JGBS: Futures Little Changed Overnight, US Tsys Bull-Flatten

In post-Tokyo trade, JGB futures closed little changed, -1 compared to settlement levels. US tsys finished Thursday with modest gains, long end leading.

- US core goods prices accelerated to 0.28% M/M from 0.21% prior, a little shy of expectations of a rise to the low 0.30s.

- Initial jobless claims surprisingly jumped to 263k (sa, cons 235k) in the week to Sep 6 after a slightly downward revised 236k (initial 237k).

- Samantha LaDuc on X: "Toyota can absorb the 1 trillion ($6.8 billion) cost of a 15% automobile tariff and make profits [estimates 3 trillion ($20.4 billion) in earnings after the tariffs]. However, few companies are as resilient as Toyota. According to a 2024 Cabinet Office survey of 587 large listed Japanese manufacturing exporters, the 40 most competitive companies expected to be able to record profits [on their exports] even if the yen rose to 101. However, the 127 least competitive companies [22% of these listed firms] would need the yen to weaken to the 146-152 range to be able to compete and maintain a profit." Richard Katz Nikkei."

- Today, the local calendar will see IP and Capacity Utilisation data alongside an Auction for Enhanced-Liquidity 5-15.5 YR.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

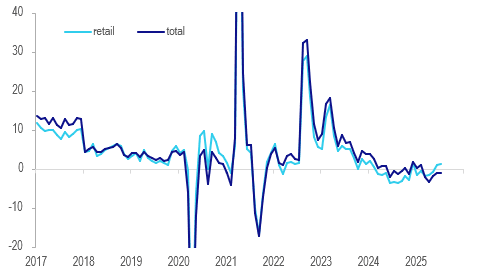

NEW ZEALAND: Gradual Recovery In Retail Card Spending

July NZ card transactions rose 0.6% m/m, the highest monthly increase this year, but the annual rate is still down 1.0%. Retail spending was up 0.2% m/m rising 1.2% y/y, signalling a gradual recovery in nominal consumption. It has been trending higher since the March trough at -1.8% y/y. The RBNZ is likely to cut rates on August 20 as inflation is in the band and the economic recovery remains subdued, and the July card data was consistent with this.

- While total retail spending rose slightly on the month, the core was close to flat. Statistics NZ noted that consumables transactions rose 0.5% m/m, while vehicles ex fuel jumped 5.2%. Apparel fell 1.9% and durables -0.8%.

- Non-retail ex services expenditure increased 1.6% m/m but services only 0.3%.

NZ card spending y/y%

Source: MNI - Market News/LSEG

JGBS: Futures Weaker Overnight After US CPI Data, PPI & 5Y Supply Due

In post-Tokyo trade, JGB futures closed weaker, -18 compared to settlement levels, after US tsys finished with a twist steepening on Tuesday.

- The focus was on the July CPI for insight on the FOMC's policy path. That the data failed to surprise on the hotter side of expectations opened the door a little wider for a September rate cut.

- Despite a further acceleration in monthly core inflation in July, there was an unexpectedly steady rate of core goods CPI - key to the overall inflation outlook given expectations for tariff passthrough to accelerate this summer. (MNI's Inflation Insight has more details, PDF here).

- That provided a strong underpinning for Wall Street which climbed to record highs.

- (Bloomberg) -- "Japan's current benchmark 10-year government bond wasn't traded at all on Tuesday, the first such instance in more than two years, according to data from an institutional brokerage."

- Today, the local calendar will see PPI and Machine Orders data alongside 5-year supply.

AUSSIE BONDS: Twist Steepener With US Tsys, Q2 Wages Due

ACGBs (YM +1.5 & XM -1.0) are slightly mixed after US tsys finished with a twist steepening on Tuesday as the key details of the July CPI report came in softer than widely expected.

- Despite a further acceleration in monthly core inflation in July, there was an unexpectedly steady rate of core goods CPI - key to the overall inflation outlook given expectations for tariff passthrough to accelerate this summer. (MNI's Inflation Insight has more details, PDF here).

- The short-end saw a post-CPI rally, buoyed by deepening Fed cut expectations: a 25bp reduction in September is now 94% priced (up from about 88% Monday), with 60bp of cuts through end-2025 (up from 57bp Monday).

- Cash ACGBs are 2bps richer to 1bp cheaper with the AU-US 10-year yield differential at -4bps.

- The bills strip is flat to +2.

- RBA-dated OIS pricing is slightly softer across meetings today. A 25bp rate cut in September is given a 37% probability, with a cumulative 52bps of easing priced by year-end.

- Today, the local calendar will see the Q2 Wage Price Index.

- The AOFM plans to sell A$1200mn of the 4.25% 21 December 2035 bond today and A$1000mn of the 2.75% 2 1 November 2029 bond on Friday.