BOE: Headlines from Bailey's media interview

"*BAILEY: TIMING, SCALE OF CUTS MORE UNCERTAIN THAN BEFORE AUGUST

*BAILEY: MARKET PRICING SIGNALING WAIT-AND-SEE APPROACH ‘RIGHT’" Bloomberg

Those headlines seem the most pressing here. Will be interesting to see the full context behind the latter, but the first seems to imply not much has changed since August.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

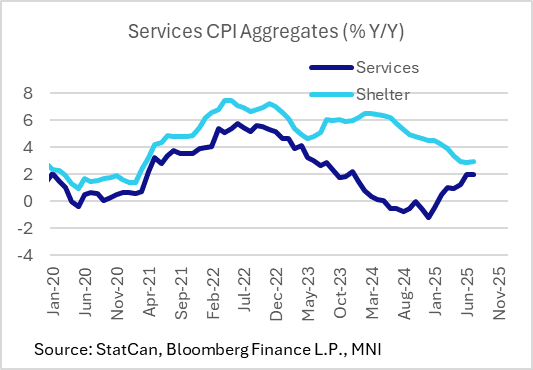

CANADA DATA: Pickup In Shelter Prices Defies Broadly Softer Services CPI (2/2)

Services prices decelerated below 3.0% Y/Y for the first time since January, at 2.8% after 3.0%. However, this came despite the main surprise in the CPI report was in shelter: it unexpectedly accelerated to 3.0% Y/Y from 2.9% - just a 2-month high but most expectations had been for a further deceleration. And indeed, this was the first uptick in shelter since February 2024.

- Within shelter, owned accommodation inflation fell to 2.5% after 2.8%, marking a fresh 52-month low - but rented accommodation rose to 5.0% after 4.6%, a 3-month high, while water/fuel/electricity rose to a 4-month high 0.6% Y/Y after 3 months of deflation. Most analysts we'd seen had expected a slowdown, not an acceleration, in rent pressures. Mortgage interest costs slowed to 4.8% Y/Y from 5.6%, continuing the longer-term trend.

- Non-shelter services decelerated by 0.3pp. One volatile category - air transportation - saw an increasing degree of deflation (-10.6% after -9.2%). And travel/tours, which had been cited by BOC Gov Macklem as an area of volatility potentially only temporarily pushing up core inflation, saw a continued downward move (-1.7% Y/Y after -0.4%).

- Elsewhere in services, household operations saw continued disinflation, recreation/education/reading and transportation (fuel-related) were soft; health and personal care was steady.

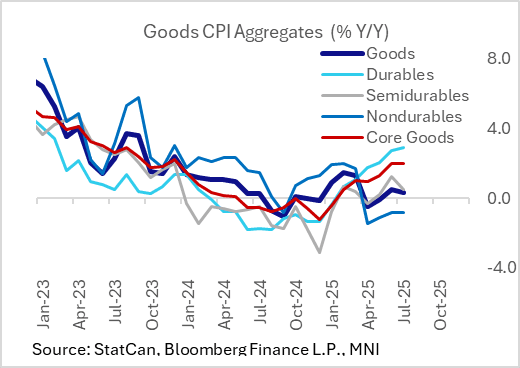

CANADA DATA: Goods Inflation Comes In Mixed, With Durables Leading Rise (1/2)

Looking into the "surprises" in the largely below-expected Canada July inflation aggregates, we generally saw goods inflation as mixed-to-very slightly lower than expected, contrasting with a slightly stronger set of services price data than anticipated.

- The main upward contributors to Y/Y July headline CPI were on the shelter side: rent rose 5.1% Y/Y, mortgage interest cost 4.8%, and property taxes/"other special charges" 6.0% - more on this shortly. Rounding out the top 5 contributors were passenger vehicle purchases (4.5%) and restaurant food (3.2%).

- The main downward contributors: as expected, gasoline (-16%), natural gas (-7%)m and fuel/parts/accessories for RVs (-14%) appear to reflect the base effect of the end of the carbon tax in April, with air transport (-11%) and telephone services (-5%) in the top 5 drags on Y/Y CPI.

First looking at goods categories: overall CPI diminished to 0.3% Y/Y in July from 0.5% prior. But core goods (ex-food purchased from stores/energy) remained steady at 2.0% for a 2nd consecutive month, a joint-post Dec 2022 high. This was probably on the in-line/soft side of expectations.

- Within goods, upside pressure on durables - considered sensitive to tariff / countertariff impacts - continued, rising to 2.9% Y/Y from 2.7% for a 29-month high (and well up from the negative readings in 2024). However, they appeared not as high as feared.

- Passenger vehicle purchase inflation as noted was 4.5% Y/Y, up from 4.1% prior but appearing to be less acute than analyst estimates we'd seen. Furniture price inflation remained steady (3.3% Y/Y), with appliances reaccelerating (0.6% after -0.4%).

- Semidurable goods inflation pulled back sharply to 0.5% from 1.3% (which had been an 18-month high), and nondurables remained negative Y/Y at -0.8%.

- The slowdown in non-durables including some offsetting factors, with food price inflation unexpectedly picking up to 3.3% from 2.9% prior (had decelerated for 2 consecutive months), with pressures more acute for store-bought food (3.4% after 2.8%) than for restaurants. On a seasonally-adjusted M/M basis, food prices were steady at 0.4%.

- Energy prices fell largely as expected, by 10.4% Y/Y.

- However clothing and footwear price inflation was on the soft side, pulling back sharply after a June spike (0.8% Y/Y after 2.0%, corroborated by the SA M/M readings (-0.7% after +0.7%) and helping keep overall core goods prices down.

BONDS: Broader buying in US Tsys and EGBs

Some broader intraday high in Bond futures on both sides of the Pond, for Treasuries and EGBs.

Not seen any standout flow, around 5k in Bund, 3k in TYU5 cumulative, but Block trades also went through in Germany, suggest all buyer, helping the upticks:

- RXU5 total of ~6k at 129.06 (2 Blocks).

- UBU5 ~2.2k at 113.76.

That little pullback lower in Yield is helping the USDJPY towards the session low.