HYBRIDS: Hybrids: Week in Review

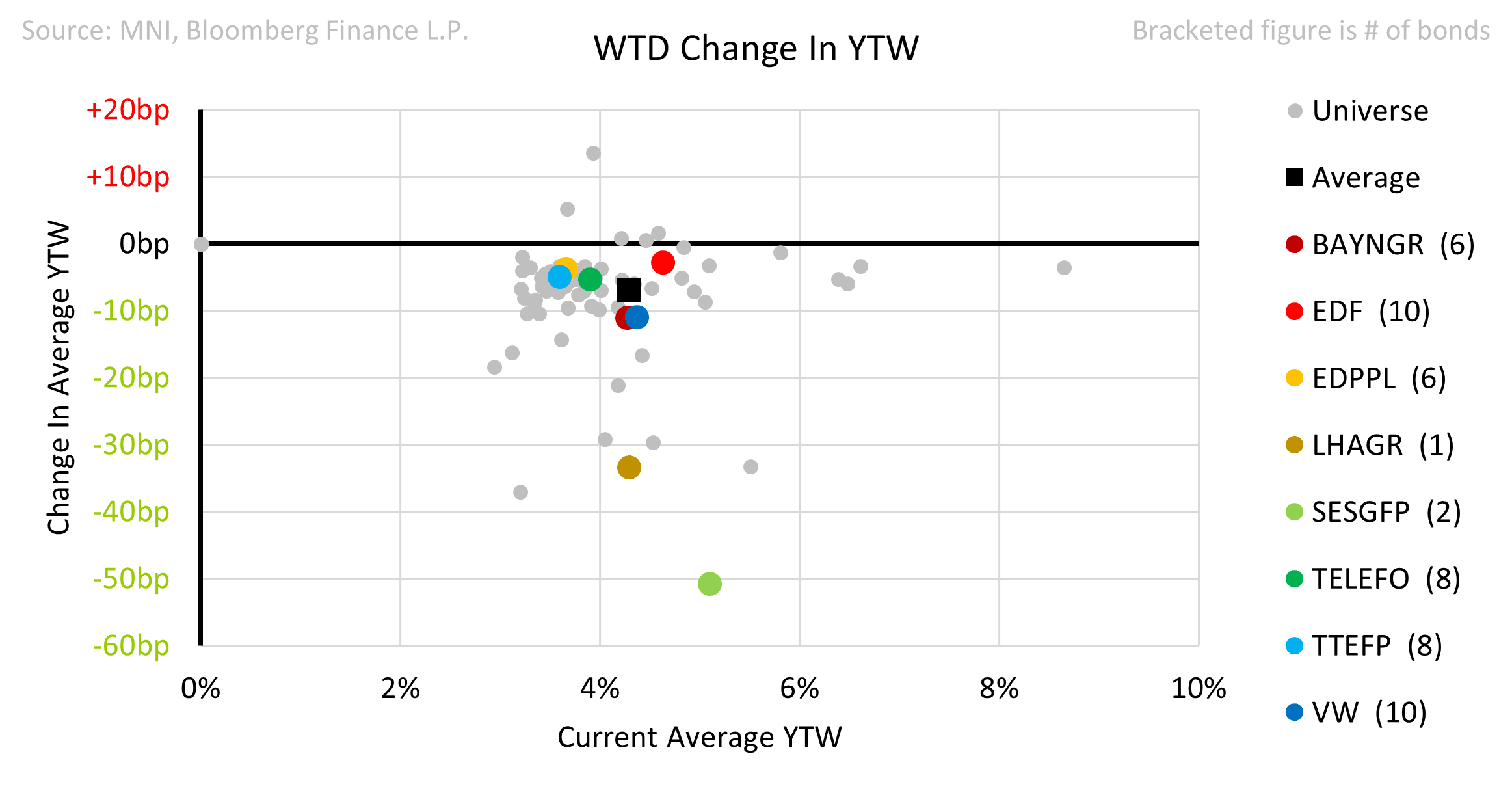

• EDF issued €1.25bn PerpNC5.5 combined with a tender for c.€1.22bn of outstanding NC26 bonds. The deal priced in line with fair value and sold off slightly in secondary.

• CPI Property issued £300m PerpNC5.25 via a Type A structure which will convert into equity-like units under certain conditions. The deal priced at 10% Annual yield which we saw as generous. Bonds were 1.25pts higher in secondary trading. The company is using the proceeds to repurchase a stake in its Polish unit.

