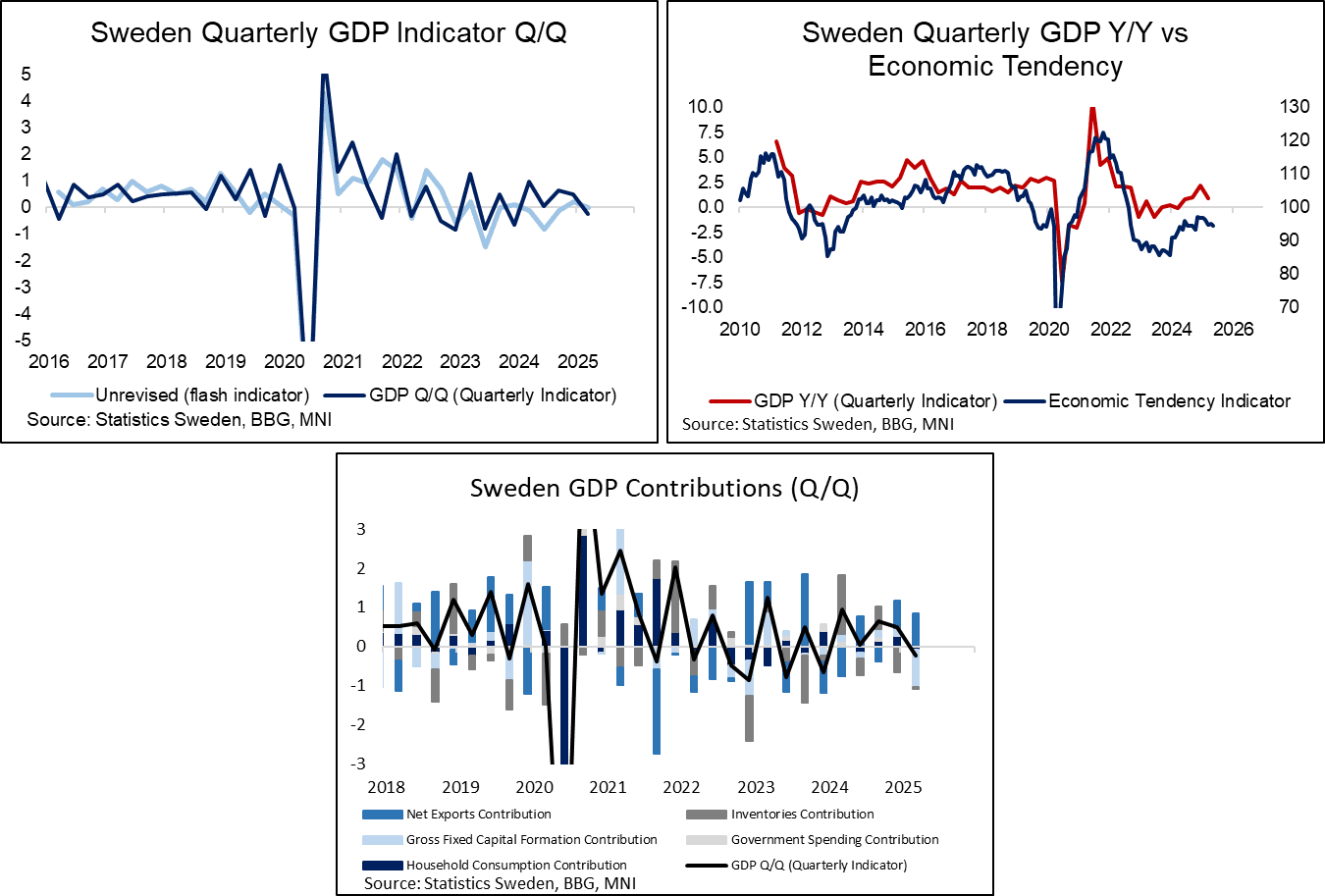

SWEDEN: Investment Drags Heavily On Q1 GDP

Gross fixed capital investment was the largest drag on Swedish Q1 GDP, falling 3.8% Q/Q (vs 0.7% prior) and pulling quarterly GDP down 1.0pp. All sub-components of GFCF saw negative sequential quarterly readings, but most notably buildings and construction at -7.5% Q/Q (vs 1.8% prior).

- Consumption fell 0.2% Q/Q (vs 0.6% prior), pulling quarterly GDP down 0.1pp. That’s despite the monthly household consumption indicator rising 0.7% 3m/3m as of March.

- Goods consumption fell 0.3% Q/Q (vs +0.1% prior) while services fell -0.1% Q/Q (vs +0.9% prior).

- Export growth was strong, at 1.8% Q/Q (vs 1.2% prior), adding 1.0pp to GDP. Goods (1.7% Q/Q vs 2.0% prior) and services (2.1% Q/Q vs -0.4% prior) both contributed. The strength in goods consumption could reflect some tariff front-loading – though this wasn’t obvious in monthly nominal trade data. Volume trends had been improving through March, though.

- Imports rose 0.3% Q/Q (vs -0.1% prior), dragging 0.2pp from quarterly GDP.

