EM LATAM CREDIT: LATAM Credit Market Wrap

Source: Bloomberg Finance L.P.

Measure Level Δ DoD

5yr UST 3.62% +2bp

10yr UST 4.04% +0bp

5s-10s UST 41.3 -1bp

WTI Crude 58.5 -0.2

Gold 4209 +66.1

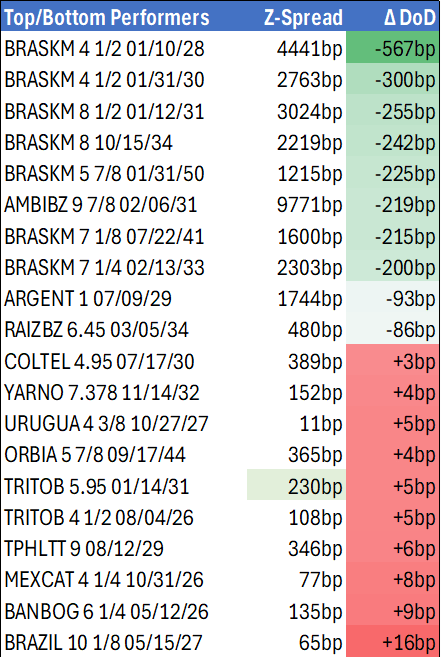

Bonds (CBBT) Z-Sprd Δ DoD

ARGENT 3 1/2 07/09/41 1234bp -16bp

BRAZIL 6 1/8 03/15/34 231bp -10bp

BRAZIL 7 1/8 05/13/54 317bp -9bp

COLOM 8 11/14/35 336bp -2bp

COLOM 8 3/8 11/07/54 393bp -2bp

ELSALV 7.65 06/15/35 387bp -5bp

MEX 6 7/8 05/13/37 221bp -6bp

MEX 7 3/8 05/13/55 268bp -6bp

CHILE 5.65 01/13/37 130bp -5bp

PANAMA 6.4 02/14/35 242bp -5bp

CSNABZ 5 7/8 04/08/32 593bp -64bp

MRFGBZ 3.95 01/29/31 254bp -31bp

PEMEX 7.69 01/23/50 485bp -6bp

CDEL 6.33 01/13/35 189bp -3bp

SUZANO 3 1/8 01/15/32 179bp -5bp

FX Level Δ DoD

USDBRL 5.46 -0.03

USDCLP 961.06 -0.08

USDMXN 18.5 -0.03

USDCOP 3895.08 -30.71

USDPEN 3.40 -0.02

CDS Level Δ DoD

Mexico 94 (3)

Brazil 145 (9)

Colombia 207 (1)

Chile 54 (3)

CDX EM 97.63 0.08

CDX EM IG 101.28 0.01

CDX EM HY 93.21 0.24

Main stories recap:

· Short maturity Treasury yields inched back up 2bp to reverse yesterday’s move as major U.S. indexes recovered.

· The EM primary market cooled after elevated activity in prior weeks with only a couple of new issues globally.

· LATAM credit markets remained volatile with Brazil corporate bonds roaring back after last week’s oversold conditions. Raizen and CSN were notable outperformers with bonds up 2-4 points.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

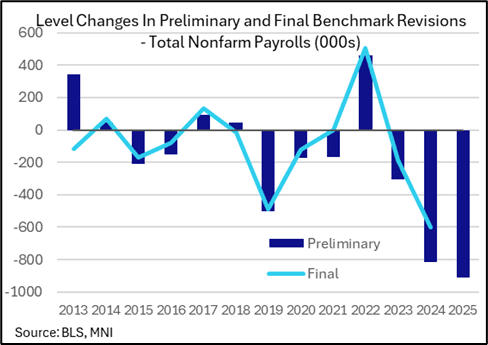

US OUTLOOK/OPINION: Macro Since Last FOMC - Labor: Heavy Downward Revision [3/5]

- Whilst on the subject of payrolls, the BLS preliminary estimate for the annual payrolls benchmark revision points to a substantial downward revision of -911k over the twelve months to March 2025 – to be known for sure early next year with the actual revision.

