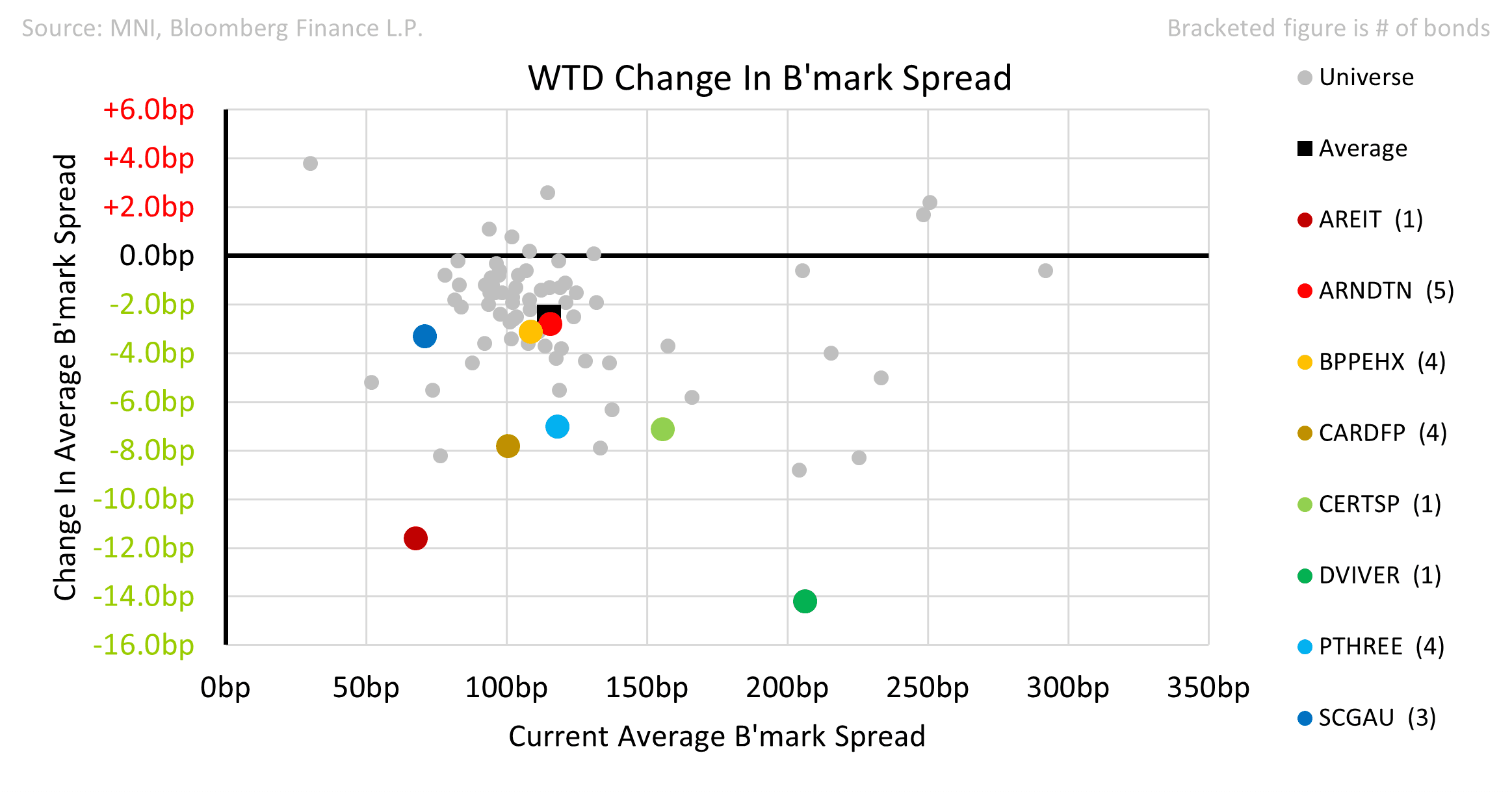

EU REAL ESTATE: Property: Week in Review

Real Estate continued tighter with nearly 3bps of tightening this week. Month-on-Month the sector is 9.5bps tighter (including some BB names) with some very significant moves in BB+/BBB- borrowers. Altrarea -38bps; Alstria Office -42bps; CapitaLand Ascendas -36bps; New Immo -65bps; IWG -26bps; Public property -30bps; Sirius -27bps; VGP -35bps. CityCon is the outlier on the downside with a +33bps widening (MoM) on persistent management turnover.

• P3 Group (PTHREE) issued a new 7.5yr. The issuer is 100% owned by GIC and logistics assets are in favour currently. This was the company’s 5th visit to the market, and the heightened profile helped the existing paper to rally. PTHREE 32s were 16bps tighter on the week.

• Carmila also saw secondary performance. Its 32s rallied 10bps on the combination of a Tender for shorter dates and a blow-out 7.25yr deal which came 15bps inside FV with a nearly 8x book.

• Blackstone Property Partners released a healthy H1 report with share of Logistics continuing to grow.

• Stoneweg (CERTSP) was upgraded by Fitch.

• Scentre was able to borrow €500m in 8yr 25bps through its former associate URWFP reflecting the strength of its position in the Aus/NZ market.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SWEDEN: August Flash Inflation Due Tomorrow; Key For Riksbank Sep Decision (1/2)

Swedish August flash inflation is due tomorrow at 0700BST/0800CET and will be key in determining whether the Riksbank can cut rates as early as the September 23 decision. Markets currently price the September decision as a coin toss between a 25bp cut and hold.

- The median analyst surveyed by Bloomberg expects CPIF ex-energy inflation at 3.1% Y/Y (vs 3.2% prior), but five of the eleven forecasters expect a sub-3% reading. The Riksbank projected 2.71% Y/Y in the June MPR, but this projection is stale given the large upside surprise seen in June.

- The range of analyst expectations is likely due to differing assumptions on the extent to which summer inflationary impulses (e.g. for package holidays and car rentals) are unwound.

- Although full details of the report will not be available until the final release on September 11, we think that annual CPIF ex-energy disinflation of 0.3pp (i.e. a 2.9% Y/Y or below rounded reading) would be sufficient to give at least three Executive Board members confidence that the summer inflation uptick is likely to be temporary.

- This may pave the way for a (potentially not unanimously supported) cut in September, and drive a material intraday market reaction in SEK FX and rates.

- A 3.0% Y/Y rounded reading would probably also be sufficient to driven some intraday reaction, but would place more importance on the final inflation report to assess underlying inflation details. On balance, it could push the likelihood of another cut into Q4 (i.e. the November or December decisions).

- Headline inflation is expected to accelerate to 3.2% Y/Y (BBG analyst range 3.0-3.5%), from 3.0% in July. This is expected to be driven by a base effect on electricity inflation.

BONDS: EUREX ROLL Pace (update)

- Buxl: 52%.

- Bund: 62%.

- Bobl: 80%.

- Schatz: 66%.

- BTP: 44%.

- BTS: 52%.

- OAT: 50%.

CANADA DATA: Q2 Labour Productivity Down As US Trade War Hits Factories

- Canada labour productivity -1.0% in Q2 as GDP -0.7% and hours worked +0.3%. It was the biggest decline since Q4 2022, StatsCan says Wed.

- Manufacturing and wholesale were the biggest contributors to the decline amid US trade tensions.

- Q2 hourly compensation (-0.5%) decreased for the first time since the first quarter of 2021.

- Productivity YOY was 0.0%.