TRY: Limited Reaction Across Local Markets to CBRT Decision

Jul-24 11:09

- Limited reaction across both local currency and equity markets to the rate decision, with any initial moves already fading. While the 300bp move is a touch above median consensus of 250bps, some analysts had been anticipating a cut of this size.

- Yesterday, an Ekonomi columnist noted that whether the reduction is 250bps or 350bps is irrelevant because the monthly growth limits of 2.5% for SMEs and 1.5% for large businesses will remain in place for TRY-denominated commercial loans. The writer added that businesses are unable to access financing and that unless these monthly limits are addressed, interest rate reductions will not directly impact financing costs.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Twist Steeper Ahead Of A Busy Session Including Powell and 2Y Supply

Jun-24 10:57

- Treasuries trade twist steeper although are within yesterday’s wide ranges.

- The front end is supported by crude oil futures adding to yesterday’s heavy declines on limited Iran retaliation to US strikes. The long end sees some spillover from German supply expectations following Reuters headlines with the DFA Q3 announcement, although losses have been pared there.

- Today sees a heavy session, with Fedspeak headlined by day one of Fed Chair Powell’s semi-annual congressional testimony plus an update on consumer confidence in June before 2Y supply.

- Cash yields are 1.9bp lower (2s) to 1.2bp higher (30s).

- TYU5 deals at 111-09+ (-05) on reasonable cumulative volumes of 385k.

- Yesterday’s high of 111-20+ comfortably breached resistance at 111-14+ (Jun 5 high and 61.8% retrace of May 1-22 downleg), highlighting a stronger reversal. It opens 111-30 (76.4% retrace) whilst support is seen at 110-21+ (50-day EMA).

- Data: Current account Q1 (0830ET), Philly Fed non-mfg Jun (0830ET), FHFA and S&P CoreLogic house prices Apr (0900ET), Conf Board consumer survey Jun (1000ET), Richmond Fed mfg Jun (1000ET)

- Fedspeak: Powell text (likely 0830ET), Hammack on mon pol (0915ET), Powell appearance (1000ET), Williams keynote remarks (1230ET), Kashkari town hall (1345ET), Collins on housing (1400ET), Barr (1600ET), Schmid on economic outlook (2015ET) – see FED bullet

- Coupon issuance: US Tsy $69B 2Y note auction - 91282CNL1 (1300ET). Last month’s 2Y auction was solid, with a 1bp trade through for its highest since Feb, although had some mixed peripheral stats.

- Bill issuance: US Tsy $55B 6W Bill auction (1130ET)

PIPELINE: Corporate Bond Roundup: $2B IFC Guidance Updated

Jun-24 10:57

- Date $MM Issuer (Priced *, Launch #)

