JPY: FX Exchange Traded Straddle Option

Oct-10 12:53

JPYUSD (5th Dec) 66 Straddle sold at 1.97 in 1k.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: Dovish Adjustment In Fed Pricing After PPI

Sep-10 12:46

Dovish repricing in the U.S. front end in the wake of the inline to softer-than-expected PPI release.

- FOMC-dated OIS now shoes 27.5bp of easing for this month (~10% odds of a 50bp cut), with a cumulative 46.5bp showing through October and 68.5bp of easing priced through December.

- Contracts 0.5-1.5bp more dovish vs. pre-data levels.

- SOFR-implied terminal rate pricing 2.88% vs. 2.93% heading into the data and post data extremes of 2.855%.

- Our macro team notes that the short answer for why PPI was so much softer than expected in August was the final demand trade services category, which as we noted in our preview is extremely volatile and prone to revisions.

- It's also why "core" PPI - which excludes trade as well as food/energy - was in line with expectations at +0.3% M/M. More to come shortly, but from the report, basically the categories that jumped in July causing so much concern reversed in August.

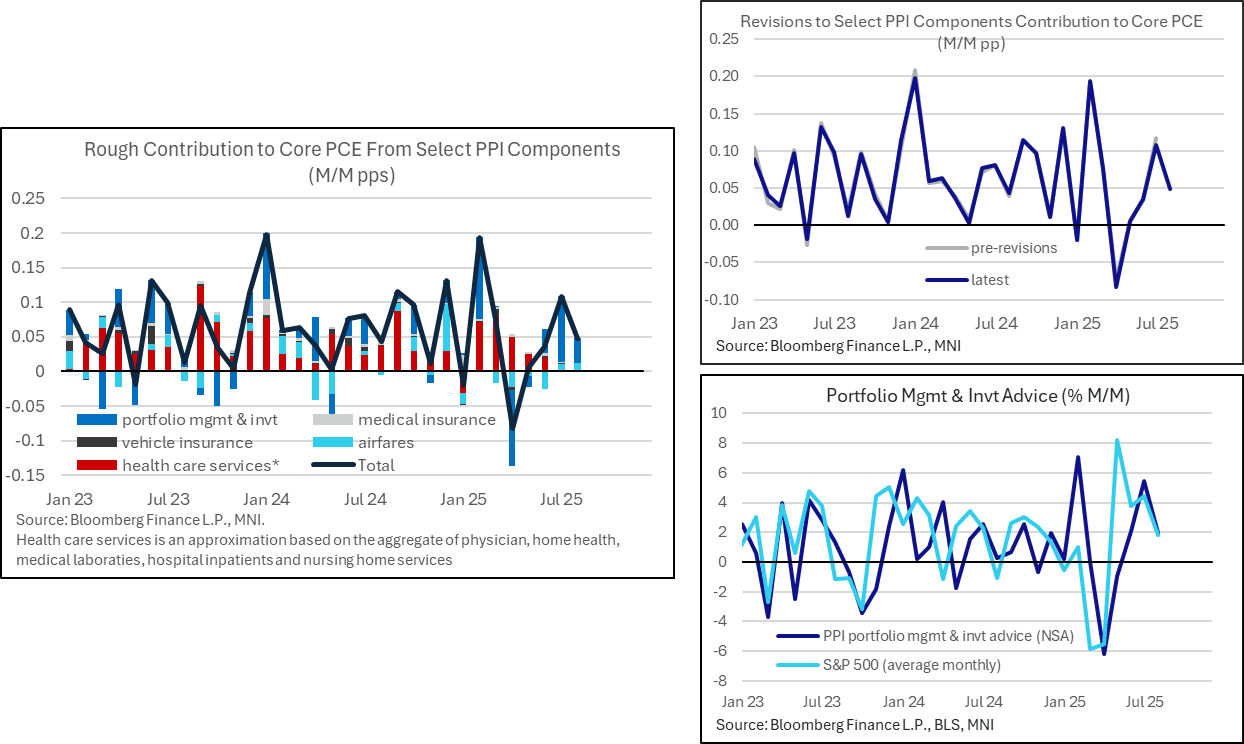

US DATA: PCE-Relevant Components In PPI Cool After A Strong July

Sep-10 12:41

- Our crude proxy for core PCE contributions stands at 0.05pps in August after offsetting revisions with a still strong 0.11pp in July (vs 0.12pp previously) and 0.04pp in June (vs 0.03pp).

- PPI portfolio management and investment advice: 1.9% M/M after a near enough unrevised 5.5% M/M. We’d only seen Nomura on this beforehand (2.2%) and don’t think this reading will have surprised many although if anything it's on the slightly soft side considering recent strength in equity markets.

- As you can see in the contributions chart below, this category has been providing a lot of the upside recently.

- Our collection of health care services is seen as having a second month of zero M/M contribution, in what’s a clear soft patch since earlier in the year.

US TSYS: Post-PPI React

Sep-10 12:34

- Fast two-way as Treasury futures extend lows before gapping higher after lower than expected PPI inflation data and down-revisions to prior.

- Currently, the Dec'25 10Y trades +2 at 113-13 (yld 4.0645 -.0230) vs. 113-16 high -- Initial resistance above at 113-21+ High Sep 5.

- Curves steeper: 2s10s +0.402 at 53.111, 5s30s +0.860 at 112.185.

- Soft PPI heads enough to re-trigger USD weakness, erasing the entirety of the morning's tepid gains on Poland/Russia headlines. GBP/USD's show back above 1.3550 tops out at 1.3563, still well short of yesterday's highs into 1.3590.