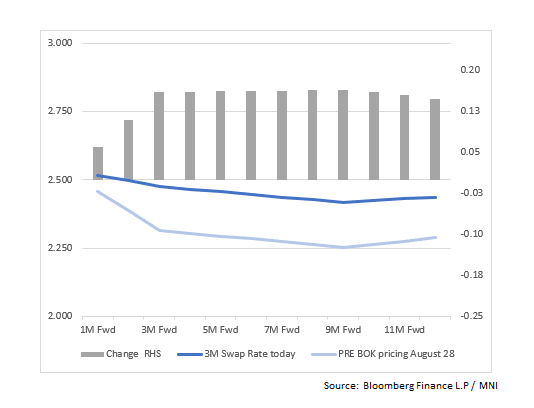

SOUTH KOREA: Korean update Swaps Pricing Vs. Pre-BOK Meeting Levels

- The Korean swaps curve no longer has a full rate cut priced in now by mid-year next year, having earlier this month priced one in via the 7mth forward.

- The probability of a cut over the next month is 9% (from 12%) and three months is 26%, from 34% earlier this month. The MIPR function on BBG has -4bps of cuts priced in over the next 3 months, and -14bps over the next 12 months, which has remained stable.

- The BOK next meets on the 23 October.

- The key for the BOK and the bond market remains the focus by the government on the housing market. Additional attempts to cool the overheated Seoul property markets have been announced this week yet today's release of the September Household loans data, showed an increase in mortgages.

- At present it seems less likely for further BOK action on monetary policy whilst the focus on cooling the property market remains.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

