POWER: Italy October Power Trades Rangebound W/W

Sep-12 07:34

The Italian front-month power base-load contract is broadly stable on the week, closely tracking moves in EU gas prices, while forecasts for above-normal temperatures for most of September are providing upside.

- Italy Base Power OCT 25 down 0.6% at 106.4 EUR/MWh

- Italy Power Cal 26 down 1.2% at 104.96 EUR/MWh

- TTF Gas OCT 25 up 0.2% at 32.395 EUR/MWh

- EUA DEC 25 up 0.1% at 75.63 EUR/MT

- TTF front month is trading near the low for the week after falling back from a high of €33.44/MWh on Sep. 10. Seasonal maintenance in Norway is set against strong wind forecasts next week amid ongoing Russia sanctions uncertainty.

- The latest two-week ECMWF weather forecast for Rome suggests mean temperatures will remain mostly above normal through the forecast period, with a brief colder period around 22-23 September.

- Mean temperatures in Rome are forecast at 22.7C on Saturday and 23.4C on Sunday, from 22.8C on Friday and above the seasonal average.

- The PUN index edged down to €114.79/MWh for Friday’s delivery, from €115.81/MWh a day earlier.

- Wind output in Italy is forecast at 703MW during base load on Saturday and at 1.67GW on Sunday, from 1.41GW on Friday. Solar PV output is forecast at 9.27GW during peak load on Saturday and at 9.51GW on Sunday, from 10.45GW on Friday according to SpotRenewables.

- Residual load in Italy is forecast at 23.77GWh/h on Saturday and at 18.47GWh/h on Sunday, from 28.39GWh/h on Friday, Reuters data showed.

- Power demand in Italy is forecast at 29.81GWh/h on Saturday and at 25.79GWh/h on Sunday, from 35.27GWh/h on Friday, Reuters data showed.

- Italian residential/commercial gas demand is forecast at 30.4mcm/d on Saturday and at 28.mcm/d on Sunday, down from 36.3mcm/d on Friday, Bloomberg data showed.

- Italy’s hydro balance forecast has been revised up for the end of the forecast period to -382GWh on 26 September, up from -417GWh previously, Bloomberg data showed.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

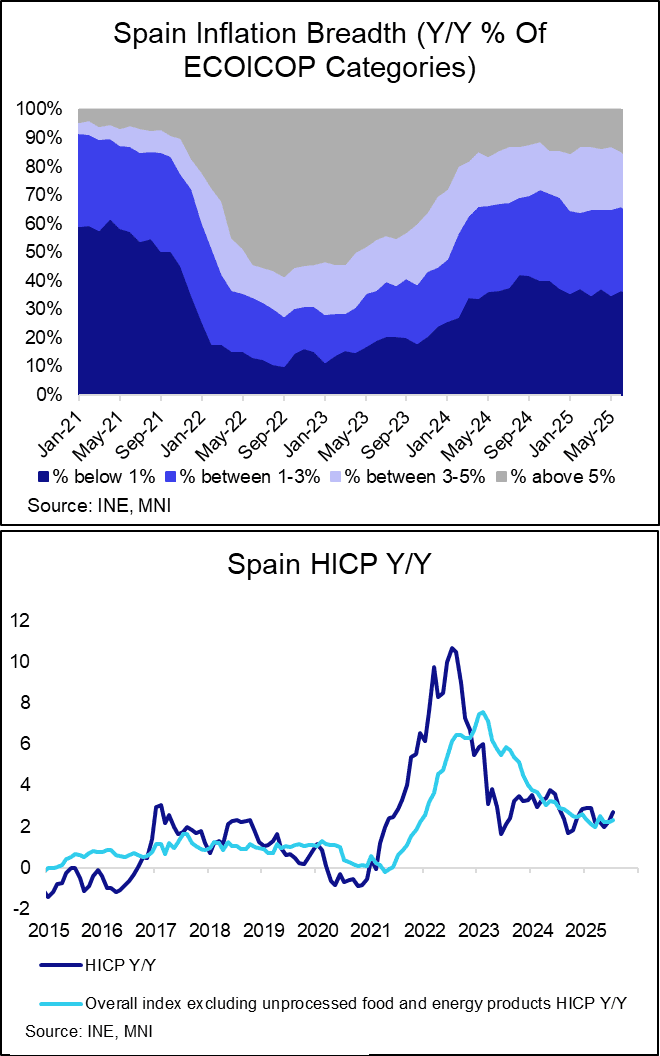

EUROPEAN INFLATION: Spain Final July HICP Confirms Flash, Airfares Push Up Core

Aug-13 07:32

Spanish final July HICP confirmed flash estimates at 2.70% Y/Y (vs 2.27% prior), while the monthly reading was revised up a rounded tenth to -0.3% (-0.34% unrounded, vs -0.4% flash). Excluding energy and unprocessed foods, HICP accelerated a touch to 2.34% Y/Y (vs 2.22% prior).

- As indicated in the flash release, there was a rise in electricity inflation (17.30% Y/Y vs 9.00% prior) which pulled the energy component higher in July. Energy HICP was 2.97% Y/Y (vs -0.77% prior).

- Elsewhere, services inflation ticked up to 3.63% Y/Y (vs 3.42% prior). This was mostly driven by a rise in airfares (international flights inflation was 13.61% Y/Y vs 3.46% prior), and to a lesser extent medical services, recreation and culture and accommodation inflation.

- Non-energy industrial goods pressures remain subdued, easing to 0.15% Y/Y (vs 0.29% prior).

- Unprocessed foods fell to 7.76% Y/Y (vs 8.45% prior), but remain elevated. Processed foods, alcohol and tobacco ticked up to 1.32% Y/Y (vs 1.20% prior).

- The proportion of HICP subcomponents with annual inflation rates above 5% rose to 18%from 15% in June, the highest since March 2024.

BUNDS: Full reversal in the German 30yr Yield

Aug-13 07:24

- Long end Germany Buxl lead the bounce to keep moving away from Yesterday's low.

- The German 5/30s printed a 98.28 high on the Cash Open, but now seeing some flattening bias, falling towards 96.00.

- That part of the Curve was trading around 94.57, when the 30yr Yield printed a 14yr High.

- The 30yr Yield is fading back to the July high it broke Yesterday, Buxl futures was trading around 115.38.

(Chart source: MNI/Bloomberg Finance LLP).

GILTS: Firmer Start

Aug-13 07:19

Gilts follow peers higher at the open, with oil a little off overnight lows.

- Futures as high as 91.95.

- Bears have countered recent bullish technical developments.

- They look to yesterday’s low (91.51) as their first target, which protects the Aug 1 low (91.44) and July 18 low/bear trigger (91.08).

- Conversely, bulls need to close yesterday’s opening gap lower (~92.25) before switching focus higher.

- Yields 2-3bp lower across the curve, modest flattening noted.

- 2s10s and 5s30s remain above 70bp and 140bp respectively, after yesterday’s steepening resulted in closes above. Intraday ’25 highs on both curves (84.6bp & 147.2bp) remain unchallenged.

- Fiscal issues continue to dominate local headlines. Guardian sources have reported that “the Treasury is looking at ways to raise more money from inheritance tax amid growing pressure on the country’s finances ahead of the autumn budget”.

- Curve steepening risks remain intact, albeit with crowded positioning and a more activist approach from policymakers when it comes to managing spikes higher in long end yields posing risks to that idea.