- 06/24 $1B #JBIC 3Y SOFR+44

- 06/24 $2B IFC 5Y SOFR+41

- 06/24 $1B CAF 3Y SOFR+69

- 06/24 $Benchmark Denmark 2Y +4

- 06/24 $Benchmark Westpac 5Y +70a, 5Y SOFR

- 06/24 $Benchmark Toyota 2Y +65a, 5Y +90a, 10Y +105a

- 06/24 $Benchmark Nomura PerpNC5.5 7.75%a, 5Y +130a, 10Y +150a

- 06/24 $Benchmark Kazakhstan 7Y 5.25%a, 12Y 5.625%a

- $14.45B Priced Monday

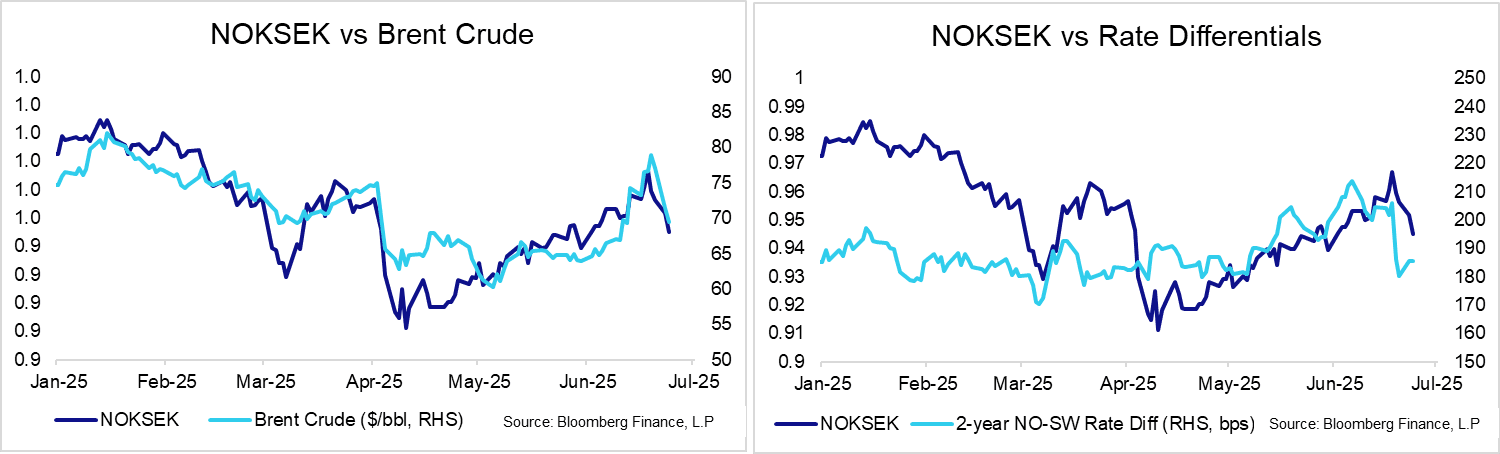

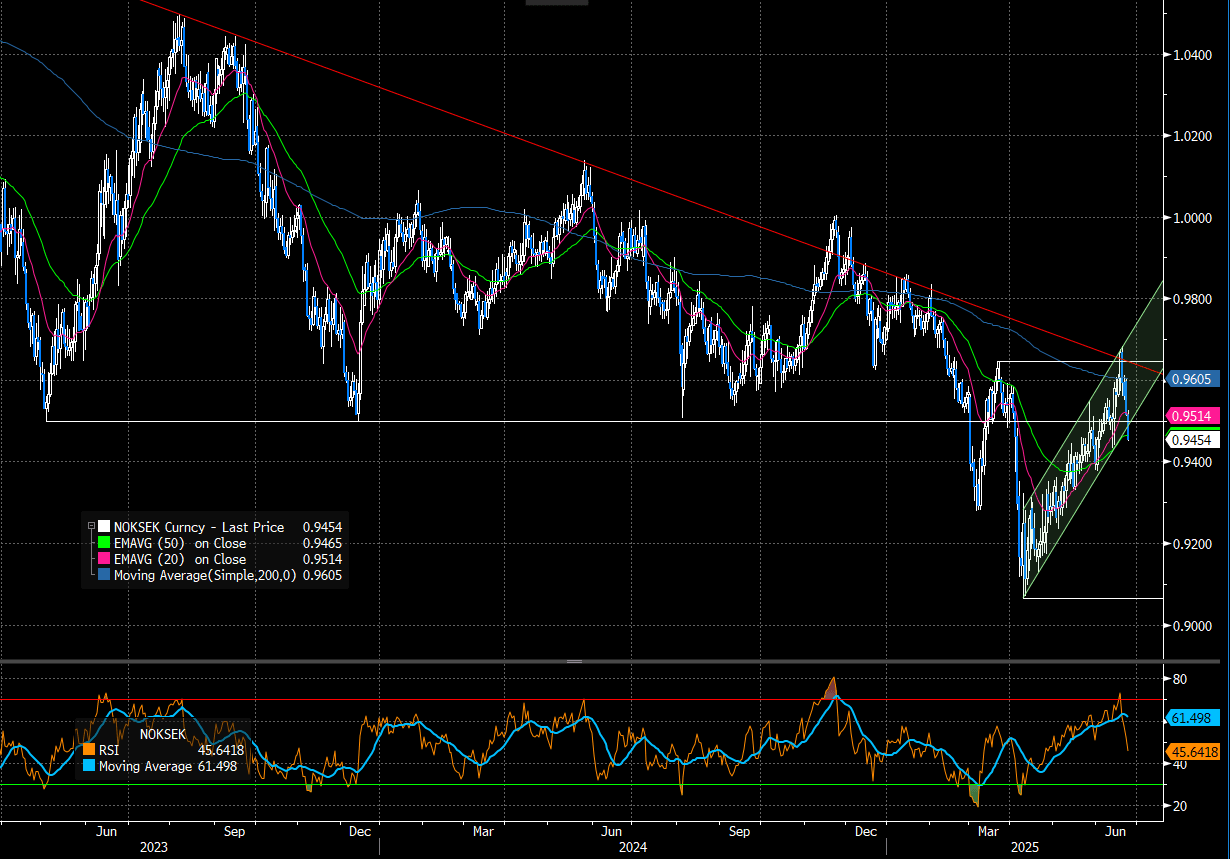

SCANDIS: NOKSEK Pierced Trendline Support, Bearish Threat Strengthens

Jun-24 10:56

NOKSEK has pierced the trendline drawn from the April 9 low (0.9498 today), breaking out of the bullish channel that had contained price action since US President Trump’s initial reciprocal tariff rollback. The cross is now hovering just below the 50-day EMA at 0.9465, down 0.7% today. A clear breach of this moving average would strengthen a bearish threat, and expose the next supports at 0.9434 (June 12 low) and 0.9374 (50% retracement of the April 9 – June 19 rally).

- The 15% reversal lower for Brent crude futures has been the primary driver of this week’s pullback in NOKSEK, strengthening the downside momentum spurred by last week’s rate decisions. A reminder that Norges Bank cut rates to 4.25% against all expectations on Thursday, providing a much greater surprise than the Riksbank’s more dovish-than-expected decision.

- There are mixed opinions amongst analysts on the outlook for Scandi FX:

- Goldman Sachs believe the Scandis should perform well against the USD ahead, “with both currencies standing to benefit from the theme of shifting asset allocations that should be supportive of the Euro and its satellites more broadly”.

- JP Morgan also favour fading last week’s dovish reactions in SEK and NOK, re-entering a short EUR vs Scandi basket trade. They note that “the themes of relative growth, fiscal space, rate pass through, carry-to-value rotation and repatriation flows are still in favour of the trade. For NOK, we also think the currency will be a prime candidate for carry efficient USD short structures if and when the market re-engages with its USD bearish position”.

- Meanwhile, Danske Bank “maintain an upward sloping forecast profile for EUR/NOK”, seeing “oil support to NOK as a temporary driver and expect a return of headwinds from relative rates and structural challenges”. Additionally, “despite SEK benefits from US-Europe rotation flows, weak growth acts as a SEK negative, leading us to maintain a positively sloping profile for EUR/SEK”.

- This week’s Scandi calendar includes the Riksbank’s June minutes tomorrow morning and the June Economic Tendency Indicator on Thursday. In Norway, labour market data will be in focus (May LFS on Thursday, June registered unemployment in Friday).

Figure 1: NOKSEK Since 2023

Figure 2: NOKSEK vs Crude and Rate Differentials