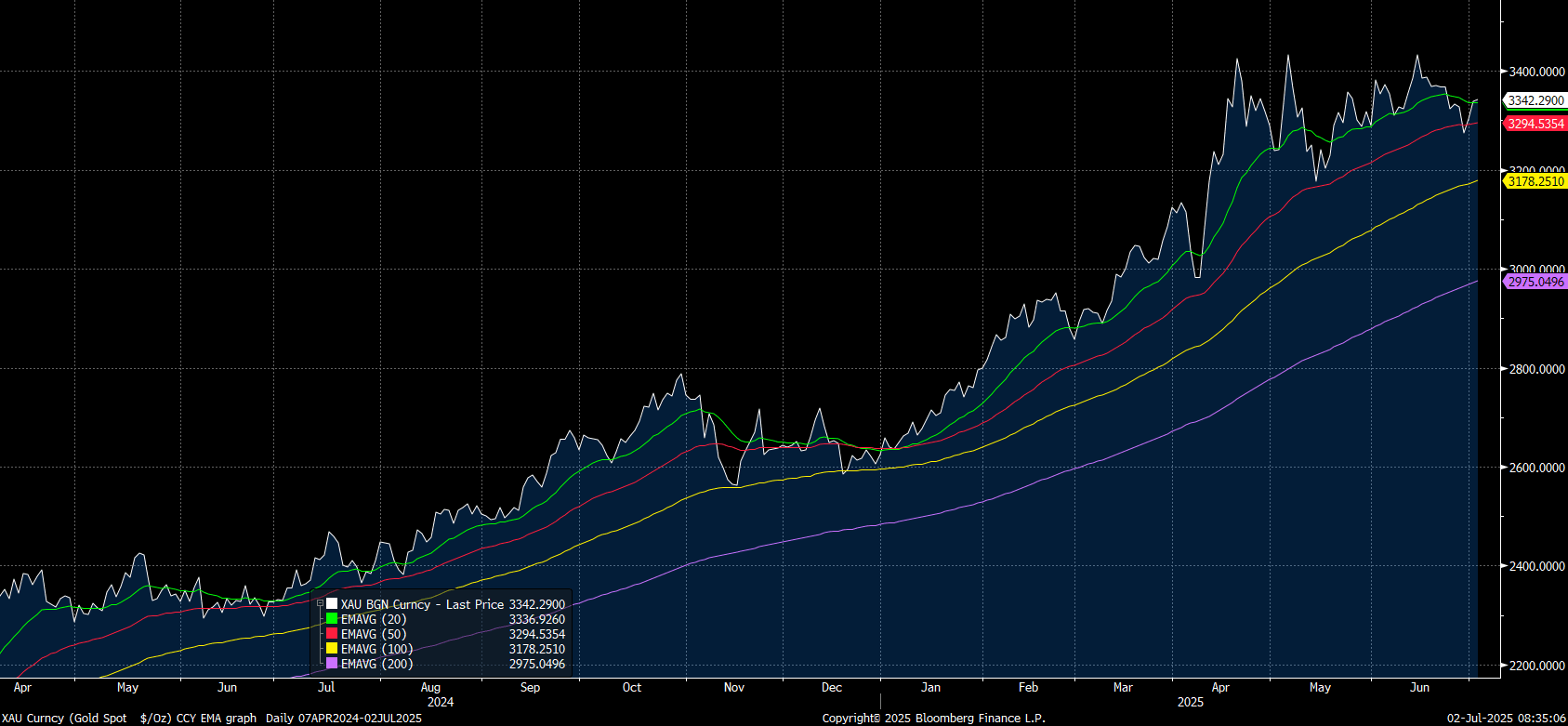

- The fiscal concerns were enough to give GOLD a boost and it finished the US session up +1.08% to a high of US$3,332.33, a bounce of over 3% from Friday's lows, before settling into the close at $3,338.84.

- The rally sees gold back above the 20-day EMA of $3,336.98, having briefly traded below the 50-day EMA on Friday.

