ASIA FX: Some Divergences In USD/Asia Correlations With US Real Yields

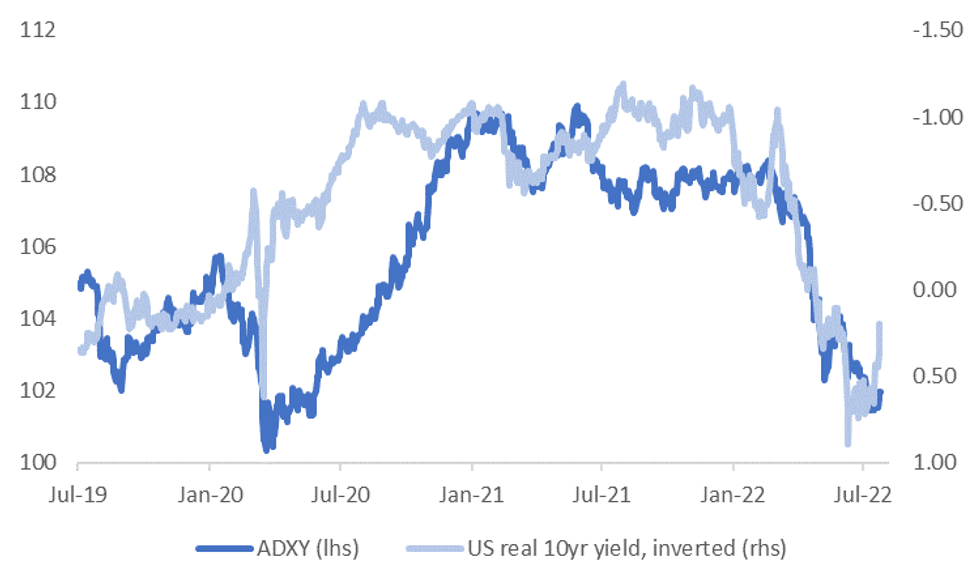

The ADXY currency index has certainly benefited from lower Fed tightening expectations in recent sessions. The first chart below plots the ADXY against the real US 10yr yield, note that the real yield is inverted on the chart.

- The relationship between the two series has been particularly tight since the start of the year.

- If we look at the individual USD/Asia currency pairs, the correlations for the past 6 months are strongly positive. That is, higher US real yields driver USD/Asia pairs higher, all else equal and vice versa when real yields fall. Most correlations are in the 80-90% range.

Fig 1: ADXY & US Real 10yr Yield

Source: J.P. Morgan/MNI/Market News/Bloomberg

Source: J.P. Morgan/MNI/Market News/Bloomberg

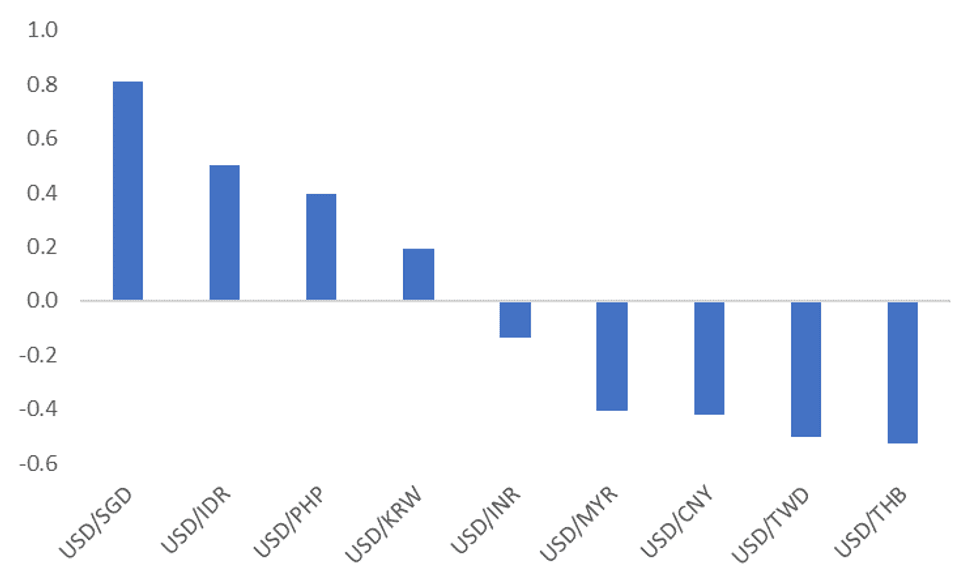

- On a shorter term basis, for the past month, correlations are quite divergent though. See the second chart below.

