GOLD: Gold Pauses Rally On Robust Risk Sentiment, Watching Events

After rising each session in August, gold prices were down 0.3% to $3369.33/oz on Wednesday but still up 2.4% this month driven by weaker US data and higher US tariffs. They are currently around $3369.4. They didn’t find support from the lower US dollar (BBDXY -0.4%) or yields as they were pressured by robust risk appetite and they considered the latest developments including a punitive 25% tariff on India for buying Russian oil, Fed talk suggesting it is closer to a rate cut and the prospect of Russia-Ukraine talks.

- The Fed’s Daly and Cook sounded dovish saying that “we will likely need to adjust policy in the coming months” and that payrolls were a possible “turning point” respectively.

- Trump said that special envoy Witkoff made “great progress” in Russia and that he should meet with President Putin next week and that Putin and President Zelensky should meet soon. He sounded very uncertain though on the chance of a truce.

- Bullion fell to a low of $3358.34 before recovering somewhat. It held above initial support at $3268.2, 30 July low. Initial resistance is at $3390.5, 5 August high. The rally over the rest of August though signals that declines are corrective and the bull cycle started on 30 June is intact.

- Silver is 3% higher in August but the rally paused on Wednesday with the metal little changed at $37.830 after falling to $37.622. It is currently at $37.885. Trend signals remain bullish with initial resistance at $39.655. Initial support is at $36.216.

- Equities rallied with the S&P up 0.7% and Euro stoxx +0.3% and the S&P e-mini has started Thursday +0.2%. Oil prices fell again with WTI -1.4% to $64.27/bbl. Copper rose 0.6%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

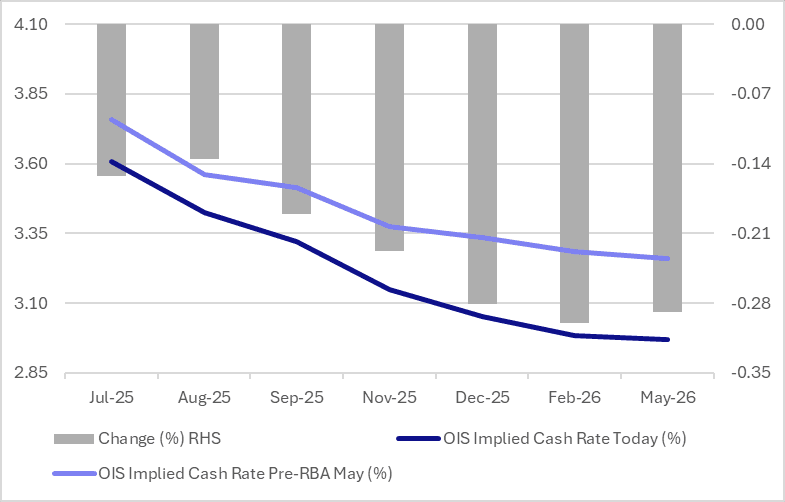

STIR: RBA Dated OIS Almost Fully Priced For A 25bp Cut Today

RBA-dated OIS pricing is slightly firmer on the day across meetings ahead of today’s RBA Policy Decision.

- A 25bp rate cut this week is given a 94% probability, with a cumulative 79bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- Notably, pricing across meetings is 14-30bps softer than levels before the May 20 RBA Meeting.

Figure 1: RBA-Dated OIS – Current Vs. Pre-RBA (May)

Source: Bloomberg Finance LP / MNI

JGBS: Futures Unchanged Overnight, US Tariffs Remain In Focus Ahead Of Aug 1

In post-Tokyo trade, JGB futures closed unchanged compared to settlement levels, despite US tsys finishing with a modest bear-steepener (1-6bps cheaper).

- Bloomberg - President Donald Trump's plan to impose 25% tariffs on goods from Japan starting Aug. 1 may have negative implications for the US bond market as soon as this week. Japan is the largest foreign holder of US Treasuries. If investors there view Trump's move as unacceptable, they could skip a few Treasury auctions and have a meaningful bearish effect on bond prices.

- Bloomberg - "Meiji Yasuda Life Insurance Co. plans to avoid actively investing in Japanese super-long-term government bonds for the next 1-2 years as interest rates may rise and supply pressures build."

- Today’s US calendar will see NFIB Small Business Optimism, Consumer Credit and a $58B 3-year note auction. However, the main focus will be on the FOMC minutes for the June meeting.

- Today, the local calendar will feature trade balance and Bank Lending data alongside 5-year supply.

AUSSIE BONDS: Cheaper Ahead Of RBA Policy Decision

ACGBs (YM -2.0 & XM -3.0) are cheaper after US tsys finished with a modest bear-steepener (1-6bps cheaper).

- US tsys had gapped higher briefly early Monday after Treasury Secretary Bessent alluded to several trade announcements expected over the next 24 hours, with "plenty of countries wanting to make deals." However, US tsys swiftly pulled back from highs amid a general lack of specifics from the Trump administration.

- Cash ACGBs are 2-3bps cheaper with the AU-US 10-year yield differential at -17bps.

- The bill contracts are flat to 2bps cheaper.

- Today, the RBA is widely expected to cut by 25bps. This is the sell-side consensus, albeit with a small number of economists expecting rates to be left on hold.

- May monthly CPI data should give the RBA confidence to cut. The trimmed mean eased to 2.4%y/y. Services inflation is still running at a stronger pace, but we continue to move off recent highs for this sub-sector of inflation.

- RBA-dated OIS pricing is little changed across meetings. A 25bp rate cut today is given a 94% probability, with a cumulative 77bps of easing priced by year-end.

- The AOFM plans to sell A$1200mn of the 4.25% 21 December 2035 bond tomorrow and A$1000mn of the 2.75% 21 November 2029 bond on Friday.