EU CREDIT SUPPLY: Japan Tobacco: Guidance

Aug-27 10:31

(JAPTOB: Hyb A3/A-/NR)

- Guidance: EUR500m WNG 30NC5.5 4.125%a (market sources).

- IPT: 4.625%a.

- Books above EUR7.6bn.

- We had FV 4.125% area.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EUR: Extending broader lows

Jul-28 10:30

- The EUR continues to dip lower against the USD, CAD, AUD, NOK, GBP, CNH, and JPY.

- Some of the earlier moves have been a function of the Dollar strength in early trade, although some market participants are still finding the extend of the USD bid at time perplexing.

- The pull back lower in EGB Yields and the fade off the high in European Equities have kept the lid on the EUR.

- Small supports in EURUSD are seen at 1.1631 and 1.1616.

LOOK AHEAD: Monday Data Calendar: Dallas Fed Mfg, Heavy Tsy Supply

Jul-28 10:27

- US Data/Speaker Calendar (prior, estimate)

- 07/28 1030 Dallas Fed Mfg Activity (-12.7, --)

- 07/28 1130 US Tsy $69B 2Y Note (91282CNP2) & $73B 26W bill auctions

- 07/28 1300 US Tsy $70B 5Y Note (91282CNN7) & $82B 13W bill auctions

- Source: Bloomberg Finance L.P. / MNI

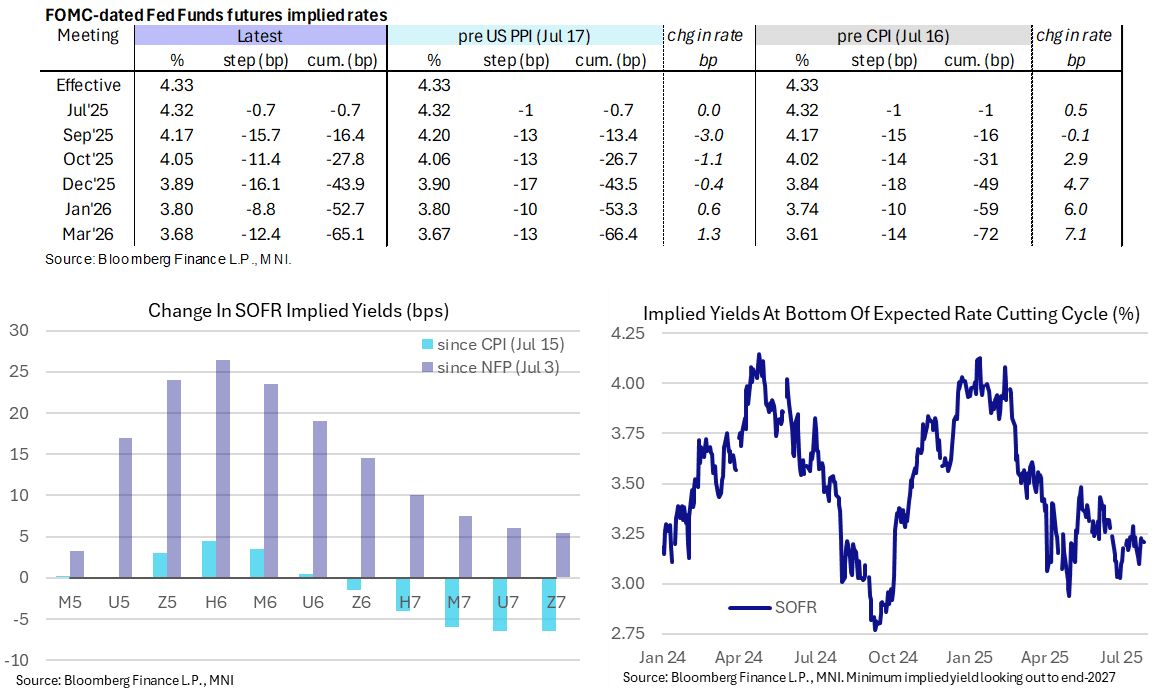

STIR: No Material Impact On Fed Rates From US-EU Trade Deal

Jul-28 10:22

- Fed Funds implied rates opened a touch firmer but are back to unchanged from Friday’s close for 2025 meetings, with no notable reaction from weekend announcements of a US-EU trade deal with 15% tariffs on EU goods.

- The deal had already been touted in the media, even if White House adviser Navarro had suggested to take those earlier reports with a "grain of salt".

- US-China relations with US Tsy Sec Bessent and China Vice Premier He Lifeng leading discussions in Stockholm through Tuesday this week.

- Cumulative cuts from 4.33% effective: 0.5bp for Wed, 16.5bp Sept, 28bp Oct, 44bp Dec, 52.5bp Jan and 65bp Mar.

- The 44bp of cuts to year-end is off last week’s high of 42bp, a level that was last sustainably higher in February.

- The SOFR implied terminal yield of 3.21% (SFRH7) is 1bp lower on the day, within a 3.1-3.3% range seen through July.

- MNI Fed Preview for Wednesday’s decision (with analyst version to follow later today as always): https://media.marketnews.com/Fed_Prev_Jul_2025_6823c76c5b.pdf