UK FISCAL: Huge implications for markets from today's fiscal data

Sep-19 11:24

- The release of today's fiscal data is huge driver for UK (and global) markets today. Overall it shows that borrowing is overshooting the OBR's forecast YTD by GBP11.4bln (whereas the data released last month estimated that the OBR's forecasts were on track. It's largely VAT receipts being lower, "other tax receipts" below lower and local authority borrowing being higher that's driven the surprise today (see "Other Tax" Receipts; Local Authorities Drive PSNB Higher, 11:39BST)

- This suggests that the starting point for the upcoming OBR forecasts is looking much worse than expected before today's release (as we noted earlier in Timetable and economic / fiscal data included in the OBR's forecasts, 8:29BST will likely incorporate one more fiscal release next month).

- The UK Budget is likely to be the biggest domestic UK event for the rest of the year (even more so than any MPC meeting, despite the uncertainty over whether there could be a cut or not in Q4).

- Today's data suggest we will need a combination of higher gilt issuance or spending cuts or tax increases that are even more brutal than they would have otherwise been. With income tax / employee NIC / VAT increases ruled out in the manifesto, this increases the probability of more taxes on specific goods and services which could feed through to higher inflation - and push back rate cuts further, too.

- This is then feeding into markets: the acceleration of the fiscal deterioration, along with the risk of meaningful productivity forecast markdowns from the OBR, have promoted steepening on the gilt curve.

- This builds on yesterday’s moves on the 2s10s and 5s30s curves, while limiting any outright recoveries from session lows in the long end.

- GBP FX is also hugely impacted by fiscal matters at present (and sticky inflation) with EURGBP hitting its highest level since 7 August this morning.

- We would also flag that the moves in reaction to today's fiscal data have been larger than those seen in response to the MPC meeting yesterday.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY OPTIONS: Large Oct'25 10Y Call Interest - Ongoing

Aug-20 11:21

- Over 87,900 TYV5 113 calls, 20-23 ref 111-24.5 to -25.5

- 50k traded at 19 yesterday, total volume over 78k, saw open interest rise by 48,990 to 158,754.

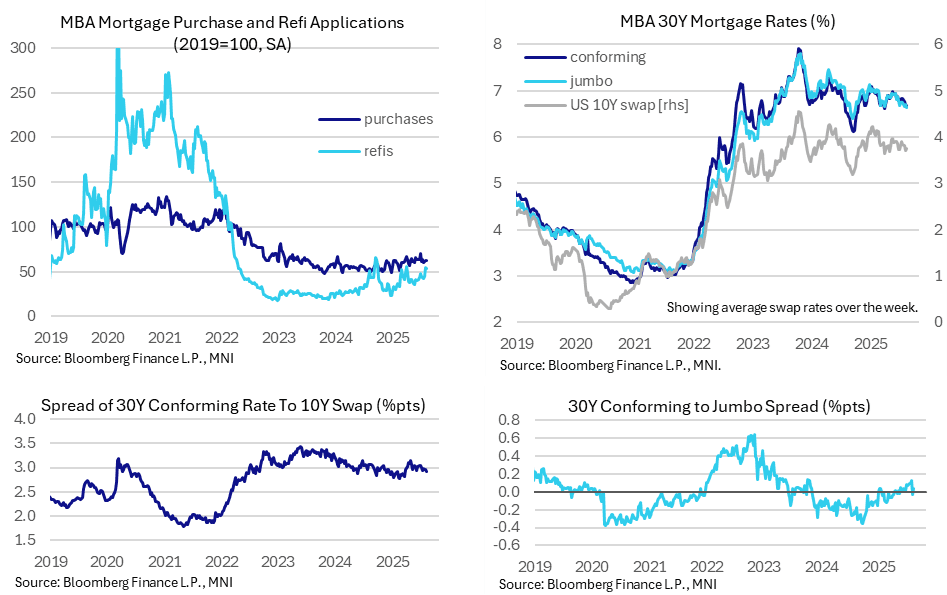

US DATA: Mortgage Applications Hold Onto Most Of Refi Boost

Aug-20 11:18

- MBA composite mortgage applications edged -1.4% (sa) lower last week to hold onto most of its refi-driven 11% increase the week prior.

- Indeed, new purchase applications increased 0.1% after 1.4% whilst refis dipped -3.1% after 23.0%.

- Levels relative to 2019 averages: composite 59%, new purchases 62% and refis 53%.

- The 30Y conforming rate was near unchanged on the week at 6.68% (+1bp) after the 6.67% the week prior was the lowest since early April.

- Coupled with a 5bp rise in the average 10Y swap rate over the week and the 30Y mortgage to 10Y swap spread fell below its range of 300bp +/-5bp seen mostly since reciprocal tariff announcements in April vs 285bps averaged in Q1. That is however just one week and it's only a relatively small decline.

- Jumbo loan rates meanwhile have reverted to trading inside regular rates again after a 6bp decline to 6.64%. The regular to jumbo spread of 4bp compares with -3bp the week prior and 12bp the week before that at what was its highest since Oct 2023.

SWEDEN: Government Projects Recovery In 2026; Economy In Balance In 2027

Aug-20 11:10

The Swedish Government updated economic forecasts here

- "Sweden’s economic recovery began in late 2024 but was interrupted in early 2025 when the US administration announced high tariffs against the EU and the rest of the world"..."The tariff agreements signed over the past few months are expected to reduce the risk of an escalated trade conflict, which is positive for growth both in Sweden and among its neighbours. Swedish households have begun to show optimism after a period of low expectations. Going forward, increased domestic demand is seen as particularly vital for Sweden’s recovery."

- "The prospects for recovery are good. From the second half of 2025, real wage growth, lower interest expenditure and an accommodative fiscal policy are expected to contribute to steady growth in household consumption"

- "Overall, growth is expected to be higher next year, and in 2027 the Swedish economy is predicted to be essentially in balance. "

- "The labour market recovery is expected to be slightly delayed, and employment is forecast to rise at a faster rate in 2026."