- If we continue to see real yields correct lower, current correlations suggest USD/SGD, USD/IDR, USD/PHP and USD/KRW may see greater downside compared to the rest of the USD/Asia bloc.

- Interestingly, today IDR and PHP have been the best performers within Asian FX, although clearly other factors could be at play other than the sharp US real yield drop overnight (from +36bps to +20bps).

- For SGD, we suspect this high correlation reflect its correlation the majors (EUR, JPY etc), which themselves are influenced by US yield shifts. For IDR and PHP, it likely reflects sensitivity to external financing conditions, particularly given high foreign ownership levels of Indonesian debt and the Philippines large current account deficit at the moment.

- For the other USD/Asia pairs, we can obviously see a shift in correlations, but it may be the case other drivers are more important for these currencies at the moment.

Fig 2: USD/Asia Correlations With Real US 10yr Yield - Past Month

Source: J.P. Morgan/MNI/Market News/Bloomberg

Source: J.P. Morgan/MNI/Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILT TECHS: (U2) Key Support Remains Intact

- RES 4: 116.00 Round number resistance

- RES 3: 115.55 High Jun 6

- RES 2: 115.02 High Jun 8

- RES 1: 113.61/14.55 20-day EMA / High Jun 24

- PRICE: 112.15 @ Close Jun 28

- SUP 1: 111.81 Low Jun 28

- SUP 2: 110.57 Low Jun 21

- SUP 3: 109.89/60 Low Jun 16 / 4.50 proj of May 19 - 24 - 26 swing

- SUP 4: 109.33 Low Jul 8 2014 (cont)

Gilt futures have pulled back from last week’s high of 114.55 (Jun 24). Despite the move lower, a short-term bullish corrective cycle remains in play and a resumption of gains would signal scope for a climb towards 115.55, the Jun 6 high. The broader trend remains down with key support and the bear trigger defined at 109.89, the Jun 16 low. A break of this level would confirm a resumption of the downtrend.

EUROSTOXX50 TECHS: (U2) Still Trading Above Recent Lows

- RES 4: 3774.00 High Jun 9

- RES 3: 3689.00 High Jun 10

- RES 2: 3630.50 50-day EMA

- RES 1: 3584.00 High Jun 27

- PRICE: 3502.00 @ 05:31 BST Jun 29

- SUP 1: 3384.00 Low Jun 16 and the bear trigger

- SUP 2: 3300.00 Round number support

- SUP 3: 3241.70 1.382 proj of the Mar 29 - May 10 - Jun 6 price swing

- SUP 4: 3189.10 1.50 proj of the Mar 29 - May 10 - Jun 6 price swing

EUROSTOXX 50 futures continue to trade above recent lows and a corrective cycle remains in play The primary trend direction is down though. Moving average studies are in bear mode condition and this highlights a clear bearish trend set-up. Firm resistance is at 3630.50 the 50-day EMA and key support is at 3384.00, Jun 16 low. A breach of the 50-day EMA is required to strengthen S/T bullish conditions, signalling scope for a stronger recovery.

CROSS ASSET: Pullback In NRW CPI Provides EUR Downside & Bid For German FI

EUR/USD trades as low as $1.0506 as the German State of North Rhine Westphalia sees headline Y/Y inflation ease to +7.5% in Y/Y terms in June (prev. +8.1%), while the M/M reading printed at -0.1% (prev. +0.9%). EURUSD trades off of worst levels of the session last, $1.0510. German fixed income futures (Bund, Bobl & Schatz) shunted higher on the print.