EU CONSUMER CYCLICALS: Kering: owner Artemis and Puma stake

(KERFP; NR/BBB+ Neg)

Leaks it was considering Puma sale was always confusing (given stock at lows) and helped keep alive concerns Artemis was stretched on its debt load. The below - when combined with Artemis stating it is not reliant on the Kering dividend recently - should shut-down any concerns.

'The person, who declined to be named as the information was private, said Artemis had been approached by many potential suitors for its stake, including private equity firms and sector peers, but that the firm was not negotiating anything. "Would we sell at this level? Never in our lives... We consider that Puma is worth much more than that," the person said, though echoed public comments from Artemis chairman Francois-Henri Pinault this week that Puma was not "strategic' - Reuters

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

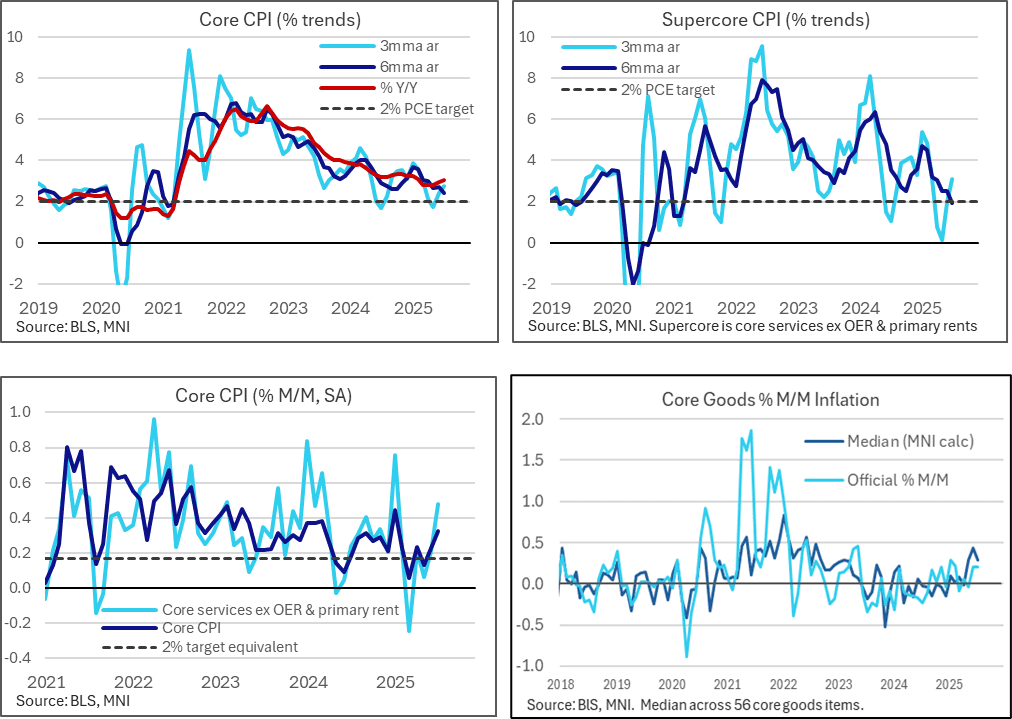

US DATA: US CPI Wrap: No Sign Of Faster Tariff Passthrough In July CPI Report

The July CPI report saw further acceleration in monthly core CPI inflation but it was driven by the volatile supercore category. Instead, core goods inflation, an area of focus for tariff passthrough clues, was surprisingly soft as it only maintained the monthly clip seen in June whilst median core goods inflation moderated after a strong increase in June.

- Core CPI inflation was exactly in line with the median unrounded analyst estimate we had seen for July at 0.32% M/M, accelerating from 0.23% in June and 0.13% in May for its strongest month since January.

- The breakdown relative to expectation was dovish however, as core goods underwhelmed (0.21% M/M vs average expectations closer to 0.4%) in a month that was expected to show increasing signs of tariff passthrough ahead of perhaps the largest monthly increases in the fall months. It follows a very similar 0.20% M/M in Jun after a weak -0.04% M/M in May.

- Notably, this came despite used cars prices exceeding expectations (0.48% M/M vs estimates closer to 0.3) although that’s still a modest increase after four consecutive monthly declines averaging -0.6% M/M.

- Indeed, MNI calculations of median core goods inflation across 56 items softened to 0.28% M/M after a particularly strong 0.44% in June and 0.29% in May. This is still a robust pace - it averaged 0.0% M/M in 2024 and 0.06% M/M in Q1 - but clearly doesn't show any further acceleration in what would have been a sign of accelerated tariff passthrough.

- The offsetting factor to softer than expected core goods inflation was core services (0.36% M/M vs average expectations around 0.30%), driven by the volatile “supercore” category at 0.48% M/M whilst rental inflation was exactly as expected.

- Airfares played a large role here (4.0% vs 1.5% expected) and as always won’t feed into PCE. Some notable PCE inputs meanwhile saw partly offsetting large moves from booming dental services (2.6% M/M, 4.3% of supercore CPI) and further declines in lodging (-1.0% M/M, 6.4% of supercore).

