EM ASIA CREDIT: JD.com: Weak profits at Food Delivery

(JD, A3/A-pos/NR)

"*JD.COM SAYS IT COMPLETED PURCHASE OF HK GROCERY CHAIN KAI BO" - BBG

Food Delivery losses widen, negative for spreads.

JD.com completed its HK$4bn acquisition of Hong Kong’s Kai Bo Food Supermarket. However, focus today is on below consensus Q2 results, where heavy losses in Food Delivery under the New Businesses segment drove a sharp decline in group profits. Group operating profits fell to RMB1.1bn in Q2 from RMB11.6bn a year earlier, as losses in New Businesses (RMB14.8bn) effectively erased core JD Retail earnings. This will have a negative impact also on peers, Meituan and Alibaba.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US: Is The Fed Chair Being Sacked Underpriced ?

A post on X from Congresswoman Anna Paulina Luna alluding to the imminent firing of Jerome Powell is adding fire to the situation. For the moment the market seems to be brushing this off and should it materialise is massively underpriced. What if the only way Trump can actually get yields lower is to replace the Fed Chair with someone who is willing to cut, and cut a lot. Should this happen it would further erode trust in US Assets and the USD would freefall once more. You would think the knee-jerk reaction would be higher in the Long-End but should an Uber Dove be appointed this could drive yields lower albeit with the front-end leading the charge and the curve steepening further.

- Rep. Anna Paulina Luna on X: “Jerome Powell is going to be fired. Firing is imminent.”

- (Bloomberg) -- “I think it sort of is,” President Donald Trump says when asked whether the renovations at the central bank were a fireable offense for Federal Reserve Chair Jerome Powell.