• CityCon 7.875% NC29 is now 2.75pts lower since the COO’s departure last week.

• SES 6% NC32 is up 2.75pts on the week as any defence related names in Europe benefit from the US’s retrenchment.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: German Curve unwinds all the steepening bias

- Continued unwind in the German, in the back of the Buxl leading the Gains in Germany.

- After reaching its steepest level since March 2019 the 5s/30s is back below Opening levels.

- US Cash Tsys is also richer, while the belly underperforms, and curves are leaning flatter.

- Saw the Initial small resistance moving down to 129.18 in Bund, and this level has so far held, printed a 129.16 high.

BOE: Lombardelli: Neutral could be close to (or at) 4%

Lombardelli's comments are significant. She is saying that neutral could be close to (or at 4%). And she is deviating from the wider Bank guidance that rates are still "meaningfully restrictive." Highlights on her views below:

- In August "I judged it appropriate to pause the reduction of monetary restriction, due to my concerns about the current and expected above-target rates of underlying inflation and my judgements about the balance of supply and demand in the economy. I preferred to maintain the level of monetary restriction for longer rather than continue to reduce it at the previous pace."

- "At the time of the August decision headline inflation was 3.6% and it is expected to remain roughly between 3.5 and 4.0% for the remainder of this year. This is driven in part by inflation in food and energy - the most salient prices - and comes after a long period of relatively high inflation. This increases the risk of an inflation persistence scenario such as the one we considered in May."

- "It is less clear if the disinflation process is continuing in services prices"

- "While previous policy restrictiveness continues to weigh on the economy, I am less confident that the current policy stance as embodied in the market curve continues to be meaningfully restrictive. At the time of the August MPC vote, we had reduced rates by 100 basis points and I judged that there might not be that much further to go before the current policy stance is effectively neutral. Looking at history, it’s plausible that neutral may be closer to the upper end of the 2-4% range from Bank analysis. If so, this would mean we don’t have many more rate cuts to go as we potentially approach the end of the cutting cycle. I am not predicting that we are already at neutral, but nor am I confident that if we reduce restrictiveness much further we will still be sufficiently restrictive to return inflation to target sustainably."

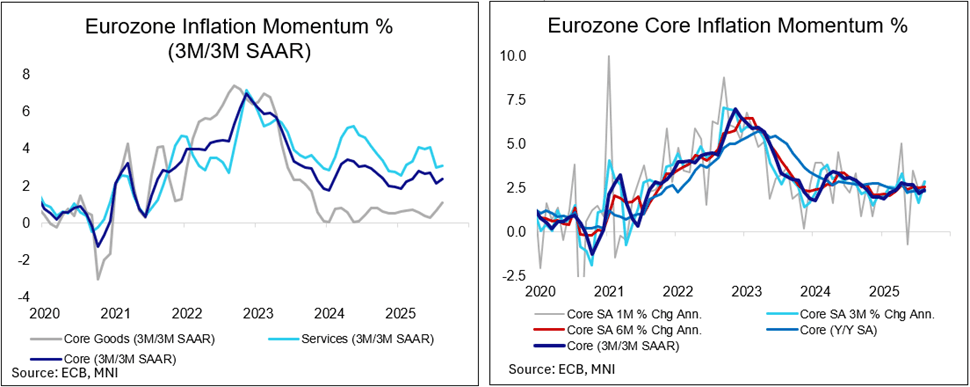

EUROPEAN INFLATION: MNI Eurozone Inflation Insight – August 2025

We have published the MNI Eurozone Inflation Insight, with the full report found here.

- Eurozone August headline HICP inflation printed marginally below consensus expectations on Tuesday, at 2.05% (cons 2.1) for essentially unchanged from the 2.04% in July.

- As we flagged in our preview ahead of country-level data, such a marginal downside surprise was not sufficient to ensure a dovish tilt in EUR rates, with markets pricing for both the September and October ECB meetings to remain largely out of play.

- A cumulative 7-8bps of cuts are currently priced to year end, which some Governing Council members appear to be leaning against.

- One of the stronger views here, but not a surprising one, was executive board member Schnabel in a Reuters interview Tuesday morning, while some other ECB officials continue to flag a further cut as a possibility – as Bank of Lithuania Chairman Simkus, also in an interview on Tuesday morning.

- ECB President Lagarde meanwhile said on Monday (Sep 1) that the Eurozone inflation goal of 2% has been met, building on her comment from the Jul 24 press conference that “Inflation is currently at our two per cent medium-term target”.