EU TRANSPORTATION: IDS: Final Books

4y >€3.25b, 7y >€3.9b.

Combined 5.1x cover.

Sterling 5y now -17bps/+0.7pts in secondary.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US OUTLOOK/OPINION: BofA See Onus Firmly On Data To Prevent Fed Cut

Writing after Fed Chair Powell’s Jackson Hole address on Friday, BofA noted that whilst they formally stick to their call for a hold next month, “the risks have obviously shifted meaningfully toward a cut”. BofA have been one of the more hawkish analysts in recent months, seeing no rate cuts through year-end.

- “The onus is firmly on the data to prevent a cut. A 4.2% u-rate in August, with 70k+ job growth and minimally negative/positive revisions, could keep a hold in play. A 4.1% u-rate would lower the threshold for payrolls, but 4.3% would raise it significantly. If it's a close call, August CPI and PPI should also matter.”

- “Barring further deterioration of the labor market, we think that the Fed would risk a policy error if it were to cut rates. We see signs that economic activity has picked up after the soft patch in 1H. If that is correct, the labor market will likely also rebound. Meanwhile, the underlying inflation picture - excluding of tariffs - has not improved since the Fed started cutting last year. The lagged housing component has decreased substantially, but other components have been flat or up.”

- “While challenging our view to fade near-term cuts, the speech endorses our recommendation to receive 5y OIS (entry 3.44, target 2.8, stop 3.8 current 3.40”). […] We continue to think that a dovish Fed, alongside easy financial conditions and sticky inflation, should support 10-year BEs and the belly inflation in the US versus Europe.”

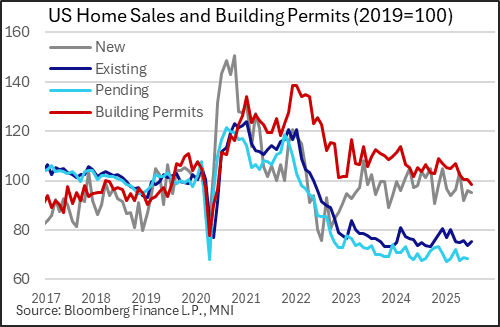

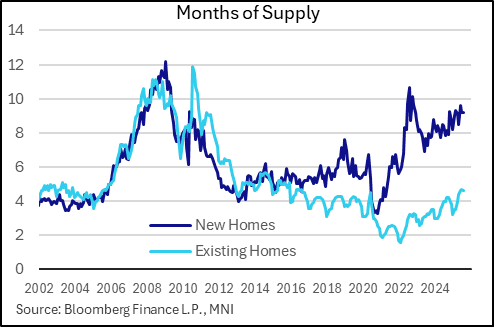

US DATA: New Home Sales Activity Not As Bad As Once Thought, But Still Weak

New home sales were much stronger than expected in July, with an upward revision to June suggesting that activity has been stronger this summer than previously estimated - but nonetheless, broader trends of elevated inventories and falling prices continue to suggest increasing slack in the new build market.

- The June reading of 652k (seasonally-adjusted, annualized) was better than the 630k Bloomberg consensus, but actually represented a slight fall (-0.6%) on the month due to a sizeable upward revision to June to 656k (from 627k). This is a significant improvement from May's near-18 month low (623k), though still keeps sales below pre-pandemic (2019) levels (and down 8% Y/Y).

- Regionally, sales were mixed, with falls in the Northeast and West more than compensated for by rises in the South and Midwest.

- The pickup in activity will be welcome news for homebuilders, though the rest of the data remained tenuous.

- One element of good news was that revisions were also seen in lower inventories, closer to 500k the last couple of months whereas June's data had previously shown 511k houses on the market which would have been highest since October 2007 (instead, the distinction of highest since 2007 reverts to March's 504k).

- That said, inventories remain over 9 months of supply equivalent (9.2 for 2 consecutive months) albeit a little below the 9.6 in May though well above levels that prevailed in the tight markets of 2021-23 and above the 7.9 months a year earlier.

- Additionally the data showed a 5.9% Y/Y fall in median prices ($403.8k, $20-30k below prices seen in 2022-23 at the height of the market).

- As such the broad sweep of data continue to indicate deterioration in the new homes market overall, though it may be worsening at a lesser rate than previously thought. This will continue to keep a lid on residential construction activity.

US TSY FUTURES: BLOCK: Sep'25 2Y Buy

- +6,000 TUU5 103-27.62, but through 103-27.5 offer at 1001:00ET, DV01 $215,400.

- Futures continue to unwind Friday's post-Chair Powell rally, however, with the 2Y contract trading 103-27.38 (-2.75)