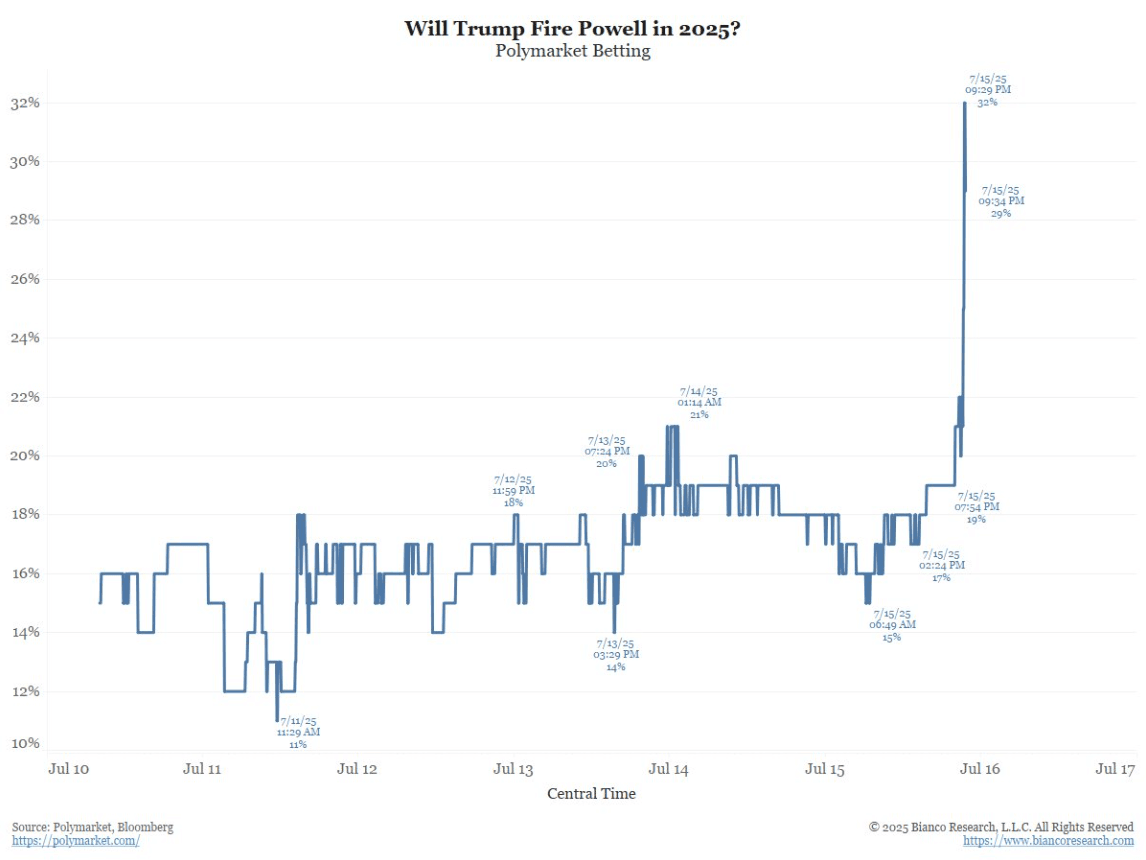

- Jim Bianco - “The betting market of “Will Trump fire Powell in 2025” has responded and the uptrend continues. See Graph Below.

Fig 1: Polymarket Betting - Will Trump Fire Powell In 2025

Source - @biancoresearch/Polymarket/Bloomberg

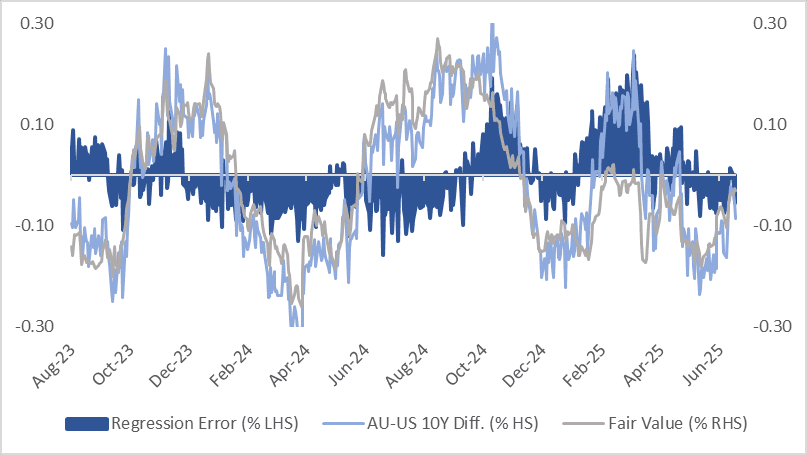

AUSSIE BONDS: AU-US 10Y Diff Is Near Middle Of Range

The AU-US 10-year cash yield differential currently stands at -7bps, positioned near the middle of the +/- 30bps range that has held since November 2022.

- A simple regression of the 10-year yield differential against the AU-US 1-year forward 3-month swap rate (1Y3M) differential over the past year suggests the current spread is slightly below fair value at -3bps.

- The 1Y3M differential, a key gauge of expected relative policy trajectories over the next 12 months, has traded within a 40bp range this year and is currently in the top half of the range at ~-5bps after last week’s surprise decision by the RBA to leave the cash rate unchanged at 3.85%.

- In early February, the 1Y3M differential had declined approximately 100bps since mid-September 2024, falling from +60bps to -40bps.

Figure 1: AU-US Cash 10-Year Yield Differential (%)

Source: Bloomberg Finance LP / MNI

JGBS: Modestly Cheaper At Lunch On A Data-Light Day

At the Tokyo lunch break, JGB futures have weakened and are hovering just above session lows, -18 compared to the settlement levels.

- (Bloomberg) -- Japanese stocks struggled for direction as caution around fiscal policy ahead of Sunday’s upper house election limited buying, but a weaker yen boosted tech and some exporters.

- Cash US tsys are flat to 1bp richer, with a flattening bias, in today's Asia-Pac session after yesterday's post-CPI sell-off.

- Cash JGBs are flat to 3bps cheaper (futures-linked 7-year) across benchmarks. The benchmark 10-year yield is 1.6bp higher at 1.597% after setting a fresh cycle high of 1.598% yesterday.

- Swap rates are flat to 1bp higher. Swap spreads are tighter out to the 20-year.