ENERGY: India Key Industry Output Grows 2% Year on Year

Aug-20 12:03

India’s eight key industries’ production increased 2.0% on the year in July, compared with growth of 2.2% y/y in June, revised up from 1.7%, data from the Ministry of Commerce & Industry showed.

- Petroleum refinery products fell 1% on the year vs a rise of 3.4% y/y in June

- Electricity output rose 0.5% on the year vs a revised fall of 1.2% y/y in June

- Coal fell 12.3% on the year vs a fall of 6.8% y/y in June

- Crude oil fell 1.3% on the year vs a fall of 1.2% y/y in June

- Natural gas fell 3.2% on the year vs a fall of 2.8% y/y in June

- The infrastructure output across the eight sectors makes up 40% of the country's industrial production.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

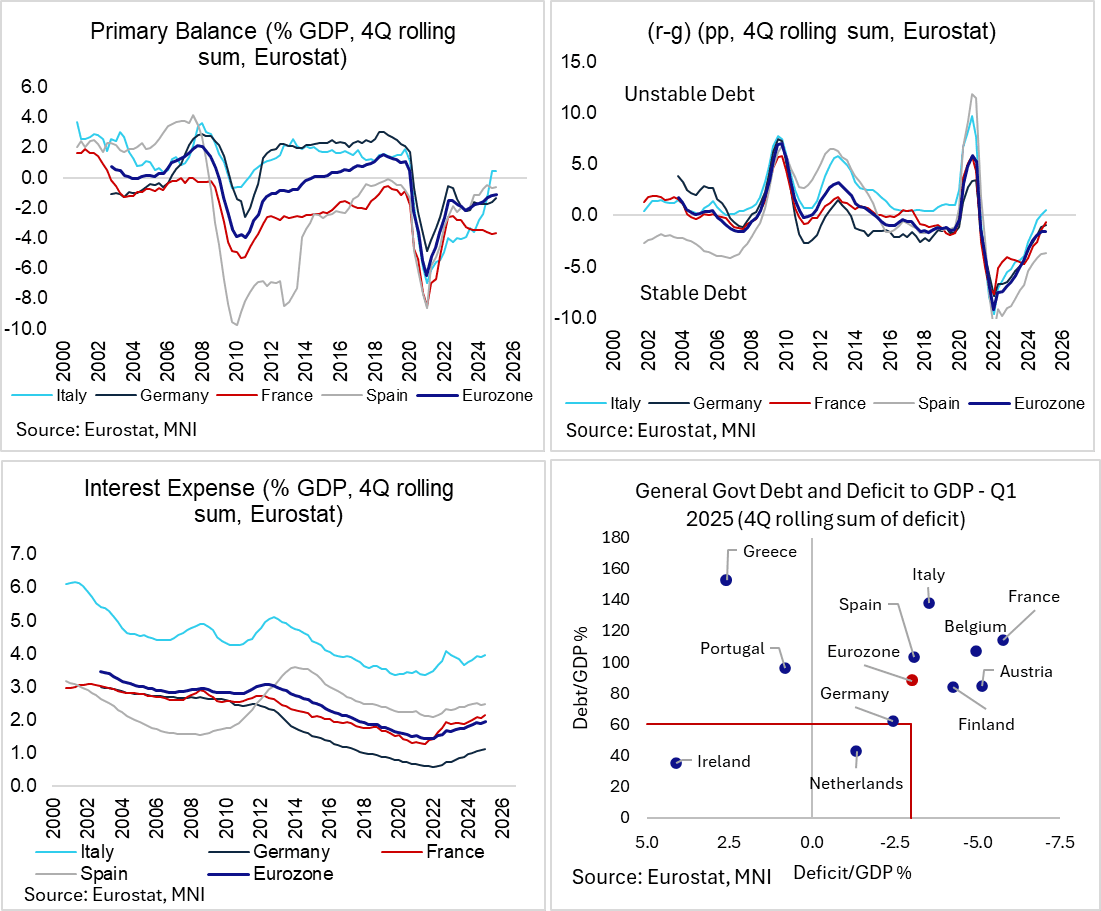

EUROPEAN FISCAL: Eurozone Debt Arithmetic Will Be Challenging In Coming Years

Jul-21 11:50

A likely slowdown in Eurozone nominal GDP growth will make debt/GDP arithmetic more challenging in the coming years. Annual Eurozone headline inflation is expected to move below 2% next year, while tariffs and associated uncertainty keep real growth risks tilted to the downside. This suggests nominal GDP growth will struggle to stay above the average interest rate on government debt, which continues to trend higher following large Covid-induced spending increases and the ECB’s 2022-2023 hiking cycle.

- The difference between the average interest paid on Eurozone government debt and the nominal growth rate (“r-g”) was unchanged at -1.6pp in Q1 (on a 4Q rolling basis). However, this differential has been narrowing since 2022 and increased across the four largest economies last quarter.

- In Italy, “r-g” was positive for the first time since 2021 at 0.5pp, up from 0.0pp in Q4. However, Italy ran a primary surplus of 0.4% in Q1 (again 4Q rolling sum to nominal GDP), implying debt is at least not on an explosive, unstable path higher. Italian 4Q average debt/GDP was 136.5% in Q1. The Italian government expects total debt/GDP to increase to 137.8% in 2026, before starting to fall towards 134.9% by 2029.

- The arithmetic in France is more worrying though. “r-g” rose 0.8pp to -0.7pp in Q1, while France ran a primary deficit of 3.6%. 4Q average debt/GDP rose to 114.1% from 113.2% in Q4. Although PM Bayrou outlined a E44bln savings plan for the 2026 budget last week, he is already facing significant pushback from opposition parties. This raises the risk of censure (and likely fiscal paralysis) or U-turns on proposed fiscal consolidation policies.

- Looking across the eleven largest Eurozone economies, only Italy (0.4%), Portugal (2.9%), Greece (6.0%) and Ireland (4.6%) ran a 4Q rolling primary surplus in Q1.

FOREX: USD Dips on Renewed Flattening Pressure

Jul-21 11:37

- Renewed flattening pressure in the Treasury curve is keeping the USD under pressure here - and GBP/USD is testing the Friday high as a result. Lower volumes are aiding the price action here, with G10 FX futures markets showing below-average activity for this time of day.

- Anticipated trade tension remains a key driver here as markets narrow in on the early August deadlines for US-RoW reciprocal tariffs, and the expiry of the extension granted to China to strike a broader deal. Retaliatory measures from the EU could be a key driver ahead. We reported last week that support for EU retaliation against US tariffs is "growing among member states and in the European Parliament, amid expectations that a likely trade deal by the Aug 1 deadline will disappoint the hopes of countries including France".

- As a result of greenback weakness to start this week, the USD Index has been contained by the 50-dma, which continues to trend lower. Failure to break above the 50-dma (today at 98.653) will signal that the correction higher off 96.377 may have concluded.

TARIFFS: Bessent On Trade Talks

Jul-21 11:34

- "U.S. TREASURY SECRETARY BESSENT ON AUG 1 DEADLINE: TALKS ARE MOVING ALONG -CNBC" Reuters

- "U.S. TREASURY SECRETARY BESSENT ON AUG 1 DEADLINE: QUALITY OF DEAL, NOT TIMING IMPORTANT" Reuters

- "*BESSENT: DOESN'T HAVE TO GET UGLY WITH THE EUROPEANS" Bloomberg