EM LATAM CREDIT: LATAM Credit Market Wrap

Source: Bloomberg Finance L.P.

Measure Level Δ DoD

5yr UST 3.93% +2bp

10yr UST 4.35% +1bp

5s-10s UST 41.3 -1bp

WTI Crude 66.9 -1.5

Gold 3325 +11.8

Bonds (CBBT) Z-Sprd Δ DoD

ARGENT 3 1/2 07/09/41 900bp +6bp

BRAZIL 6 1/8 03/15/34 249bp -1bp

BRAZIL 7 1/8 05/13/54 348bp -2bp

COLOM 8 11/14/35 392bp -7bp

COLOM 8 3/8 11/07/54 469bp -2bp

ELSALV 7.65 06/15/35 427bp +2bp

MEX 6 7/8 05/13/37 249bp -2bp

MEX 7 3/8 05/13/55 314bp -1bp

CHILE 5.65 01/13/37 143bp -3bp

PANAMA 6.4 02/14/35 290bp -0bp

CSNABZ 5 7/8 04/08/32 579bp +3bp

MRFGBZ 3.95 01/29/31 281bp +1bp

PEMEX 7.69 01/23/50 584bp +0bp

CDEL 6.33 01/13/35 203bp -1bp

SUZANO 3 1/8 01/15/32 173bp +3bp

FX Level Δ DoD

USDBRL 5.54 -0.03

USDCLP 950.42 +0.54

USDMXN 18.6 -0.00

USDCOP 4011.22 +3.09

USDPEN 3.55 -0.00

CDS Level Δ DoD

Mexico 102 (1)

Brazil 147 5

Colombia 216 0

Chile 53 (0)

CDX EM 97.70 0.12

CDX EM IG 101.34 0.07

CDX EM HY 93.95 0.14

Main stories recap:

Comments

Closing Comment

Closing Comment

· A new record high for the SPX was set as Delta Airlines signaled more certainty in the economic environment and reinstated a profit outlook, creating expectations of others to follow.

· The Treasury market absorbed the last leg of the monthly refunding with a solid 30-year auction and yields were little changed across the curve.

· The EM primary market marched on with two CEEMEA sovereign € deals, one for frequent issuer Turkey and one for debut issuer Bosnia and Herzegovina, while in LATAM we had Spain based LATAM electricity generator Enfragen issuing 7NC3 notes at 8.5%.

· Benchmark bond spreads in the EM secondary market were mixed in Asia while in CEEMEA they trended tighter and in LATAM they moved in a narrow, mixed range.

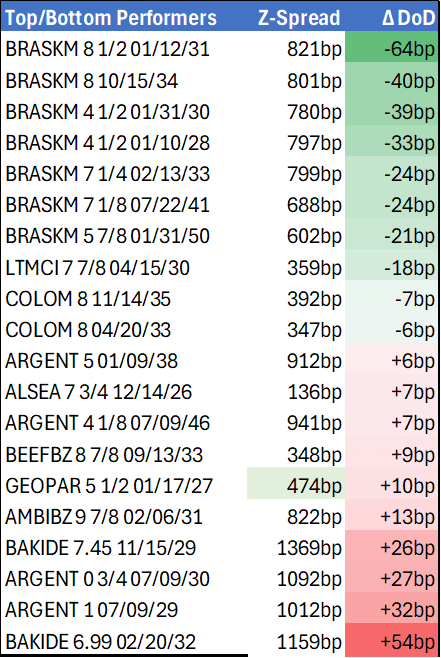

· Once again Brazil’s Braskem outperformed, following yesterday’s news of a potential tax incentives bill for the chemical industry making its way through congress.

· Also supportive for Braskem was today’s announcement of possible Brazil reciprocal tariffs on U.S. imports that could be beneficial as plastics are a major export to the country.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US OUTLOOK/OPINION: Upside CPI Surprise Can Tee Up A Hawkish Fed Next Week

- Friday’s payrolls report pushed back on some weak data in the build up to the release, showing only a mild increase in the unemployment rate and decent jobs growth considering a backdrop of heavily reduced immigration. It’s seen a Fed rate path back towards the most hawkish levels seen since February with a next cut only fully priced for October (a cumulative 28.5bp with 17bp for September).