- Analyst estimates were wide-ranging but we estimated a median of -750k, mainly in a range of -500k to -1mn (sometimes given as a similar range by each analyst) but with Barclays more pessimistic still with -1.1-1.3mn.

- Governor Waller, the only FOMC member we’d seen offer an estimate, had pencilled in a monthly hit of around 60k, i.e. a downward revision of a little over 700k. Note that this compares with last year’s preliminary estimate of -818k before the -598k in the actual benchmark revision published with the January monthly payrolls report released in February.

- Taking these revisions at face value (which history suggests is likely overly negative), the average pace of monthly payrolls growth of 147k in the twelve months to Mar 2025 would have been 71k. As for private payrolls, the -880k preliminary downward revision implies average monthly private payrolls growth would be revised down from 122k to 49k.

- Beware extrapolating this monthly downward revision to the aforementioned three-month average in seasonally adjusted payrolls growth of 29k as of August but the risk is certainly on payrolls growth to have been even weaker than currently estimated.

US STOCKS: Indices Close To All-Time Highs, Alphabet Joins The $3tn Club

- ESZ5 at 6671.25 (+0.4%) is holding onto solid gains for the day having eased only slightly off fresh all-time highs of 6681.25, with gains at the time extended by Trump suggesting a move to semi-annual reporting for corporates.

- Next resistance is seen at 6685.25 (1.00 proj of Aug 1-15-20 price swing) after which lies the round 6700. Support meanwhile isn’t seen until 6546 (20-day EMA).

- Some of the large idiosyncratic moves at play have been pared, with gains becoming a little more broad-based compared to two hours ago. That includes Tesla (+3.0%, gains pared having been 7.5% at one point) after Musk bought ~$1bn of shares, Alphabet (+3.4%) extending trend gains after a recent antitrust ruling with it today becoming the fourth company with a market cap in excess of $3trn and Oracle (+2.1%) attributed to data center construction expectations along with Seagate Technology up 7.2%. Other notable gains include Amazon (+1.5%) and Apple (+0.9%).

- Nvidia is back in the red (-0.4%) having clawed back to flat after receiving an intraday boost following a lack of fresh headlines at the China trade delegation press conference after Bessent-He talks. It had dragged pre-market and earlier in the session after China said it violated antitrust regulations with its acquisition of Mellanox.

- Leaders: Communication services (+2.0%), consumer discretionary (+0.9%) and IT (+0.6%).

- Laggards: Consumer staples (-1.0%), health care (-0.9%) and materials (-0.8%).

- The tech-heavy nature of day’s gains unsurprisingly sees NDQ outperform at +0.7% (20 pts off earlier all-time highs of 24274.80). The Russell 2000 also performs well (+0.4%) whilst the Dow Jones lags (+0.1%).

EURJPY TECHS: Trend Needle Points North

- RES 4: 177.08 2.000 proj of the Feb 28 - Mar 18 - Apr 7 price swing

- RES 3: 175.43 High Jul 11 ‘24 and a key medium-term resistance

- RES 2: 174.86 1.764 proj of the Feb 28 - Mar 18 - Apr 7 price swing

- RES 1: 173.97 High Jul 28 and the bull trigger

- PRICE: 173.44 @ 20:30 BST Sep 15

- SUP 1: 171.39 50-day EMA

- SUP 2: 169.73/45 Low Jul 31 / 23.6% of the Feb 28 - Jul 28 bull leg

- SUP 3: 168.46 Low Jul 1

- SUP 4: 167.46 Low Jun 23

The trend set-up in EURJPY is unchanged, it remains bullish and attention is on key resistance and the bull trigger at 173.97, the Jul 28 high. Clearance of this level would confirm a continuation of the bull phase. Moving average studies are in a bull-mode position too, highlighting a primary uptrend. A break of 173.97 would open 174.86, a Fibonacci projection. Key support to watch lies at the 50-day EMA at 171.39.