TURKEY: Imamoglu Ready to Back Other Candidates Against Erdogan

In a written response to questions from Bloomberg through his advisers, Istanbul Mayor Ekrem Imamoglu said he is open to endorsing an alternative candidate if he’s prevented from contesting the next presidential election.

- Imamoglu's university diploma was retroactively annulled in March, stripping him of the qualifications required to run for president. He also faces multiple charges, including corruption and supporting terrorism, and in July was convicted of threatening a prosecutor. While he is yet to be banned from politics, that could follow depending on the outcome of the cases.

- Meanwhile, hundreds of officials from opposition-led municipalities have been detained in a sweeping corruption probe launched after the opposition’s nationwide gains in the 2024 local elections. The most notable court case is scheduled for September 8, when a judge will rule on whether the CHP’s 2023 congress was legally valid.

- Bloomberg write that Ozgur Ozel has recently begun to circulate as a possible consensus candidate should Imamoglu be barred from running in the election currently scheduled for 2028, while Ankara Mayor Mansur Yavas is widely seen as another strong potential challenger to Erdogan.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Curve Steepens, Front End Supported By Bailey & REC

Futures top out at 91.85 before threatening a break below Friday’s low.

- Contract last 91.75.

- Bears remain in technical control and eye the July 8 low (91.42). Conversely, bulls initially need to clear the July 10 high (92.19).

- Little in the way of tangible impact from BoE Governor Bailey’s dovish comments and a soft REC labour market report further out the curve, although they do feed through into STIRs and the front end of the gilt curve.

- Yields -3bp to +1bp, curve twist steepens.

- Month-to-date ranges intact across the major benchmark yields

- 2s10s registers the highest level since April, 78.9bp, and is on track to register the highest close of ’25. The April 9 high (84.6bp) provides the next major upside target.

- 5s30s trades back above 140bp, with the ’25 intraday high (147.2bp) providing the next upside area of interest.

- GBP STIRs around pre-gilt open levels. SONIA futures flat to +3.0, while BoE-dated OIS shows ~54bp of cuts through year-end.

- The Mansion House event, as well as CPI & Labour market data, headline this week’s UK calendar. Please see our earlier STIR bullet/Global Week Ahead email for greater colour on those events.

US-RUSSIA: Trump Expected To Announce UKR Weapons Package, Endorse RU Sanctions

10:00 ET 15:00 BST: President Donald Trump will hold a (closed press) White House meeting with NATO SecGen Mark Rutte, where he is expected to finalise a new plan to arm Ukraine “that is expected to include offensive weapons,” per Axios. Later today, Trump is expected to make a 'major statement' on Russia. No timing has been released.

- Axios reports the plan is likely to include long-range missiles that could reach targets "deep inside Russian territory” a “major shift for Trump, who had until recently [said] he would provide only defensive weapons to avoid [escalation].”

- Politico reported the weapons package "numbers in the hundreds of millions”, and “could come from the fund approved by [Biden] that lets the DOD give weapons from the U.S. military stockpile...”

- Trump's 'major statement' is also likely to include preliminary approval of Senator Lindsay Graham's (R-SC) punitive sanctions/tariffs bill, reworked to provide Trump full discretion over implementation.

- Graham said on X: “.... A turning point is coming.” He told Axios: "Trump is really pis--- at Putin. His announcement tomorrow is going to be very aggressive."

- Senate Majority Leader John Thune (R-SD) indicated the bill will hit the Senate next week. House Speaker Mike Johnson (R-LA) endorsed the bill, putting it on a track to Trump’s desk.

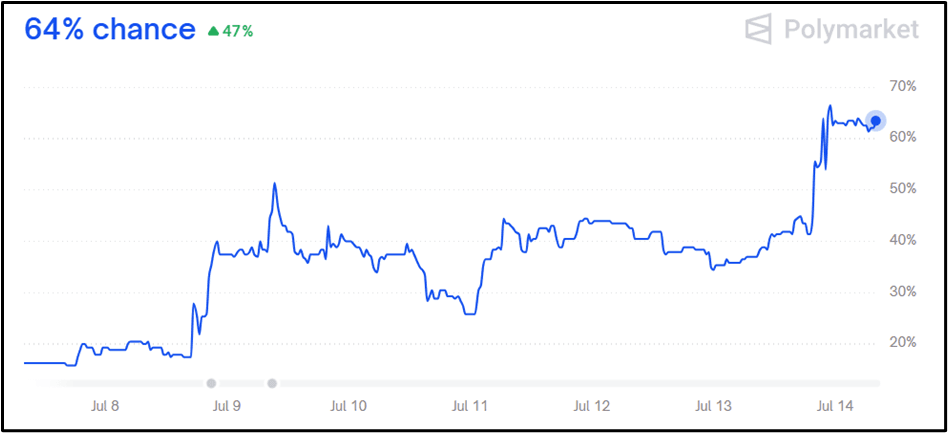

- Polymarket sees a 64% chance Trump increases Russia sanctions before August, a significant spike since last week.