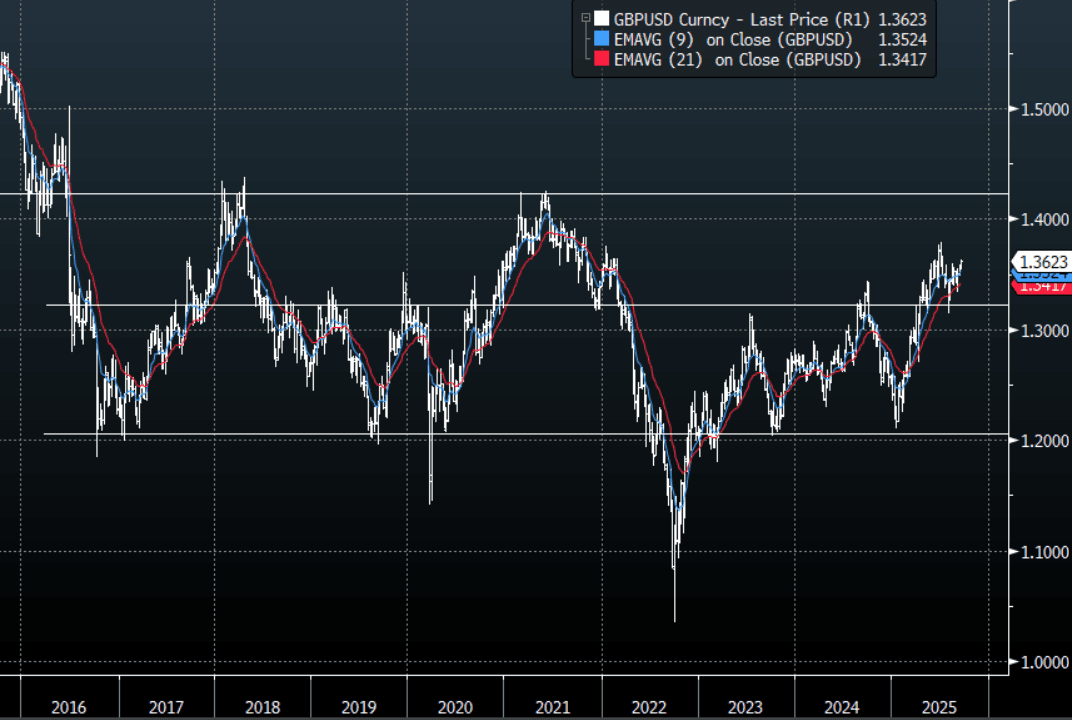

GBP: GBP/USD - Trying To Regain Its Upward Momentum, Employment Today

The GBP/USD had a range overnight of 1.3553-1.3620, Asia is trading around 1.3615. Cable looks to be trying to regain its momentum higher and break back through the 1.3600/50 area. A big week for event risk, unemployment today, then CPI and the BOE, and a sprinkle of FOMC just to add some spice. Should the market get the scenario it is hoping for from the FOMC the USD could begin to regain its momentum lower. This could potentially then see GBP/USD break out of its multi-month 1.3150 -1.3650 range and begin another leg higher. The initial target is the year's highs just below 1.3800, a sustained break above here would target the 1.4200/1.4300 area.

- MNI UK DATA PREVIEW: September 2025 CPI and Labour Release. Both labour market data and CPI data will have already been released to MPC members this morning, and both data releases are important for future monetary policy despite markets pricing in only around a 1/3 probability of a rate cut this year (and not fully pricing a 25bp cut until April 2026). We think that both Governor Bailey and Deputy Governor Ramsden are very much focused on the labour market print (probably a little more so than inflation). Along with Breeden, all three members are likely needed on board in order for another rate cut this year to materialize. We think that the market focus will switch back to AWE private regular pay data. Both the median and mean estimate from the previews that we have read is that this will fall to 4.65%Y/Y in the 3-months to July.

- MNI BOE WATCH: Seen Slowing QT And Holding Policy Rate. The Bank of England is widely expected to leave its policy rate unchanged at 4.0% at its September meeting and to keep its guidance intact while voting to ease back on gilt sales. The MPC vote split will, as ever, be in the spotlight with the most common view that it will be seven-two for no change, with independent members Swati Dhingra and Alan Taylor, who have both highlighted the fragility of economic activity rather than inflation persistence, voting for a 25bp cut. Taylor initially backed a 50bp cut in August.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 1.3600(GBP401m). Upcoming Close Strikes : 1.3250(GBP401m Sept 19) - BBG

- Data/Event: Unemployment, CPI Tomorrow, BOE Thursday

Fig 1: GBP/USD spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Weaker At Lunch, Koizumi/Kato Combo Weighs

At the Tokyo lunch break, JGB futures are weaker, -8 compared to settlement levels, after giving up early gains as trading resumed following the long weekend.

- Today, the local calendar will see the Tertiary Industry Index.

- (Bloomberg) “JGB traders are leaning hawkish as Shinjiro Koizumi taps Finance Minister Kato to steer his campaign. Traders see that pairing as the stronger ticket in the LDP race, and one that could give the Bank of Japan room to raise interest rates before year-end.”

- (Dow Jones) “The JGB yield curve may modestly flatten, assuming the Bank of Japan raises rates at a pace of 50bps per year, DBS Group Research's Eugene Leow says. The shape of the JGB yield curve depends largely on how aggressive Japan's central bank is likely to act in the coming few quarters, the senior rates strategist says.”

- Cash US tsys are marginally richer in today's Asia-Pac session after yesterday's modest rally.

- Cash JGBs are flat to 1bp cheaper across benchmarks. The benchmark 10-year yield is 0.9bp higher at 1.603% versus the cycle high of 1.649%.

- Swap rates are flat to 2bps higher. Swap spreads are wider.

