EU AUTOMOTIVE: Hyundai Motor: Q2 results impacted by tariffs

(HYNMTR; A3/A-/A-)

Tariffs and incentives drag earnings lower, outlook murky, negative for spreads.

Hyundai Motor has reported Q2 results, with reported EBITDA down 11% YoY to KRW4.9T, ahead of consensus (KRW4.5T). Automotive segment revenues rose 5.1% YoY to KRW37bn, though crucially operating profits and margins came under significant pressure from poor mix, higher incentive spending and tariff impacts.

Reported 2Q25 Automotive segment operating profits declined 40% YoY to KRW2.2T, with an operating margin of 6.1%, down 450bp from 10.6% a year earlier. A strong performance in the Finance business, which saw operating profits increase 16% YoY, helped support group earnings overall.

Looking ahead Hyundai expects tariff impacts in Q3 to be higher than Q2.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

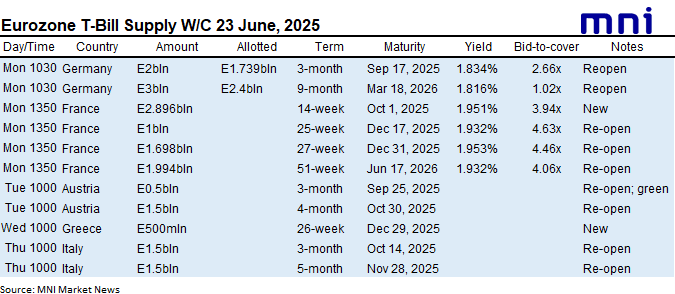

EUROZONE T-BILL ISSUANCE: W/C 23 June

Austria, Greece and Italy are still due to sell bills this week, while Germany and France have already come to the market. We expect issuance to be E18.1bln in first round operations, broadly similar to the E18.0bln last week.

- This morning, Austria will look to come to the market with E0.5bln of the 3-month Sep 25, 2025 Green ATB and E1.5bln of the 4-month Oct 30, 2025 ATB.

- Tomorrow morning, Greece will look to sell E500mln of the new 26-week Dec 29, 2025 GTB.

- Finally on Thursday morning, Italy will look to hold a 3/5-month BOT auction with E1.5bln of the 3-month Oct 14, 2025 BOT and E1.5bln of the 5-month Nov 28, 2025 BOT on offer.

GBPUSD TECHS: 50-Day EMA Support Remains Intact

- RES 4: 1.3800 Round number resistance

- RES 3: 1.3757 1.618 proj of the Feb 28 - Apr 3 - 7 price swing

- RES 2: 1.3681 1.500 proj of the Feb 28 - Apr 3 - 7 price swing

- RES 1: 1.3632 High Jun 13 and the bull trigger

- PRICE: 1.3561 @ 06:47 BST Jun 24

- SUP 1: 1.3506 Intraday low

- SUP 2: 1.3367 50-day EMA

- SUP 3: 1.3277 Trendline support drawn from the Jan 13 low

- SUP 4: 1.3140 Low May 12 and key support

The trend needle in GBPUSD continues to point north. Support at the 50-day EMA, at 1.3367, remains intact. A clear breach of this average would signal scope for a deeper retracement. Moving average studies are in a bull-mode position too highlighting a dominant medium-term uptrend. Key resistance and the bull trigger has been defined at 1.3632, the Jun 13 high. Clearance of this hurdle would resume the primary uptrend.

BOBL TECHS: (U5) Support Stays Exposed

- RES 4: 118.649 1.382 proj of the May 21 - Jun 3 - Jun 5 price swing

- RES 3: 118.531 1.236 proj of the May 21 - Jun 3 - Jun 5 price swing

- RES 2: 118.390 High Jun 13 and a bull trigger

- RES 1: 118.065 61.8% retracement of the Jun 13 - 16 downleg

- PRICE: 117.910 @ 06:24 BST Jun 24

- SUP 1: 117.530 Low Jun 5 and a key near-term support

- SUP 2: 117.470 Low May 21

- SUP 3: 117.470 Low May 21

- SUP 4: 116.660 Low Mar 27

Bobl futures remain in a bull cycle, however, the contract continues to trade below its Jun 13 high. The latest pullback has exposed key short-term support at 117.530, the Jun 5 low. A break of this level would highlight a stronger reversal and cancel the recent bull theme. This would open 117.470, the May 21 low. Key short-term resistance has been defined at 118.390, the Jun 13 high. Clearance of this level would be bullish.