TWD: Lagging Equity Gains, Focus On TSMC Monthly Sales, Sep Exports

USD/TWD spot remains within recent ranges, last around 30.50, only a touch off recent highs (30.57). TWD is notably lagging the global/local tech equity surge (see the chart below). We are above the 100-day EMA (30.38), whilst on the topside the 200-day rests at 30.84 on the topside.

- To be sure, higher USD/JPY levels will be providing an offset to the better tech led equity tone. USD/TWD has maintained a positive levels correlation with USD/JPY.

- We also haven't seen positive inflows this week from offshore investors (with -$344mn in net outflows recorded up to Wednesday). YTD inflows are just over $9bn, so offshore investors may be waiting for fresh positive catalysts before adding further to longs.

- We do get TSMC monthly sales this afternoon, a good gauge of tech demand/sentiment. If we see inflows resume, USD/TWD should be biased lower.

- Also out later on is Sep trade figures. Markets are looking for a 38.8%y/y export print, versus 34.1% in August. Re-accelerating export growth would be seen as a positive by the market.

Fig 1: USD/TWD Spot Versus Local Equities (Inverted)

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA: Bond Futures Fall Tuesday

- China's major bond futures are all lower today for a third consecutive day of falls.

- The 10-Yr is lower by -0.05 at 107.790 to move further below all major moving averages.

- The 2-Yr is lower by -0.01 at 102.38 to move away from the 20-day EMA of 102.38.

- Government bond yields are marginally lower with the CGB 10-Yr at 1.78%.

GLOBAL MACRO: Supply Side Pressures Neutral, Commodity Prices Mixed

Global indictors have been mixed suggesting that we could see inflation rates remain fairly steady. Some commodity prices were higher in August, such as food, while others were lower, like oil. In September so far metals are higher while oil prices and container rates continue to trend lower.

- There had been concerns that increased US protectionism could adversely impact supply chains. The NY Fed global supply chain pressure index shifted slightly positive in May but returned to -0.1 in August but overall it has remained very close to neutral through 2025 implying few pressures.

Global inflation vs supply chain pressures

- Shipping rates are likely either to be disinflationary or neutral. The FBX container shipping rate fell 16.8% m/m in August to be down 61% y/y with the China to North America’s east coast route down 29.7% m/m & 66.9% y/y. The bulk goods Baltic Freight index rose for the third straight month in August and is slightly higher this month.

- Brent crude fell for the second straight month in August and has started September lower. It is now down around 10% YTD. With the market widely expected to be in surplus, oil is unlikely to add to inflation pressures.

- FAO food prices have only fallen in two of the last 8 months. Annual inflation has stabilised but is yet to moderate. Processed rice prices rose almost 2% in August but were down over 40% y/y and have started September lower.

- LME metal prices were slightly weaker in August but still up 5.9% y/y and September so far are looking higher with all metals up except lead. Iron ore was higher last month and could post a third straight monthly increase this month. Wool is also up and has been trending higher since last October.

Global inflation vs food & oil prices

Source: MNI - Market News/LSEG

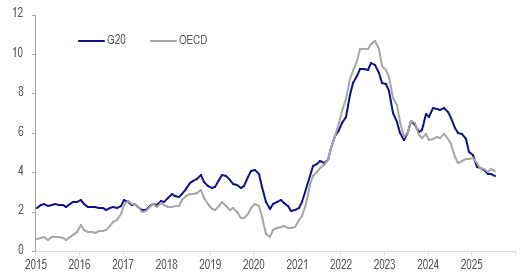

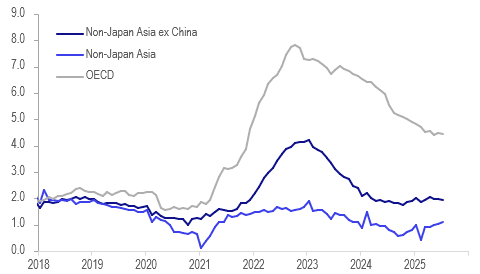

GLOBAL MACRO: Underlying CPI Inflation Appears To Have Stabilised

G20 inflation has been trending gradually lower over 2025 with it reaching 3.8% y/y in July, the lowest in over four years. However, both headline and underlying OECD inflation have been fairly stable since March with disinflation progress stalling. Non-Japan Asia ex China core has also been steady around 1.8-2% since the start of 2024. The impact of tariffs on inflation especially in the US remains highly uncertain but lower global demand could put downward pressure on prices.

Global headline CPI y/y%

Source: MNI - Market News/LSEG

- July OECD headline inflation moderated 0.1pp to 4.1%, while core was stable at 4.5%. They peaked at 10.7% y/y and 7.8% respectively in October 2022. August preliminary euro area CPI was steady around 2%.

- US August CPI prints on Thursday and is forecast to show core steady at 3.1% but headline picking up 0.2pp to 2.9%. The data will continue to be watched closely for tariff impacts.

- Non-Japan Asia ex China saw headline inflation moderate 0.3pp to 1.5% y/y in July, the lowest since our aggregate began in 2012. Core was 1.9% y/y down from 2.0% after it peaked at 4.2% in January 2023. China’s underlying inflation picked up 0.1pp to 0.8% in July, the highest in almost 18 months.

- August Asian releases to date saw lower headline and core inflation in Korea and Indonesia, while Taiwan and Thailand were little changed and the Philippines saw both rise.

Asia vs OECD core CPI y/y%

Source: MNI - Market News/LSEG