- Data quality concerns aside, this renewed hawkish shift could offer greater sensitivity to a downward surprise in Wednesday's US CPI report, especially if driven by less volatile services components. However, with expectations that larger tariff impacts will only show in the summer, a downside surprise might have limited legs in market reaction. Conversely, a stronger increase could further push out timing of the next Fed cut to December along a flattening in the Treasury curve.

- This release lands in the media blackout ahead of the Jun 17-18 FOMC meeting. There’s clearly no need for any non-conventional blackout steers (Fed Funds show 0bp of rate moves for the decision) but the report will impact the new economic forecasts and dot plot in the SEP with this meeting. The median dot in the March round (made ahead of touted but unknown details of the Apr 2 “Liberation Day” reciprocal tariffs) pencilled 50bp of cuts for 2025 before another 50bp of cuts in 2026. However, four saw just a single 25bp cut in 2025 and another four saw zero cuts. With many Fed speakers subsequently pushing for further patience, a hawkish surprise with this month’s CPI/PPI reports could help embolden more members to pencil in at most one cut in the year.

- Talk of hikes remains mostly elusive although Governor Cook (permanent voter, usually leans dovish) noted on Jun 3 a need to be open to “all possibilities”. Her speech itself hewed very close to the FOMC majority's view on monetary policy without giving much away on her personal views on future rates, saying that she believed: "The current stance of monetary policy is well positioned to respond to a range of potential developments. Trade policy changes and the response of financial markets, firms, and consumers suggest risks to both sides of our dual mandate. As I consider the appropriate path of monetary policy, I will carefully consider how to balance our dual mandate, and I will take into account the fact that price stability is essential for achieving long periods of strong labor market conditions." However, in Q&A she intriguingly noted that "we have to be open to all possibilities. We don't know how tariffs are going to play out. One could imagine those scenarios - cutting, staying or hiking, happening." It's not often these days we hear Fed governors even mention the possibility of hikes, even if of course that's part of keeping every possibility "open".

USDCAD TECHS: Gains Considered Corrective

- RES 4: 1.4200 Round number resistance

- RES 3: 1.4111 High Apr 4

- RES 2: 1.3901/1.4016 50-day EMA / High May 12 and 13

- RES 1: 1.3782 20-day EMA

- PRICE: 1.3683 @ 16:40 BST Jun 10

- SUP 1: 1.3611 Low Oct 8 2024

- SUP 2: 1.3579 1.500 proj of the Feb 3 - 14 - Mar 4 price swing

- SUP 3: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

- SUP 4: 1.3473 Low Oct 2 2024

The trend structure in USDCAD remains bearish and short-term gains are considered corrective. Support at 1.3686, the May 26 low and a bear trigger, has recently been cleared. This confirms a resumption of the downtrend and maintains the price sequence of lower lows and lower highs. Sights are on 1.3579 next, a Fibonacci projection. Resistance at the 50-day EMA is at 1.3901 - a key level. The 20-day EMA is at 1.3782.

US OUTLOOK/OPINION: CPI Services Moderation Eyed More Broadly

- These developments in travel-related services are likely to play a role in determining the market reaction to “supercore” inflation (core services ex OER & primary rents).

- The six estimates we’ve seen average 0.18% M/M (range 0.09-0.26) after 0.21% M/M in April, for some relative stability after Q1 saw a huge 0.76% in Jan before 0.22% in Feb and -0.24% in Mar.

- Separately, rental services inflation is expected to moderate slightly to 0.33% for OER and 0.31% for primary rents. A weighted average of the two accelerated to 0.39% M/M in Mar and 0.35% M/M in Apr after four months averaging 0.29% through Nov-Feb had seen a long-awaited return to the 0.28% averaged in 2019 before the pandemic.