- Taking a step back, core CPI inflation firmed to 3.06% Y/Y (cons 3.0) after 2.93% Y/Y for its strongest since Feb 2025. Both three- and six-month run rates are tracking softer than this, at 2.8% and 2.4% annualized respectively.

- Adding to the net dovish take from core CPI details, headline CPI undershot with 0.20% M/M in July (MNI median 0.24) owing to downside surprises in both food (0.05% M/M vs expectations 0.25%, including food at home at -0.12% M/M for only the second decline in the past fifteen months) and energy (-1.1% vs 0.6%, despite gasoline being as expected).

- It saw headline CPI inflation little changed at 2.70% Y/Y after 2.67% in June, holding the prior acceleration from the April low of 2.31% Y/Y.

SECURITY: Russia And Ukraine Escalate Attacks Ahead Of Alaska Summit

Ukraine and Russia have intensified long-range strikes and ground operations ahead of Friday’s summit between Russian President Vladimir Putin and US President Donald Trump in Alaska.

- Ukraine's Security Service reports that Ukrainian drones hit a warehouse facility in Russia’s Tatarstan region - around 1,300 kilometres from the front line - which Kyiv claims houses an assembly plant for foreign drone components. The strike is the second this week targeting the facility, and follows a series of strikes on Russian energy infrastructure.

- Ukrainian President Volodymyr Zelenskyy said in an address yesterday that Russia is, “redeploying their troops ... for new offensive operations," warning Russia is, “not preparing for a cease-fire or an end to the war.”

- NYT reported earlier Russian forces have moved "several miles into Ukrainian-held territory in the east, threatening to outflank Ukraine’s positions."

- Finland-based military analyst Pasi Paroinen writes on X that Russian forces have “rapidly infiltrat[ed] past Ukrainian lines at a depth of roughly 17km during the past three days." A notable advance considering Moscow made few “meaningful net gains in terms of territory,” during June/July.

- The moves appear to be posturing ahead of the Alaska talks, with Trump acknowledging yesterday that there will be some “land swapping” in a likely deal.

- While Trump downplayed the prospect of a deal with Putin, the outcome in Alaska could set the tone for a potential upcoming meeting between Putin and Zelenskyy, with Kyiv fearing that Trump could be convinced to advocate for unfavourable ceasefire terms.

FED: KC Fed's Schmid Sounds Like He Would Dissent To A September Cut

Kansas City Fed President Schmid (2025 FOMC voter, hawk)'s comments in a speech Tuesday ("The Federal Reserve and Outlook for the Economy and Monetary Policy" - link) hint that he wouldn't support a rate cut as soon as September's FOMC meeting, and could even dissent against such a decision. He sees policy as "not very restrictive" and close to neutral and appears to view the debate over tariff-driven inflation as something of a distraction - instead the Fed should "monitor demand growth" in order to keep inflation "on a path to 2%".

- In short, "with the economy still showing momentum, growing business optimism, and inflation still stuck above our objective, retaining a modestly restrictive monetary policy stance remains appropriate for the time being. Though of course this is a position that I will continually reassess as we receive new data and information on inflation, the labor market, and the economy more generally."

- He says that "My support for a patient approach to changing the policy rate is based on two connected arguments. First, while monetary policy might currently be restrictive, it is not very restrictive. And second, given recent price pressures, a modestly restrictive stance is exactly where we want to be."

- He says that the current policy stance is "not far from neutral": "we are as close to meeting our dual mandate objectives of price stability and full employment as we have been for quite some time. And while uncertainties abound, I do not see strong evidence of a trend movement away from our mandates at this point." He points to financial market variables: "looking at financial markets, with stock prices near record highs and bond spreads near record lows, I see little evidence of a highly restrictive monetary policy."

- On the labor market, he appears to shrug off the weakly-perceived July employment report: "While it is true that payroll growth was weak over the summer, a broader set of indicators suggest a labor market that is in balance. " On inflation: "On the other side of the mandate, inflation remains too high." And on growth: "Currently, the economy continues to show strong momentum...I am hearing increased optimism as some of the uncertainty and concern around trade policy that spiked in April recedes. Overall, my expectation is that the economy will show continued resilience."

- On tariffs, he says that he wouldn't "characterize my view on tariffs and inflation as 'wait-and-see'", in part because "I will confidently forecast that a decade from now economists will still be arguing over exactly what impact the tariffs had on inflation. As such, I see no possibility that we will know the effect of the tariffs on prices, either as a one-off shock to the price level or a persistent inflation impetus, over the next few months."

- As such he'll be "data dependent" - while "the Fed cannot offset the effect of higher tariffs on prices, [] what the Fed can do is monitor demand growth, provide space for the economy to adjust, and keep inflation on a path to 2 percent. Overall, I am anticipating a relatively muted effect of tariffs on inflation, but I view that as a sign that policy is appropriately calibrated rather than a sign that the policy rate should be cut."