Figure 1: Trump increase sanctions on Russia before August?

Source: Polymarket

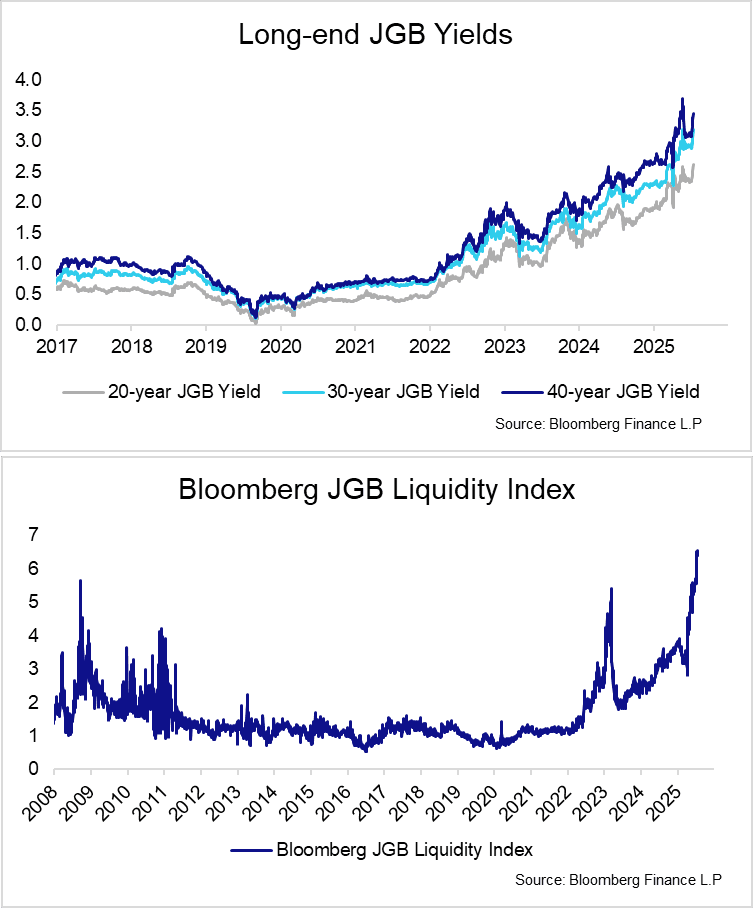

JGBS: Steepening Extends With 30-year Yields Eyeing May 21 High

Bear steepening in the JGB curve has extended this morning, spilling over into long-end EGBs and Gilts. 10s30s is currently just under 5bps steeper at 157.3bps, still below last Tuesday’s 160.3bp high.

- 30-year yields are up 11bps at 3.172%, with initial key resistance the May 21 high at 3.204% (the highest level since the BBG series began in 1999).

- Meanwhile, 10-year yields pierced the May 22 high of 1.582% overnight, but are currently back at 1.580% (+6bps today).

- As already noted, a combination of fiscal/political risks and possible upgrades to the BOJ’s inflation projections at the upcoming July 31 decision have contributed to the latest rise in yields.

- The Upper House election will be held on July 20. The LDP is on course to lose a significant number of seats and the governing coalition could also lose its overall majority. JNN reporting overnight was supportive of this scenario.

- Meanwhile the latest Bloomberg sources reporting was consistent with last week’s MNI Policy Team piece: BOJ officials may increase their median CPI forecast for FY25 from 2.2% partly due to a temporary surge in rice prices, MNI understands. The steepening of the curve suggests this is a contributing factor of today’s JGB selloff, rather than a driver.

- Structural forces pushing long-end JGB yields higher also remain in play, namely concerns around demand for long-end debt and weak liquidity at that portion of the curve.

- This week’s Japanese calendar includes 5-year supply tomorrow, June trade data on Thursday and June national CPI on Friday.