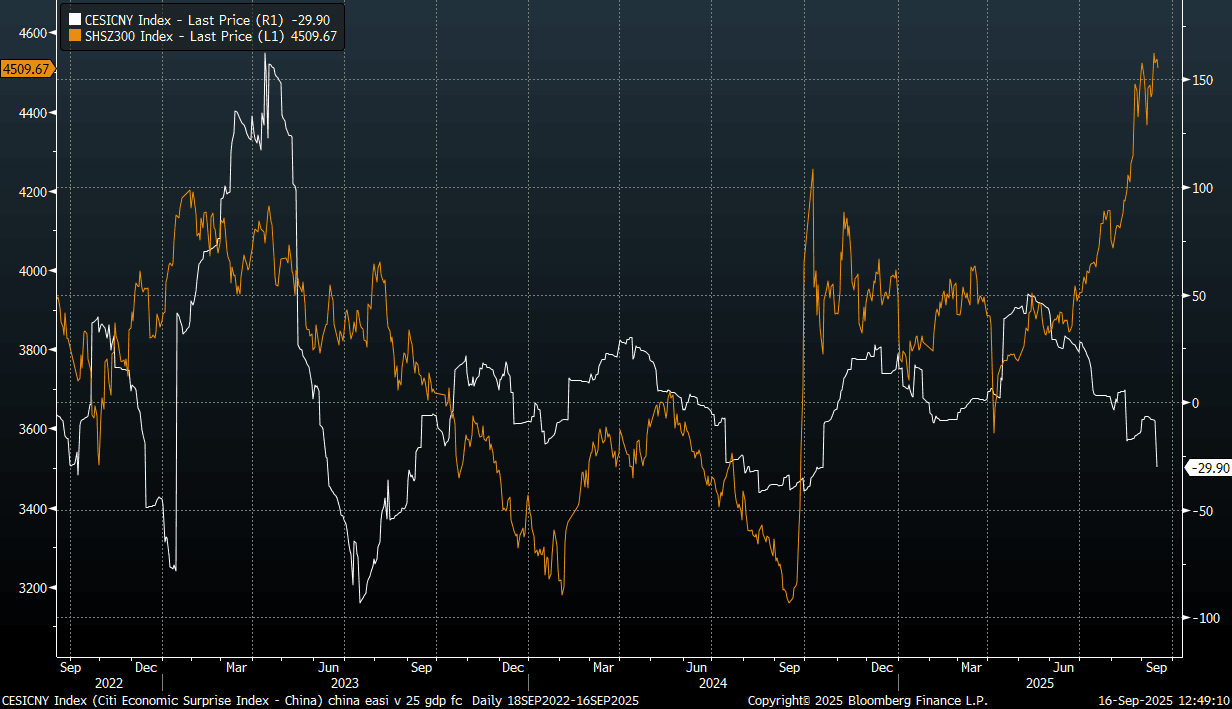

CHINA: China Surprise Index At Fresh 2025 Lows, But Local Equities Supported

Yesterday's softer than expected China data outcomes for August sent the Citi China economic surprise index (EASI) to fresh lows for 2025. It also widened the wedge between this surprise index and China equity trends, see the chart below. Even with mainland China equities down modestly so far today, this only closes the gap a touch (CSI 300 is off around 0.50%).

- To be sure, there have been divergences in the past but usually what we see is positive correlation between the two series, with positive data surprises usually coinciding with higher equity index levels. At face value, concerns around China growth momentum could weigh on equity trends at some stage.

- Still, we may remain divergent in the near term. Firstly, China isn't alone is having softer data outcomes recently relative to expectations. The other major economy EASIs have also softened (although they remain at higher levels relative to the China index). This is impacting these equity markets either, where in the US for example we have hit fresh record highs.

- Focus remains in the tech/AI space. For China the Chinext is up over 40% from start July levels, while the CSI 300 index is up a more modest 15% over the same period.

- The policy shift towards reducing excess capacity in parts of the economy may also weigh on economic activity but aid profitability. This has been a focus in the steel sector in recent months.

- Finally, softer data may encourage views that easier policy settings/economic support will come from the China authorities. Easing Fed expectations has certainly been a support for US/tech led global equity indices in recent months.

Fig 1: Citi China Surprise Index (White Line) and CSI 300 Equity Index (Orange Line)

Source: Citi/Bloomberg Finance L.P./MNI