UK FISCAL: Just under 1/3 of VAT revenues come from retail / wholesale

Sep-19 11:58

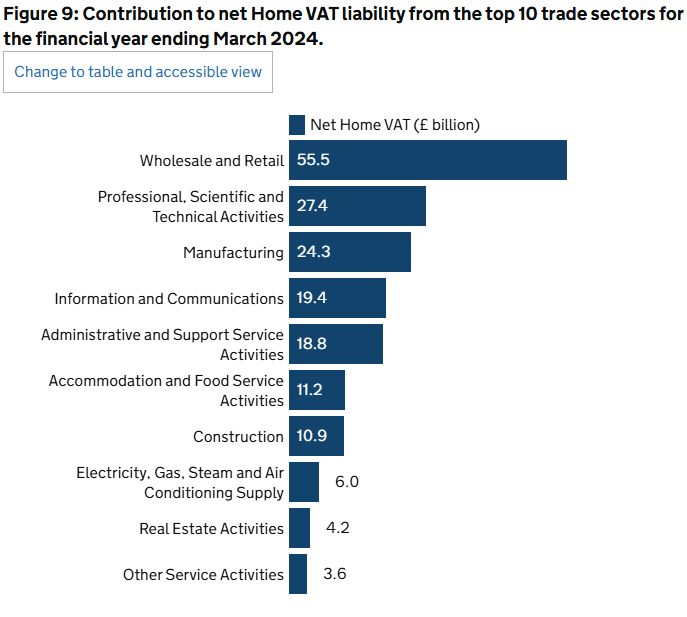

- UK retail sales / consumption data have been holding up pretty well so far this fiscal year, so there seems to be some surprise that VAT can be one of the contributors to the overshoot in this morning's borrowing data.

- We would note, however, that while VAT is often thought of as a consumption tax it has a much wider base than just retailed goods.

- The below chart shows the contribution of different sectors to VAT (on the latest data for the fiscal year 2023/24).

- Wholesale and retail trade account for 32% of total net home VAT liabilities in 2023/24 - just under a third of the total.

- Manufacturing is the third largest category accounting for almost 15% (and has been soft this year) while construction makes up 6-7% of liabilities.

- There is also a huge amount of services sectors here.

- Note also that the OBR noted in its monthly commentary that people may be spending more on food (which is VAT exempt) as food prices have increased, and reducing consumption of other goods.

Chart source: HMRC Statistics

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGB SYNDICATION: Finland New 7-year Apr-32 RFGB: Allocations

Aug-20 11:56

- HR: 110% vs 0% Feb-32 Bund

- Spread set earlier at MS + 29bp (guidance was MS + 31bps area)

- Size: E4bln (MNI expected E3bln but noted upsizing to E4bln was possible)

- Books in excess of E33bln (inc E2.25bln JLM interest)

- Maturity: 15 April 2032

- Coupon: Short first

- Settlement: 28 August 2025 (T+6)

- ISIN: FI4000591862

- Bookrunners: Barclays (DM/B&D) / Bofa Securities / Danske Bank / Deutsche Bank / J.P. Morgan

- Timing: Hedge deadline is 13:00 UKT / 14:00 CET

From market source / MNI colour

US TSYS: Early SOFR/Treasury Option Roundup: Oct'25 10Y Calls Ongoing

Aug-20 11:45

SOFR and Treasury options volume gaining ahead of the NY open, large Oct'25 10Y call interest carries over from Tuesday, Sep Tsy option positioning/unwinds ahead of Friday's expiration. SOFR option flow more paired. Underlying futures trading steady to mildly higher (off highs after MBA apps data). Projected rate cut pricing retreat slightly from late Tuesday (*) levels: Sep'25 at -21.1bp (-21.7bp), Oct'25 at -34.9bp (-35.1bp), Dec'25 at -54.1bp (-54.4bp), Jan'26 at -65.1bp (-65.6bp).

- SOFR Options:

- 8,000 SFRU6 96.75/97.25 2x1 put spds ref 96.805

- 1,400 SFRZ5 96.25/96.37/96.50/96.62 call condors ref 96.21

- Block, 4,500 SFRZ5 96.25/96.50/96.75/97.00 call condors, 6.0 ref 96.21

- 6,000 SFRU5 96.00/96.12/96.25 call flys ref 95.90

- 4,000 SFRU5 95.87/95.93 put spds ref 95.90

- Treasury Options: (reminder Sep options expire Friday)

- Block/screen, over 10,800 TYU5 111 puts, 2 vs. 111-22.5/0.08%

- over 5,600 TYU5 112 calls, 8 last

- over 5,300 TYU5 112.5 calls, 2 last

- over 92,600 TYV5 113 calls, 20-23 ref 111-24.5 to -25.5 (78k trade Tuesday)

OUTLOOK: Price Signal Summary - Trend Needle In Gilts Points South

Aug-20 11:44

- In the FI space, a bear threat in Bund futures remains present. The contract traded sharply lower Friday resulting in a breach of 128.84, the Jul 25 low and bear trigger. Note that the 129.00 handle marks the base of a broad range and a clear range breakout would strengthen a bearish threat. This would open 128.40 initially, the Apr 9 low. Strength above the 50-day EMA of 129.89, is required to signal a reversal. Resistance at the 20-day EMA is at 129.58.

- Gilt futures traded sharply lower last Friday and Monday’s sell-off confirmed a bearish start to the week, strengthening current conditions. The contract has breached key short-term support and a bear trigger at 91.08, the Jul 18 low. This signals scope for an extension towards 90.11, the May 22 low. On the upside, resistance to watch is seen at 91.94, the 50-day EMA. Clearance of this average is required to highlight a potential reversal. First resistance is 91.32, Monday’s high.