Source: Bloomberg Finance LP / MNI

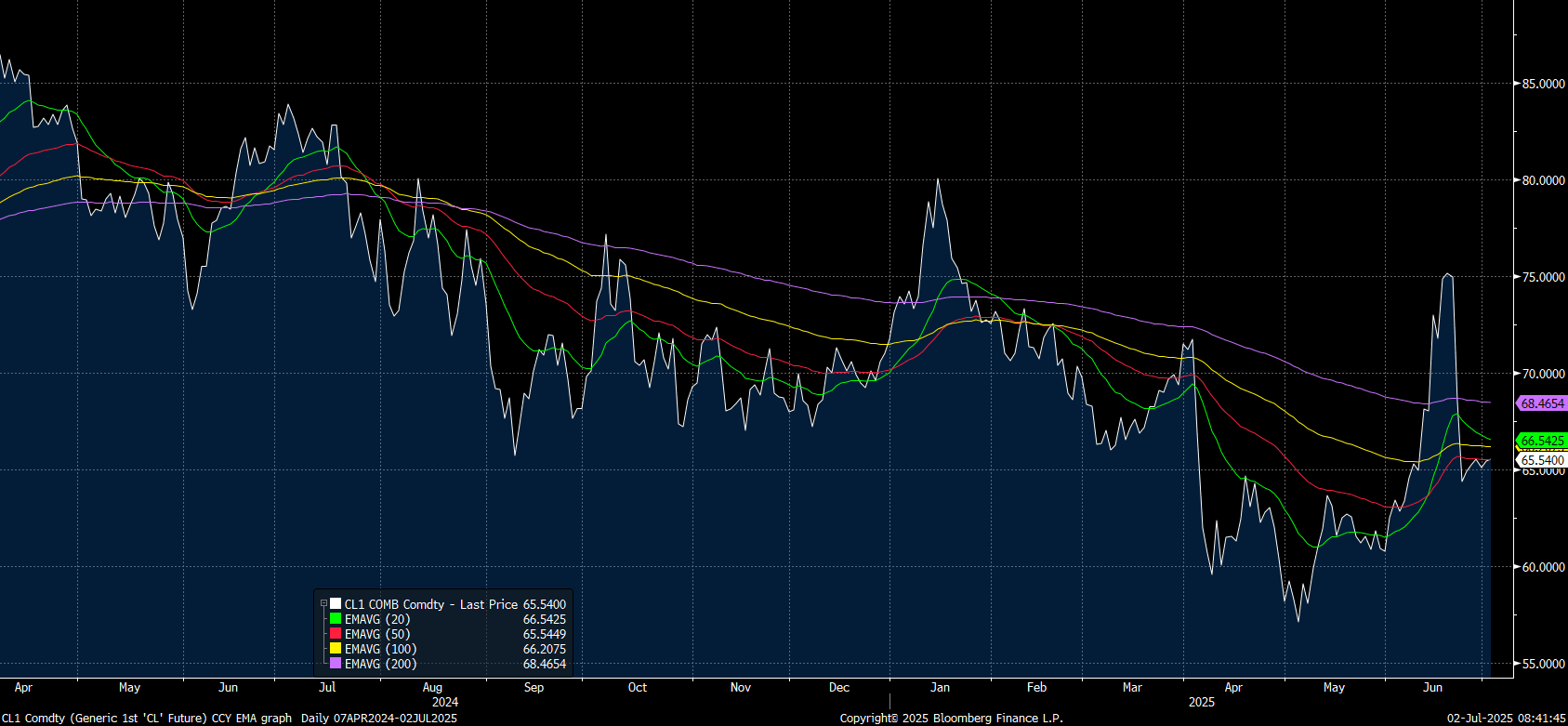

- Oil had a stronger night despite the expectations of a further increase in OPEC+ output in August as the market weighs the potential for stronger than expected demand given the heat experienced across most of Europe and the US.

- WTI finished in the US up at the end of the US session by +0.52% and is opening stronger in the Asia trading day. At US$65.54, WTI is attempting to break the 50-day EMA of $65.54 with the 100-day EMA above at $66.20

Source: Bloomberg Finance LP / MNI

- Brent closed out the US session down -0.74% at US$67.25 bbl to remain below all major moving averages.

- The IEA forecasts that global oil demand will rise by up to 2.5m barrels a day from 2024-2030 despite EV's forecasting to displace up to 5m barrels per day over the next decade.