- Public consumption growth was 0.1% Q/Q (vs 0.1% prior).

- On the production side, goods producer value added fell 2.8% Q/Q (vs +1.3% prior), manufacturing was down 2.0% Q/Q (vs +0.5% prior), while services rose 1.1% Q/Q (vs 0.1% prior).

- Although LFS data pointed to 0.4% 3m/3m employment growth in March, total employed persons fell 0.1% in the national accounts. Hours worked in the business sector rose 0.1% Q/Q, implying productivity of -0.3% Q/Q.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JPY: The Yen is testing broader lows

- Some downside continuation for the Yen as Noted earlier since the EU Cash Govie open, nothing fast, but at new intraday low against the USD, GBP, EUR, while the Aussie still lags, although it is still the best performer, up 0.57% at present following the Australian CPI beat.

- The Overnight Japanese Data miss is likely playing a part, although the Overnight moves were more limited.

- USDJPY is eyeing Yesterday's high at 142.76.

EUROPEAN INFLATION: German HICP/CPI Y/Y Expected To Decelerate By 0.1pp [2/2]

Recap: German final March HICP was unrevised from the flash readings at 2.3% Y/Y (2.6% prior) and 0.4% M/M (0.5% prior). The final reading of national CPI was also unrevised at 2.2% Y/Y (2.3% prior) and 0.3% M/M (0.4% prior). Core CPI printed at 2.6% Y/Y (0.1pp upwardly revised, 2.7% prior), the lowest rate since June 2021.

- Overall, the CPI data confirmed a notable deceleration in services Y/Y inflation (a -0.13pp smaller contribution than in February) but with a caveat that it was mostly driven by airfares with the Easter holidays in April this year vs March last year.

- Goods inflation slightly accelerated (+0.04pp contribution vs prior) as softer energy was not quite able to cancel out firmer food / core goods inflation.

- The March CPI report highlighted differing Y/Y trends in services-heavy CPI subcategories:

- The mixed-weight transport category (i.e. across goods & services) was key in March at 0.88% Y/Y (state-level data had implied 0.9-1.0%) after 2.4% in Feb. It confirmed that energy (-2.77% vs -1.6% in Feb) and travel services (airfares -8.04% Y/Y vs 9.26% prior) acted in tandem here.

- Within the services-heavy CPI subcategories, there were some considerable differences in the Y/Y pace since December. Moderation was seen in education (4.67% Y/Y vs 5.0% Feb), restaurants and hotels (3.84% vs 4.2%) and recreation & culture (1.05% vs 1.1%). To the upside however, communications at -1.10% Y/Y (vs -1.2%) and healthcare at 2.98% (vs 2.8%).

- A material acceleration in food inflation was also confirmed, at 3.4% Y/Y after 2.8% in Feb.

- Categories associated with the core goods sector appear also firmer than before - clothing and footwear came in at 1.0% (after 0.5% prior) and furnishings and household Equipment at -0.25 (after -0.7%).

EUROPEAN INFLATION: German HICP/CPI Y/Y Expected To Decelerate By 0.1pp [1/2]

German April inflation is scheduled for 13:00 BST / 14:00 CEST today - however, we will receive state-level data likely amounting to 89.1% of the national basked briefly after 09:00 BST / 10:00 CEST. We will provide analysis on that, drawing signals for the later, national print.

- BBG Consensus (national level):

- HICP 2.1% Y/Y (vs 2.3% prior); 0.4% M/M

- CPI 2.0% Y/Y prior (vs 2.2% prior); 0.3% M/M

- Analyst views:

- Goldman Sachs sees HICP 2.2% headline, 3.1% core. “Services inflation to increase, driven by a notable contribution from travel-related services due to the timing of Easter this year. We expect package holidays to print close to 6%mom nsa, and airfares to come in at 11%mom nsa but see scope for a stronger print.” They expect “unprocessed food inflation to increase to 7.1%, mostly driven by a base effect.”

- Barclays sees German package holidays at 5.6% Y/Y, accommodation at 2.6% and airfares at 16.0% (all Y/Y). They see NRW headline CPI at 0.38% M/M.

- Morgan Stanley sees energy CPI/HICP at -5.4% Y/Y “on lower inflation in fuels, as well as electricity and gas” but “core inflation to rise on the positive base effect from Easter” (core CPI at 2.9%, core HICP 3.3%)

- The Bundesbank highlights in their April monthly report: “The inflation outlook is currently characterised by particular uncertainty. Prices on the energy markets have tended to decline recently, amid high volatility, and the euro has tended to appreciate against the US dollar. Based on the oil price path derived from forward prices and on the US dollar/euro exchange rate as this report went to press, the inflation rate is expected to be even somewhat lower in the near future."

- The April flash PMI noted “a slight uptick in the rate of inflation in average prices charged for goods and services. The acceleration from March’s four-month low was driven by a first – albeit marginal – increase in factory gate charges in almost two years. Services firms continued to display the stronger pricing power, although the latest increase in services output charges was the weakest since last October.”