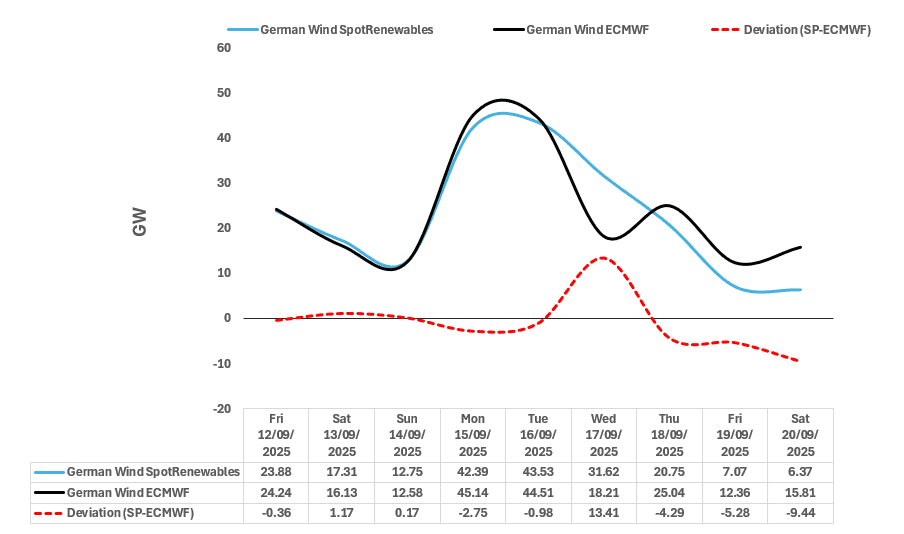

RENEWABLES: German Wind Output Forecast Comparison

See the latest German wind output forecast for base-load hours from SpotRenewables vs Bloomberg’s ECMWF model for the next seven days as of Thursday afternoon.

- Both models suggest similar wind output forecast through 16 September.

- SpotRenewables’ forecast suggests a gradual decline in wind output from 16 September, while Bloomberg’s model suggests lower wind output on 17 September and a slight rebound on 18 September.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: Richmond's Barkin: "Balance" Between Dual Mandate Variables "Still Unclear"

Richmond Fed President Barkin (non-voter in 2025 and 2026) continues to lean to the hawkish side in a speech released Tuesday called "Why the Consumer Matters" (link).

- On current monetary policy, as usual he holds back on making any explicit projections. While he says the "the fog" of uncertainty in multiple areas "is lifting", he appears to suggest that more time and data is still needed before making any decisions: "at our July meeting, with the labor market near most estimates of maximum employment and inflation above target, the FOMC continued to hold the fed funds rate at a modestly restrictive level. We may well see pressure on inflation, and we may also see pressure on unemployment, but the balance between the two is still unclear. As the visibility continues to improve, we are well positioned to adjust our policy stance as needed."

- He appears to downplay the recent weakness in nonfarm payrolls when revisions are taken into account: " businesses have been in a low hiring-low firing mode that has created an unusual but stable labor market. Unemployment remains low at 4.2 percent, near most estimates of maximum employment... Job gains have slowed recently, which is certainly worth watching. But I’m hopeful that even as businesses face cost and price pressure, they’ll largely avoid the type of large layoffs that would spike unemployment and lead to consumer pullback. As with consumers, how businesses have come into this moment matters. Firms are already running lean. They’ve been slow-rolling hiring for years in anticipation of a recession that hasn’t come. They’ve been downsizing via attrition. With businesses already light on staff, we should see fewer reductions. So, any coming increase in the unemployment rate may well also be less than many anticipate."

- That said, he doesn't appear too worried about inflationary pressures, due to consumers not having the same purchasing power as they did in the pandemic reopening episode: " this isn’t 2022, when we saw inflation balloon. For one, the Fed’s policy stance is more restrictive now. But beyond that, remember that back then, consumers were flush with cash due to pandemic stimulus, suppressed spending, higher wages, and frothy asset markets. They didn’t let price increases hinder their revenge spending. That fueled inflation. That’s just not where consumers are in 2025. They feel stretched, particularly those with low and moderate incomes. They are more willing to defer purchases if prices go up. Should they feel forced to accept price increases for certain products, I expect they will forego spending for others. I’m sure your procurement teams are thinking the same way. This dynamic may already be playing out: Amid all the talk of tariffs and higher goods prices to come, we’ve seen people stock up on iPhones and cut back on services, such as air travel and lodging. If we see this kind of demand destruction more broadly, the inflationary impact of tariffs would be less than many anticipate."

US: Trump on Tariffs and Goldman Sachs

Donald J. Trump

@realDonaldTrump

Trillions of Dollars are being taken in on Tariffs, which has been incredible for our Country, its Stock Market, its General Wealth, and just about everything else. It has been proven, that even at this late stage, Tariffs have not caused Inflation, or any other problems for Country, other than massive amounts of CASH pouring into our Treasury’s coffers. Also, it has been shown that, for the most part, Consumers aren’t even paying these Tariffs, it is mostly Companies and Governments, many of them Foreign, picking up the tabs. But David Solomon and Goldman Sachs refuse to give credit where credit is due. They made a bad prediction a long time ago on both the Market repercussion and the Tariffs themselves, and they were wrong, just like they are wrong about so much else. I think that David should go out and get himself a new Economist or, maybe, he ought to just focus on being a DJ, and not bother running a major Financial Institution.

FED: Fed Gov Nominee Miran: No Tariff Inflation; Service Disinflation Imminent

Fed Governor nominee (and current CEA head) Miran on CNBC says he "just can't comment on current monetary policy at the moment" due to his impending Senate nomination. However he reiterates his view that there's little to no evidence of tariffs translating into stronger inflation, and he also makes the case that domestic services inflation will pull back "profoundly" due to reduced net immigration.

- "At the aggregate level, when you look holistically across the inflation data, there's just no evidence of [tariffs] whatsoever."

- "If you look at core... two of the strongest categories this month in terms of inflation were used cars and airfares. And neither of those have anything to do with tariffs. We don't import used cars from from abroad in large scale. And airfares are on domestic services... we've been doing a lot of thinking about just how much of this inflation is due to the illegal immigration that's occurred... Our calculations are that the massive in surge of renters into an only sluggishly adjusting housing supply probably boosted rents by about 4-5%. And that's a significant contribution to overall inflation at a time when the housing stock adjusts only slowly... we think that there's a very strong reason for thinking of very profound service disinflation coming up in the near future, as net migration has come to zero because the President's strong border policies."

- On the BLS jobs data, he says there's an element of "noise, uncertainty" that has "increased in recent years", including the birth-death model. "So this is a degradation in the quality of the statistics that has occurred. And I think the President is dead right when he says, we need to fix this. We need to make these statistics reliable. We need to make them believable. We need to make them credible. And I'm really delighted we're shaping up to be able to do."

- He says that re economic surveys, the BLS should consider "incentive schemes to drive response rates higher. I think that we can start thinking about ways to optimize the collection system, optimize the survey system, optimize the timing of responses. I think that we should be thinking critically about these questions."