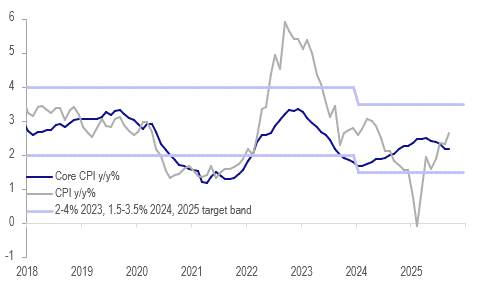

INDONESIA: Inflation Remains Contained, IDR Weaker Than Sept BI Decision

September core inflation held at 2.2%, 0.3pp below April’s peak, while headline was higher than expected at 2.65% up from August’s 2.3% due to higher volatile food prices and gold jewellery. Both measures remain well within Bank Indonesia’s 1.5-3.5% target band but with USDIDR at 16685 up 1.5% since the 17 September decision to cut rates, FX stability may become more important in October. Recent decisions have surprised with the focus on supporting efforts to boost growth rather than on the rupiah.

- The 6.4% y/y increase in food prices was driven by rice, chili and shallots.

- Global gold was up almost 12% over September and 47% higher than end-2024, therefore it is unsurprising that this has fed through to jewellery prices.

- State-administered prices remained subdued at 1.1% y/y.

- Clothing, utilities, dining out, IT & financial services and recreation saw stable inflation rates, while personal care, healthcare, transportation were higher and education and household equipment lower.

Indonesia CPI y/y%

Source: MNI - Market News/LSEG

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILT TECHS: (Z5) Bear Cycle Remains Intact

- RES 4: 92.15 High Aug 11

- RES 3: 92.06 High Aug 14

- RES 2: 91.45 High Aug 15

- RES 1: 91.24 High Aug 18 and a key near-term resistance

- PRICE: 90.52 @ Close Aug 29

- SUP 1: 90.22 Low Aug 27

- SUP 2: 90.11 Low May 22 and a key support

- SUP 3: 90.0089.99/ Psychological round number / Low Apr 9 (cont)

- SUP 4: 89.68 Low Jan 15 (cont)

A bear cycle in Gilt futures is in play and last week’s fresh cycle low reinforces current conditions. Note that on the continuation chart, moving average studies are in a bear-mode position, highlighting a clear downtrend - for now. First support to watch is 90.22, the Aug 26 low. A break would resume the bear leg and open the 90.00 handle. Initial resistance is at 91.24, the Aug 18 high.

USDJPY TECHS: Support Remains Exposed

- RES 4: 151.62 61.8% retracement of the Jan 10 - Apr 22 bear leg

- RES 3: 150.92 High Aug 1 and a key resistance

- RES 2: 149.81 76.4% retracement of the Aug 1 - 14 bear leg

- RES 1: 148.78/149.12 High Aug 22 / 61.8% of the Aug 1 - 14 bear leg

- PRICE: 146.93 @ 06:54 BST Sep 1

- SUP 1: 146.21 Low Aug 14

- SUP 2: 145.86 Low Jul 24

- SUP 3: 145.40 50% retracement of the Apr - Aug upleg

- SUP 4: 145.19 Trendline drawn from the Apr 22 low

A bear threat in USDJPY remains present and the pair is trading closer to its recent lows. The short-term bear trigger lies at 146.21, the Aug 14 low. Clearance of this level would resume a downtrend that started early August and pave the way for an extension towards 145.40, a Fibonacci retracement. For bulls, a resumption of gains would instead open 149.12, 61.8% of the Aug 1 - 14 bear leg. Key resistance is far off at 150.92, the Aug 1 high.

EUROZONE ISSUANCE: EGB Supply (2/2)

- Spain will come to the market on Thursday, holding a Bono/Obli/ObliEi auction. The three nominal bonds on offer will all be off-the-run: the 1.40% Jul-28 Obli (ISIN: ES0000012B88), the 3.10% Jul-31 Obli (ISIN: ES0000012N43) and the 4.20% Jan-37 Obli (ISIN: ES0000012932). The 1.00% Nov-30 Obli-Ei (ISIN: ES00000127C8) will be on offer alongside. The auction size will be confirmed today.

- Also on Thursday, France will hold a LT OAT auction, including the launch of a new 10-year OAT as we had expected. A combined E9.5-11.0bln of the new 10-year 3.50% Nov-35 OAT (ISIN: FR0014012II5), long 15-year the 3.60% May-42 OAT (ISIN: FR001400WYO4) and the long 30-year 3.75% May-56 OAT (ISIN: FR001400XJJ3) will be on offer.

- Belgium will conclude issuance for the week on Friday with an ORI auction. Details are to be confirmed tomorrow.

NOMINAL FLOWS: This week once again sees no redemptions. Coupon payments for the week total E8.2bln, of which E7.6bln are Italian and E0.4bln are from the EFSF. This leaves estimated net flows for the week at a positive E22.1bln, down from 28.9bln this week.